Download

1 / 7

70 likes | 85 Views

Institutions of Budget Execution: Rules and Roles. Richard Allen Budget Execution and Financial Accountability Course November 3-5, 2003. What Are Budgetary Institutions.

E N D

Institutions of Budget Execution: Rules and Roles Richard Allen Budget Execution and Financial Accountability Course November 3-5, 2003

What Are Budgetary Institutions • The rules and regulations according to which budgets are drafted, approved and implemented. Budgetary outcomes thus depend on how well these rules are both designed and observed. • Institutions, (i.e. rules), are distinct from the organizations established to implement them. • But organizations matter greatly too, for effective implementation and enforcement.

Understanding Budget Implementation • A key distinction: • Formal Rules • Informal Rules • And: • How budgets are implemented is greatly affected by how they are put together.

Main Actors in Budget Implementation Central Management • Ministry of Finance • (Ministry of Planning) • Ministry of Public Service • Office of the President • Inspection Generale des Finances • Accountant General • Government Control Office • Central Procurement Agency • Central Tender Board • National Debt Office • Central Bank • Line Ministries,Departments and Agencies • Budget/Finance Department • Procurement Department • Financial Controller, Ordonnateur, Treasury Accountant (MOF) • Internal Audit Unit • Oversight Bodies • Supreme Audit Institution • Legislature • CivilSociety

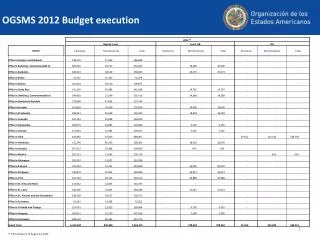

Case Study Country X – What to Do? • There are detailed budget laws and regulations covering all aspects of budget execution. Controls are centralized in the MOF (Hacienda) and the independent Controleria. • The budget/finance departments of line ministries are a paper-shuffling operation with a limited role in budget preparation and little influence on budget execution. • The annual budget documents are voluminous (20 volumes) and impenetrable. • The budget as implemented is very different from the budget as approved. Over 20,000 supplemental appropriations are approved each year. Each supplementary must be approved by the MOF. • The budget includes more then 10,000 performance indicators but these are only loosely connected to the budget planning process or budget allocations. Few programs are adequately costed. • The accounting system does not produce timely and accurate data on the different stages of the expenditure process (e.g. commitments are unrecorded). • Internal control and audit are generally effective – conducted through the Contoleria, with staff allocated to each budget entity. • Within MOF, there is lack of “connectivity” between different departments and units, lack of detailed knowledge of line ministries, and limited capacity to implement new reforms. • The Minister of Finance has initiated a budget reform. This focuses on reengineering the budget processes within the MOF and introducing an integrated financial management information system. • The supreme audit institution focuses on compliance and regularity audit, and produces its reports with a long (up to 2 years) delay. • The Congress has limited capacity to exert effective oversight and control.

How should the Bank advise the Government to strengthen its budgetary institutions?