Download

1 / 21

220 likes | 256 Views

Understand the Taxpayer Relief Act of 1997, featuring Roth IRAs, traditional IRAs, educational incentives, and retirement provisions. Explore new tax benefits and savings programs. Learn about Roth IRA eligibility and contributions.

E N D

Module Objectives • 1997 Taxpayer Relief Act • Review Traditional IRA • Roth IRA • Farmers Annuity Overview • Marketing Roth IRA’s

The Taxpayer Relief Act of 1997 The Taxpayer Relief Act of 1997 is an extensive piece of Federal legislation consisting of 17 different titles and approximately 1,000 pages. This training is a not intended to be legal or tax advice and reflects our current understanding of this new law and is for informational purposes only. You should refer to the Selected Provisions of the TRA ‘97 guide #32-7533 available through Chino for more detailed information. Each taxpayer should consult his or her own tax advisor as to the effect of any particular transaction.

The Taxpayer Relief Act of 1997 The Taxpayer Relief Act of 1997 (TRA ‘97) is the largest tax cut since 1981. The new rules provide may tax benefits for people who want to put away money for their child’s education, for the purchase of a home and for their retirement.

The Taxpayer Relief Act of 1997 • Some principle provisions of the law include: • A $500 per child tax credit, • Educational tax incentives, • Enhancements to IRA programs including new tax-favored savings programs and broader eligibility, • Lower capital gains rates, and • Lower estate and gift taxes.

The Taxpayer Relief Act of 1997 For Parents TRA ‘97 focused on giving relief to families with preschool and school age children. The “middle class” tax cut includes a $500 per-child tax credit and incentives for college education. This represents the largest portion of the tax relief provided by TRA ‘97 in the first five years.

The Taxpayer Relief Act of 1997 For Retirement Savers • TRA ‘97 will allow more flexibility and allow more people to access to IRA tax advantages. The key changes include: • Tax penalty-free withdrawal from IRA’s for qualified higher education expenses and for first-time homeowners. • Extension of tax deductible IRAs to people with higher income levels. • Creation of the Roth IRA to provide earnings potentially free of Federal income tax.

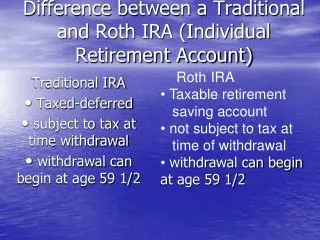

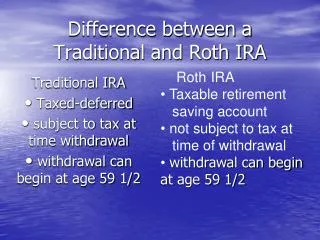

The Taxpayer Relief Act of 1997 Traditional IRA Enhancements • TRA ‘97 allows more people to qualify for deductible IRA contributions and allows money to be withdrawn penalty free if used for college expenses or first homes. • Withdrawals from IRAs are taxable in the year withdrawn. Withdrawals are subject to a 10% penalty-tax unless withdrawn… • after age 59 1/2, or for one of the reasons listed above.

The Taxpayer Relief Act of 1997 The New Roth IRA • The Roth IRA can accumulate tax-deferred and can be distributed income tax free! These features distinguish the Roth from the Traditional IRA: • No tax deduction for contributions to the account • Distribution only required at death • Tax-free accumulation of earnings • Qualified distributions are not included in income • Contributions can be made beyond age 70 1/2 • Distribution is not required at 70 1/2

The Taxpayer Relief Act of 1997 The New Roth IRA Tax-free and penalty-free qualified distribution is possible five years after the first year in which contributions are made, if withdrawn after age 59 1/2, because of death or disability, or for the purchase of a first home.

The Taxpayer Relief Act of 1997 The New Roth IRA Roth IRAs feature Broader Eligibility. There is no age limit for making contributions. The IRA purchaser must have earned income equal to the amount of your contribution up to $2,000 annually for an individual or $4,000 combined for spouses.

The Taxpayer Relief Act of 1997 The New Roth IRA There are different limits on contributions to Roth IRAs. If their Adjusted Gross Income (AGI) exceeds $150,000 and they file jointly ($95,000 for single filers) the amount they may contribute is gradually reduced. The combined total of IRA and Roth IRA accounts cannot exceed the maximum annual contribution of $2,000 per individual.

The Taxpayer Relief Act of 1997 The New Roth IRA TRA ‘97 allows money to be rolled over from Traditional to Roth IRAs. This money will be rolled over without the 10% penalty however, the IRS will treat this as a taxable event. If rolled over before December 31, 1998, the IRS has allowed an individual to pay the taxes over a four year period. In other words, if an individual rolls over $20,000, a total of $5,000 will be added to his/her taxable income for 4 years. (We will discuss in greater detail later…)

The Taxpayer Relief Act of 1997 For Homeowners First time homeowners can make tax favored withdrawals ( subject to a $10,000 limit) from their IRA’s for their down payment. In addition, TRA ‘97 will relieve many people who sell their principle residence of capital-gains taxes (profits) as much as $500,000 for married couples filing jointly and $250,000 for single individuals. This exclusion can be used every two years.

The Taxpayer Relief Act of 1997 For Savers and Investors TRA ‘97 reduces the maximum tax rate on the net individual capital gains from 28% to 20% and from 15% to 10% for sales or exchanges of qualified capital assets after May 1997. The law has increased the holding period required for long-term capital gain treatment from 12 to 18 months. As an example if a taxpayer in the 39.6% bracket who sells an asset which yields $10,000 profit, here is what the capital gains tax could be depending on the holding period:

The Taxpayer Relief Act of 1997 Capital Gains Example:

The Taxpayer Relief Act of 1997 Estate and Gift Tax Considerations The individual exemptions for the unified credit for estate and gift taxes will gradually increase from $600,000 to $1 Million by the year 2006. The gradual phase in of higher tax exemptions will require a careful review of wills, trust and gift giving strategies. (Let’s review a comparison between the Traditional IRA and the new Roth IRA.)

TRA ‘97 Review 1. What are the 5 main provisions of the Tax Payer Relief Act of 1997? • A $500 per child tax credit, • Educational tax incentives, • Enhancements to IRA programs including new tax-favored savings programs and broader eligibility, • Lower capital gains rates, and • Lower estate and gift taxes.

TRA ‘97 Review 2. TRA ‘97 will allow more flexibility and allow more people to access to IRA tax advantages. What are 3 key changes to the new IRA’s? Tax penalty-free withdrawal from IRA’s for qualified higher education expenses and for first-time homeowners. Extension of tax deductible IRAs to people with higher income levels. Creation of the Roth IRA to provide earnings potentially free of Federal income tax.

TRA ‘97 Review • 3. What features distinguish the Roth from the Traditional IRA? Tax-free accumulation of earnings No tax deduction for contributions to the account Distribution only required at death Qualified distributions are not included in income Contributions can be made beyond age 70 1/2 Distribution is not required at 70 1/2

Quote of the Day.. Attitude, Determination and Dedication will guarantee your success. Gung Ho My Friends! Henry Parson