Download

1 / 38

400 likes | 636 Views

CUNA Marketing & Business Development Council Conference Nashville, Tennessee--March 17, 2008. Growth Strategies for Credit Unions. Bob Hoel Filene Fellow. www.filene.org. Good News!. Strong capital—11+% High member satisfaction CU political strengths impress experts

E N D

CUNA Marketing & Business Development Council Conference Nashville, Tennessee--March 17, 2008 Growth Strategies for Credit Unions Bob Hoel Filene Fellow www.filene.org

Good News! • Strong capital—11+% • High member satisfaction • CU political strengths impress experts • CU financial services needed and wanted • Economy in flux—special growth opportunities

“My financial provider does what’s best for me, not just its bottom line.” • A credit union 66% • Regional or local bank 48% • Wachovia Bank 40% • National City 40% • U.S. Bank 36% • Wells Fargo (credit cards) 35% • Washington Mutual (banking & cc’s) 34% • Bank of America (banking) 32% • Chase (banking) 27% • Citibank (banking) 24% • HSBC (credit cards) 24% Source: Forrester Research, 2007, 5005 U.S. Households

“My financial provider does what’s best for me, not just its bottom line.” • USAA 88% • Independent financial advisor 76% • A credit union 66% • A.G. Edwards 66% • Independent insurance agent 64% • GEICO 60% • Edward Jones 59% • AAA Insurance 59% • State Farm 57%

CU Membership GrowthSix Decades U.S. Population

2006 Membership Growth • 55% of CUs under $50 million shrank • 32% of $100+ million CUs shrank • 20% of $500+ million CUs shrank • 30% of $500+ million CUs grew by <1% Source: NCUA & CUNA.

2006 Asset Growth • 63% of CUs under $50 million shrank • 22% of $100 million+ CUs shrank • 14% of $500 million+ CUs shrank • 27% of $500 million+ CUs grew by <2.35% Source: NCUA & CUNA.

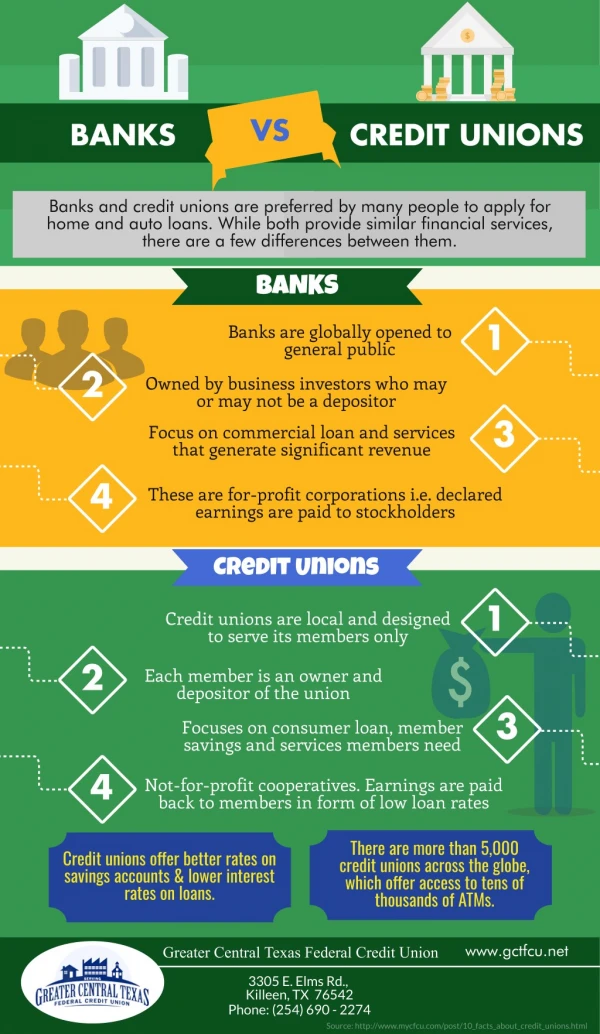

Two Ways to Grow • More Members • More Business per Member

Switch Financial Institutions? • Won’t switch for any amount 41% • For a gift valued at $250+ 33% • For one point higher deposit rate 20% • Ipod 5% • Toaster 1% Source: 2006 IBT/MCA Market Pulse.

Eligible Non-members’ Reasons for Not Joining CU Source: CUNA Survey

Where Americans “Bank” % of U.S. Households Total CU % = 34% Source: J. Lee, Filene Research Institute, 2007

New Filene Studies:High-Growth vs. Low-Growth CUs • Stars vs. Laggards • 3390 mid-size and small credit unions • 5-year period • R. Hoel, “Thriving Mid-size and Small Credit Unions,” Filene Research Institute, 2007 • Big Stars and Laggards • Large credit unions • 5-year period • R. Hoel, Filene Research Institute, study underway 2008

Stars vs. Laggards: 5-Year Asset Growth Group Group

Assets Per CU—Group 50-100(Stars +147%; Laggards +5%; All CUs 56%)

Performance Measures: Group 50-100(Avg. Annual Data: 2001-2005)

Assets per member Loans per member Loans/savings ratio Operating expenses/ average assets Employees per $million in assets Delinquent loans/ average loans Net chargeoffs/ average loans Bankruptcies per 1000 members Other Performance Measures Stars better in all!

1. Stars are highly effective lenders • Loans are the “Golden Goose” • High loan/share ratios • More loans in almost all loan categories • Manageable chargeoffs (not same thing as delinquencies) • Have the “Lending Attitude”

2. Members use CU extensively Per thousand members… • More transaction accounts • More savings accounts • More loans Higher average… • Savings balances • Loan balances

3. Pay higher savings rates • Emphasize CDs and money market funds • Laggards depend more on traditional share accounts • Savings rates higher across almost all savings product categories • Higher rates fuel asset growth

4. Emphasize high-payoffproducts • Used auto loans • Mortgages • 1sts • 2nds • Checking accounts • Savings products

5. Manage expenses aggressively • Low operating expense ratios • Fewer employees... • Per million in assets • Per thousand loans generated • Per thousand members • Lower… • Compensation and fringe costs • Office-operations expenses • Occupancy costs

High average balances = low expense ratio Expense ratio= Operating expense $ Total average assets Best predictor of operating expense ratio: Deposits per member Best predictive model also includes loan/assets ratio, average loan size, real estate loans and CU size.Source: Doyle and Kelly, Predicting and Managing a CU’s Expense Ratio, Filene Research Institute, 2005.

7. Don’t rely only on low loan rates • Convenience • Speed • Good service • Aggressive marketing • Cross selling

8. Usually generate more fee income • High checking account penetration • Other fee-generating products

9. Invest their capital in growth • Instead of building excessive capital, stars invest in… • Membership • Product and service offerings • Growing their asset and loan portfolios “In short, they deliver member value while maintaining adequate net worth levels.”

MH Federal Credit Union • Asset growth rate 20+% • Membership growth rate 20+% • Loan growth rate 25+% • Borrowers/members 92.5% • Return on assets 2.0+% • Net charge-offs/loans <0.25% • Net worth/total assets 6.5%-7.5%

“Premier Account” Package for Every New Member • Standard share account (1%) • “Better than Free” checking account and debit card • 1% interest, free first box of checks, no minimum balance • $100 line of credit tied to the free checking account (covers overdrafts) • Credit card—even low credit scorers get a $100 Visa Classic card • Ala carte relationship with MH CU is not allowed

10% CD for Members 8-18 • Initial deposit is $100 • Maximum balance is $1000 • CD matures on 18th birthday • No interest if withdrawn early • Catches… • In name of the youth—prevents parents from gaming the product • Must attend one 2-hour financial education seminar • Can roll it into an auto purchase or use it for other worthwhile purpose

Loan Deferral Program “Skip a Loan Payment” • Put your loan on “vacation” • $25 charge • Easy form • Not on… • Loans < 6 months old • RE secured loans

Offers Simple Legal Services • Wills • Attorney letters • Referrals

Every Employee Is A Salesperson • External • 1 hour/week minimum • Internal

Keep in Touch & Free Reports… Bob Hoel Filene Research Institute • bobhoel@filene.org • www.filene.org • 608-279-5553 www.filene.org/free/guestpass