Download

1 / 11

110 likes | 252 Views

Buying and Selling non-current assets. Two new ledgers. Open a sundry creditor account (separate to trade creditor) Disposal of Non current Asset. Sale of non-current asset. Not a stock item Requires general journal entry. The General Journal. The General Journal Entries.

E N D

Two new ledgers • Open a sundry creditor account (separate to trade creditor) • Disposal of Non current Asset

Sale of non-current asset • Not a stock item • Requires general journal entry

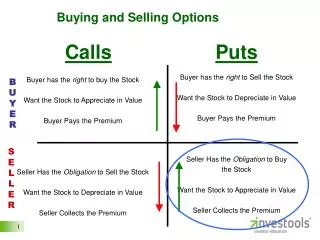

The General Journal The General Journal Entries Buying a Car on Credit

Disposal of Non-current Asset Disposal of Non-current Assets Associated concepts • Historical Cost • Depreciation • Accumulated Depreciation

The end of non-current asset life • Asset may be scrapped • Sold for cash • Traded in on a replacement asset It needs to be removed from the firm’s books

New account – Disposal of NC ASSet Example of a Disposal of Asset Ledger

Disposal of Asset Account • Transfer assets’ historical cost to the Disposal of Asset account • Transfer accumulated depreciation to Disposal of Asset account • Show amount received from sale of asset in Disposal account • Close the Disposal of Asset account to the Profit or Loss on sale of the asset.

Why sell a non-current asset for less than its value? • Item is not popular therefore little demand • May be obsolete technologically (eg computer) • It may be damaged or severely marked The accumulated depreciation may not have been accurate. A loss will be reported as an expense in the Profit and Loss statement

Profit on Sale of Non-current asset • Reported as a profit, under “Other Revenue” in Profit and Loss Statement • Recorded in sundries column in cash receipts journal

Learn the following terminology • Carrying value/book value • Loss on disposal of asset • Proceeds from sale of asset • Profit on disposal of asset • Sundry creditor