Download

1 / 19

320 likes | 880 Views

Working Capital Management. Working Capital refers to a company’s Current Assets Current Assets : Cash and Equivalents, Accounts Receivable, and Inventory Working Capital Management : Applying Investment and Financing Decisions to Current Assets. Investment Decision Applied to Current Assets.

E N D

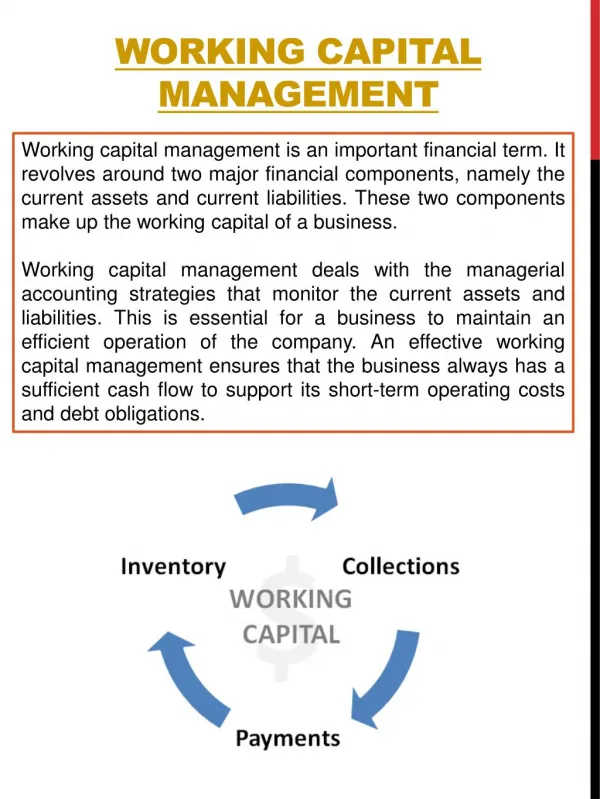

Working Capital Management • Working Capital refers to a company’s Current Assets • Current Assets: Cash and Equivalents, Accounts Receivable, and Inventory • Working Capital Management: Applying Investment and Financing Decisions to Current Assets

Investment Decision Applied to Current Assets • What current assets to own? • We know which ones are needed - we need to know what level of each the firm should have. • How much cash does firm need? • How much accounts receivable should be carried (what is firm’s credit policy)? • How much inventory is needed?

Financing Decision Applied to Current Assets • How to finance current assets? • For most firms, CA exceed CL • Therefore, part of CA is being financed by long-term sources (debt or equity) • How is financing of CA split between short-term sources (CL) and long-term sources ( long-term debt and equity)?

Tradeoffs in Working Capital Management • In making the investment and financing decision for current assets, face tradeoff between • Liquidity: Ability to pay bills, keep sales coming in, keep customers happy, play it safe • Profitability: Size of earnings after taxes

Measuring Liquidity and Profitability • Liquidity: NWC = CA - CL • Liquidity: Current Ratio = CA/CL • Profitability: Return on Total Assets • ROA = EAT/TA • Also use Current Asset Turnover to see how efficiently current assets are used • CAT = Sales/CA

Classifying Current Assets • Permanent Current Assets = minimum level of cash, A/R, and inventory needed to stay in business (PCA) • Temporary Current Assets = fluctuations in cash, A/R, and inventory corresponding to fluctuations in sales (TCA)

Matching Principle of WCM • Match the maturity of the sources of financing (CL, LTD, E) with the maturity of the uses (TCA, PCA, FA) • Use CL to finance TCA • Use LTD & E to finance PCA and FA

Conservative Approach to WCM • Objective: ImproveLiquidity • Level of Current Assets: • 1) Cash: Maintains large cash balance. • Benefit: Able to pay bills easily. • Cost: Cash could be earning a higher rate of return if it was invested elsewhere.

2) A/R: Permits high level of accounts receivable: Liberal Credit Policy (easy to get credit) • Benefit: Keeps sales high, keeps customers happy. • Cost: High bad debt expense.

3) Inventory: Maintains high level of inventory. • Benefit: Keeps sales high, keeps customers happy. • Cost: High carrying costs, funds could earn higher return invested elsewhere

Financing of Current Assets: • Use more long-term financing than the matching principle calls for. • Benefit: Have the money raised all at once and available to spend- no frequent refinancings. • Cost: Long-term debt usually has higher interest rate than short-term debt, pay more interest expense.

Summary of Conservative Approach • Level of CA: High cash, A/R, inventory • Financing of CA: More long-term sources used • Benefit: Increased liquidity • Cost: Decreased profitability

Measures Indicating Conservative Approach • High Level of Net Working Capital • High Current Ratio • Low Return on Total Assets • Low Current Asset Turnover

Aggressive Approach to WCM • Objective: Improve Profitability • Level of Current Assets: • 1) Cash: Keep minimum amount needed. • Benefit: Cash is not in no or low interest accounts, invested elsewhere earning higher rate of return. • Cost: May not be able to pay bills, no extra cash for emergencies.

2) A/R: Keeps receivables low, Tight Credit Policy (hard to get credit from them). • Benefit: Low bad debt expense. • Cost: Unhappy customers, sales drop.

3) Inventory: Minimum investment in inventory. • Benefit: Low carrying costs, money invested elsewhere. • Cost: Unhappy customers, sales drop.

Financing of Current Assets: • Uses more short-term financing than the matching principle calls for. • Benefit: Short-term debt usually carries lower interest rate than long-term debt, lower interest expense. • Cost: Frequent refinancing, may have to borrow at higher rates in future, refinancing risk.

Summary of Aggressive Approach • Level of CA: Low cash, A/R, inventory • Financing of CA: Uses more short-term sources of financing • Benefit: Increased Profitability • Cost: Decreased Liquidity

Measures Indicating Aggressive Approach • Low level of Net Working Capital • Low Current Ratio • High Return on Total Assets • High Current Asset Turnover