Download

1 / 55

550 likes | 715 Views

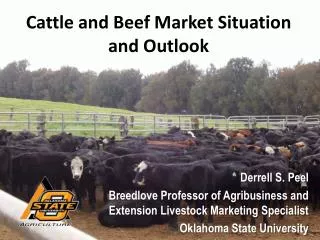

Cattle Industry “Situation and Outlook ” TSCRA March, 2012. 2012 -967,000 Hd. (3%) 2013F Flat. Slaughter Reductions 2013 vs. 2011. 1.4 Million Non-Fed .8 Million Fed 2.2 million Total 8,500/day 2- 4,000+/day packing plants 1-4,000+/day and 4-1,000+/day packing plants. A Long-Term Chart….

E N D

2012 -967,000 Hd. (3%) 2013F Flat

Slaughter Reductions2013 vs. 2011 • 1.4 Million Non-Fed • .8 Million Fed • 2.2 million Total • 8,500/day • 2- 4,000+/day packing plants • 1-4,000+/day and 4-1,000+/day packing plants

A Long-Term Chart… Source: U.S. Dept of Census, various published research estimates

U.S. Dollar Index The weak dollar has stimulated exports

The U.S. exports 18 percent of total red meat and poultry production.

15 billion pounds of U.S. beef, pork and poultry were exported in 2011. 2.8 bilbeef, 5.2 bil pork, 7 bil poultry

Demand Retail- Higher prices will limit movement and featuring. Competition between proteins. Food Service- Improvements noted in SSS. Fast food ,casual dinning, high end. Exports-Slowing YOY gains, Low Dollar, Challenges with access. Imports-Increasing, High domestic prices vs. tighter Global supplies.

2012 Retail Protein Prices Source: USDA and BLS

2012 Fed Price projections based on Changes in Supply and Demand