Download

1 / 50

560 likes | 799 Views

CPE SEMINAR ON Fraud and Money Laundering in the Banking Sector- Bangladesh Perspective. AUTHOR- MD. SYFUL ISLAM, FCA, FCMA 30 November 2008. STRUCTURE OF THE PAPER. Objective of Presentation of the Paper.

E N D

CPE SEMINAR ON Fraud and Money Laundering in the Banking Sector- Bangladesh Perspective AUTHOR- MD. SYFUL ISLAM, FCA, FCMA 30 November 2008

Objective of Presentation of the Paper I being a Professional Chartered Accountant have got plenty of opportunity to work as a Public Accountant in both home and abroad for the last eighteen years, now I am working as one of the Directors of the state owned Bank (Rupali Bank Ltd.) and also having the opportunity of working in the Investigation Task against the Grievous Offences of the country with the Legal Agency of the present Government. Through which I have been able to acquire sufficient practical knowledge and experiences in the field of Accounting, Auditing and Investigations of the malpractices done by the unscrupulous and vested group of people of our society particularly in Banking Sector by which our economy as well as the political situation has come to a very worst condition. As such I would like to express the intention to share my practical experiences through discussion with the honorable Regulatory Authority, Chairmen and Directors of the Public and Private Commercial Banks, the Auditors, General Members of the Institute of the Chartered Accountants of Bangladesh, the Law Enforcing Authority, the Chief Executives and the other High Official of all the Banks, the High Level Executives of the Trade and Commerce Associations with the view to identify the defects or the defaulting activities as are being committed in the Banking Sector of the country for creating awareness of the appropriate authorities of the country to take the Right Steps to Expel and Uprooting of all the Fraud, Money Laundering and other Malpractices from the Banking Sector of our country.

WHAT IS FRAUD The term "Fraud" refers to an intentional and an unethical act by one or more individuals among the management, those charged with the governance, the employees and the third parties to obtain an unjust or illegal advantage causing a material misstatement in the financial statements. The term "Fraud" in relation to the Banks generally refers to manipulation in the Books of Accounts, fraudulent encashment of negotiable instruments, unauthorized handling of the Securities pledged or hypothecated to the Banks, embezzlement, misappropriation of funds, pilferage of cash etc by the Bank employees, account holders and also by third parties.

FEATURES OF FRAUD It is Deceitful It is Intentional It breaches Trust It involves Losses Concealment of Fact Appearance of Outward Respectability

THE CAUSES OF FRAUD ·Absence of social Condemnation; ·Malafide Intention; ·Willful deviation from Laws and Practices; ·Degradation of overall Moral Values; ·Management inefficiency to Withstand Pressure; ·Procedural Lapses/Bottlenecks; ·Organized Crime; ·Corrupt Managers; ·Employee Scams; ·Financial Misstatement; ·False Accounting (e.g., bonus schemes); ·Financial Frauds; ·Computer Hackers; ·Any other significant Corporate Abuse.

TYPES OF FRAUD Consumer FraudCredit Card Fraud KickbacksBid Rigging Inflated InvoicesExternal Fraud Inventory TheftTheft of Cash Basic company FraudsCheque Fraud Identity Fraud Banks Fraud Computer Hacking Financial Statement Fraud Sundry Frauds

THE CIRCUMSTANCES THOSE INDICATE THE POSSIBLE EXISTENCE OF FRAUD • Banking Sector • Limitation of Audit • Unusual Circumstances • Financial Misstatement • Non Cooperation • Non Existence of Good Governance • Abnormalities in the Financial Statements • Abuse of Information Technology Security General Circumstances Behavioral Issues Poor Controls Often Ignored the Straight Information Inconsistencies

Loans & Advances Deposit Accounts Remittances Inter-Branch Suspense Accounts Clearing Nominal Accounts Foreign Exchange Transactions Lockers & Safe Deposit Vaults Cash Shortages FRAUD PRONE AREAS

MONEY LAUNDERING

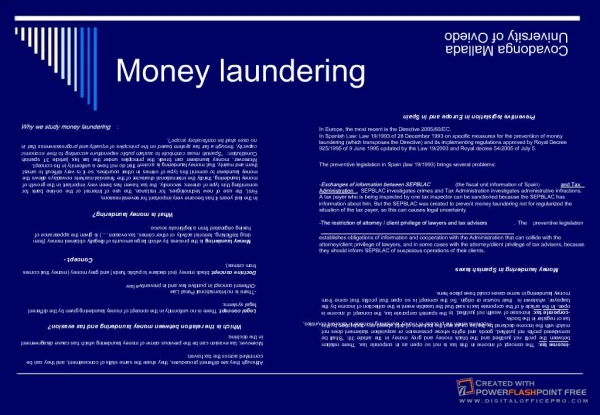

CONCEPTUAL APPROACH OF MONEY LAUNDERING Literally “Money Laundering” is the practice of engaging in specific financial transactions in order to conceal the identity, source and/or destination of money and is a main operation of underground economy. ‘Money Laundering’ as legal term is, which in fact a process of Multi steps but interlinked with one another with the aim of laundering the illegal proceeds. Now- a- days Money Laundering has become a burning issue for economic growth and social security of the nation for the following factors.

Criminals need to conceal the real ownership and origin of the money; They need to control the money; They need to change the form of money; It conceals the true sources of the Funds so that they can be used freely; The concealment or disguise of the true nature, sources, Location, disposition, movement, rights with respect to the ownership of the property. Illicit money is turned into Legitimate useful Funds; The conversion of profits of illegal activities in the Financial Assets, which appear to have Legitimate Origin.

Placement Structuring Layering Integration POSSIBLE STEPS OF MONEY LAUNDERING “Money Laundering” basically involves the following independent steps that often occur simultaneously. These are:

Dormant Accounts Telegraphic Transfers Fund Generation through Non-profit Organization Charitable Organization Abnormal Business Facilities THE POSSIBLE WAYS OF GENERATING TERRORIST FUNDS

METHODS OF MONEY LAUNDERING Establishment of "anonyms" Companies/Firms that operate with normal processes like paying Loans and paying of taxes on profits even though these firms may be non-existent in its operations. Use of over and under invoiced Exports or Imports and creating a cache of Foreign Currency. Cross Boarder Transfers through a set of zigzag patterns.

COMMON SOURCES OF MONEY LAUNDERING Drug Trafficking; Tax Evasion; Organized Crime e.g. Extortion, Prostitution; Loan Sharking, Kidnapping, Contract Killing, Gambling, Adulation, Bank Fraud and Corruption etc.; Slush Funds maintained by the big corporations e.g. Bribery, Payment to the Political Parties, Politicians etc.; Terrorisms; International Traffickers in arms; International Trafficking in human beings smuggling; Smuggling.

Securities Firm Bank The Process Of Money Laundering And Financing Of Terrorism Money Laundering Financing of Terrorism Cash from Criminal Act Legitimate Asset or Cash from Criminal Act $$$$ $$$$ Placement & Structuring Cash is deposited into Account Placement & Structuring Asset deposited into the Financial System Bank Bank Layering Funds moved to other Institutions to Obscure Origin Layering Funds moved to other institutions to Obscure Origin Non-Bank Financial Institution Insurance Company Integration Funds used to Acquire Legitimate Assets Integration Funds used to Acquire Legitimate Assets Legitimate Asset of Distribution

CASE STUDY OF FRAUD AND MONEY LAUNDERING IN THE BANKING SECTOR- BANGLADESH PERSPECTIV Due to some technical reason without mentioning the name of the person and any organization some cases have been stated here under for our better understanding that what illegal ways and techniques are applied by unscrupulous group of people of our society to defalcate of money from the Banking Sector. Issuing of illegal IBDAs (Inter Branch Debit Advices) Issue of illegal IBCAs (Inter Branch Credit Advices) Generation/ Creation of the Fund against Benami Accounts by excessively charging of the Accrued Profit / Interest payment on Deposits Accounts. Creation/ Generation of the fund against Benami Accounts by excessively charging of the Expenditure Accounts. Illegal Transfer of the Branch Investment Profit to Benami Accounts of the Bank Officials, which was earned for the timing gap of the illegal Transaction of the IBDAs and IBCAs for restating the previously Offsetted Loan Liabilities. General Case:

Issuing of illegal IBDAs (Inter Branch Debit Advices) i) Issuing of illegal IBDAs from the Branch: Case No - 1 Suppose that 10 unauthorized IBDAs i.e. without the approval of the Head office for Tk. 10 crore were issued from the “M” Branch of ABCD Bank Ltd. in favour of 10 benami accounts which has been withdrawn in cash Tk. 7 crore and issued 3 pay orders Tk. 3 crore in favour of Mr.Alam Account on “O” Branch of “XYZ” Bank Ltd., a beneficiary of the aforesaid Originating 10 benami accounts from where he withdrawn Tk. 3 crore in cash.

Transaction Profile Suppose that a fund for Tk. 10 crore was createdunder 10 benami / fictitious accounts by issuing 10 unauthorized IBDAs from “M” Branch of ABCD Bank Ltd. by debating Head Office General Account for Tk. 10 crore and crediting Loans and Advance Account for Tk. 10 crore. Step - 1 Cash was withdrawn for Tk. 7 crore and 3 Pay Orders have been issued for Tk. 3 Crore from 10 benami/ fictitious accounts in favour of Mr. Alam Account maintained with “O” Branch of “XYZ” Bank Ltd. by debiting Loans and Advance Account for Tk. 10 crore and crediting Cash and Bank Accounts for Tk. 10 crore. Step - 2 For offsetting the Head Office General Account, Adjustable Blocked Accounts has been debited for Tk. 10 crore and Head Office General Accounthas been credited for Tk. 10 crore. Step - 3 Ultimately in consolidation of the financial statements for clean off this defalcated amount from the records, Profit and Loss Appropriation Account has been debited for Tk. 10 crore and the Adjustable Blocked Account has been credited for Tk. 10 crore. Step - 4

ii) Issuing of the illegal IBDAs from One Branch to another Branch: Case No - 2 Suppose that 25 unauthorized IBDAs i.e. without the approval of the Head Office for Tk. 100 crore were issued from the “L” Branch of ABCD Bank Ltd. to “M” Branch of the same Bank for offsetting of the outstanding Loan Liabilities for Tk. 100 crore of 20 Traceable Accounts of Mr. Monir of “L” Branch, which was disbursed him earlier.

Step - 1 A fund for Tk. 100 crore was disbursed through 20 Traceable Account of Mr. Monir from “L” Branch earlier. 25 IBDAs with different amount were issued in total for Tk. 100 crore on different dates for Offsetting the Loan liabilities for Tk. 100 crore by debiting the Head Office General Accounts and crediting the Inter Branch Transaction (M Branch) Account. Step - 2 For giving the closing entry in “L” Branch, the Inter Branch Transaction (M Branch) Account for Tk. 100 crore has been debited and (Traceable 20) Loan & Advances Accounts (Mr. Monir “L” Branch) Tk. 100 crore has been credited. Step - 3 For responding of the 25 IBDAs Tk. 100 crore issued from “L” Branch, the “M” Branch has debited Loans & advances (25 benami Accounts) for Tk. 100 crore by crediting Inter Branch Transaction (L Branch) Account for Tk. 100 crore. Step - 4 For giving the closing entry in “M” Branch, the Inter Branch Transaction (L Branch) Account for Tk. 100 crore is debited and the Head Office General Accounts for Tk. 100 crore is credited. Step - 5 The illegal Loan liabilities of TK. 100 crore under 25 benami accounts are classified in “M” Branch as Bad Loss Loans for non finding of the beneficiaries of such benami accounts which have been offsetted in consolidation of the financial statements with the Adjustable Blocked Account by debiting the Adjustable Blocked Account and crediting the Loans and Advances Account for Tk. 100 crore. Step - 6 Ultimately in consolidation of the financial statements for Clean off this defalcated amount from the records the Profit and Loss Appropriation Account has been debited and Adjustable Blocked Account has been credited for Tk. 100 crore. Step - 7 Transaction Profile

Issuing of illegal IBCAs (Inter Branch Credit Advices) • Issue of illegal IBCAs (Inter Branch Credit Advices) i) Issuing of the illegal IBCAs from One Branch to another Branch: Case No – 3 Suppose that 25 unauthorized IBCAs i.e. without the approval of the Head Office for Tk.. 100 crore were issued from the “L” Branch of ABCD Bank Ltd. to “M” Branch of the same Bank for offsetting the outstanding Loan Liabilities for Tk. 100 crore of 20 Traceable Accounts of Mr. Bashir of “M” Branch, which was disbursed him earlier.

Transaction Profile Step - 1 A fund for Tk. 100 crore was disbursed through 20 Traceable Accounts of Mr. Bashir from “M” Branch earlier. 25 IBCAs with different amounts were issued from “L” Branch to “M” Branch in total for Tk. 100 crore on different dates by debiting Loans and Advances forTk. 100 crore (against 25 benami Account in “L” Branch) and crediting the Inter Branch Transaction in “M” Branch Account for Tk. 100 crore. Step - 2 For giving the Closing entry in “L” Branch, the Inter Branch Transaction (M Branch) Account has been debited for Tk. 100 crore and the Head Office General Accounts has been credited for Tk. 100 crore. Step - 3 For responding of the 25 IBCAs for Tk. 100 crore issued from “L” Branch, the “M” Branch has debited Inter Branch Transaction (L Branch) Account for Tk. 100 croreand credited the Loans and Advances Account for TK. 100 crore (20 Traceable Accounts of Mr. Bashir for Offsetting of the Loan liabilities of Tk. 100 crore as was given earlier). Step - 4 Step - 5 For giving the Closing entry in “M” Branch, the Head Office General Accounts has been debited for Tk. 100 crore and Inter Branch Transaction, “L” Branch has been credited for Tk. 100 crore. The aforesaid illegal Loan liabilities for TK. 100 crore under 25 benami accounts in “L” Branch have been Classifiedas Bad Loss Loans for non finding of the beneficiaries of such benami accounts for which full provisions have been made by debiting the Profit and Loss Accounts for Tk. 100 Crore and crediting the provisions on Loans and Advances for Tk. 100 Crore. Step - 6 Ultimately, the said Loans and Advances Tk. 100 Crore has been written off in the Accounts by Debiting Provision on Loans and Advances Tk. 100 Crore and crediting Loans and Advances Account Tk. 100 Crore. Step - 7

Generation/ Creation of the Fund against Benami Accounts by excessively charging of the Accrued Profit / Interest payment on Deposits. Case No. – 4 Transaction Profile Suppose that the Actual Interest / Accrued Profit was required to be paid Tk. 100 core but the Interest Accounts/ Profit was charged in the Accounts for Tk. 110 crore by crediting (110-100) Tk. 10 crore to 10 Benami Accounts. Step - 1 Step - 2 Tk. 10 core was subsequently been withdrawn illegally by the dishonest Bank Officials.

4. Creation/ Generation of the fund against Benami Accounts by excessively charging of the Expenditure Accounts. Case No. – 5 Transaction Profile Suppose that the actual Expenditure was Tk. 50 crore but the Expenditure Accounts were charged for Tk. 60 crore by crediting (60-50) Tk. 10 crore to Benami Accounts. Step - 1 Tk. 10 crore was subsequent illegally been withdrawn by the dishonest Bank Officials from the aforesaid Benami Accounts. Step - 2

5. Illegal Transfer of the Branch Investment Profit to Benami Accounts of the Bank Officials, which was earned for the timing gap of the illegal Transaction of the IBDAs and IBCAs for restating the previously Offsetted Loan Liabilities. Case No. – 6 Transaction Profile Suppose that 20 IBDAs were issued for Tk. 30 crore on 1st January 2008 and 25 IBCAs were issued for Tk. 32 crore on 29th January 2008 for the time gap of 29 days. Step - 1 Accounting Entries were made on 1st January 2008 When IBDAs were issued Dr. Head Office General Accounts Tk. 30 crore Cr. Loans and Advances Tk. 30 crore Step - 2 Accounting Entries were made on 29th January 2008 When IBCAs were issued Dr. Loans and Advances Tk. 32 crore Cr. Head Office General Accounts Tk. 30 crore Cr. "X" Benami A/c (instead of Branch Income Account) Tk. 2 crore Step - 3 Withdrawal of the Investment Income Tk. 2 crore from the Benami Accounts by the dishonest Bank Officials by debiting "X' Benami Accounts and crediting the Cash Account. Step - 4

6. General Case: Case No. – 7 i. Illegal Loan Facilities Providing of Loans and Advances to the Entrepreneurs through legal methods of the Bank is one of the regulated Banking Operational Functions of the Commercial Banks. But it has been experienced through some investigations that the influential and the vested group of people of our society and the dishonest Bank Officials jointly defalcate money from the Bank through disbursement of Loans and Advances committing the following irregularities: Payment of Loans before the Sanctioning; Overvaluation of the Property; Overvaluation of the Collateral Securities; Accepting of the Inadequate Securities; Accepting no Securities; Having False Particulars; Improper Documentation;

Inexistence of the Proper Introduction; Unauthorized Cash Payments; Sanctioning of the Loans without the approval of the Competent Authority; False Mortgage of the Property; Accepting of the False Deed Documents of the Property and etc. • Other possible ways of Fraud and Money Laundering. • Use of Over and Under Invoiced Exports or Imports and creating a Cache of Foreign Currency; • Cross Boarder Transfers through a set of zigzag patterns; • False Pay-Order, Demand Draft, Telegraphic Transfer; • False Letter of Credit (Import); • False Import & Export Bills; • Through Capital Flight; • Through Nostro Accounts.

A Simple Example of Transaction of Money Laundering Transaction Profile for Tk. 90 crore which was defalcated through Money Laundering by issuing of 90 illegal IBDAs from X Branch of DD Bank Ltd. OVERSEAS ACCOUNT Tk. 100 (25+75) crore BANGLADESH DD Bank Ltd. CC Bank Ltd. X Br. Issued 90 IBDAs for creating Tk. 90 crore by crediting 25 fictitious CD A/Cs Z Branch Issued pay orders for Tk. 10 crore Transferred from Y Br. Tk. 25 crore Y Br. Transferred from Z Br. Tk. 10 crore Transferred from X Br. Tk. 90 crore Total 100 crore Withdrawn & transferred by Y Branch Tk. 75 crore to overseas account

ECONOMIC AFFECTS

ECONOMIC AFFECTS OF FRAUD AND MONEY LAUNDERING The Bad money can gradually turn out the good money. There are other negative Micro Economic Consequences for example, It could compromise Bank soundness with potentially large fiscal Liabilities lessen the ability to attract the Foreign Investment, and increase the volatility of money flows and exchange rates. In this era of Technological Development in almost all the aspects and very high capital mobility, financial crime makes National Tax Collection and the Law Enforcement more difficult. the Financial system abuse the Financial Crime and Money Laundering may also be distorted the allocation of wealth and can be costly to detect and eradicate.

CURRENT SITUATION IN BANGLADESH FOR PREVENTING CRIME OF FRAUD AND MONEY LAUNDERING Bangladesh Penal Code, Foreign Exchange Regulations Act- 1947 (FERA) Income Tax Ordinance- 1984 Money Laundering Prevention Act- 2002 (MLPA) and Anti- Corruption Commission (ACC) Act- 2004, the Bank Companies Act- 1991 and The Companies Act - 1994 are the suitable Laws to prevent such crimes. While there is always scope for improvement in the Legal Framework, the blame cannot be impute squarely on those Acts and Regulation. We do not have a functioning Financial Intelligence Unit (FIU) that can collect information, the capability to analyze the same and identify specific cases and trend of committing Fraud,Money Laundering, Defalcation and other Financial Crimes. Our Investigation Agencies are not well trained with adequate knowledge and procedures to investigating Financial Crimes/ Corporate Corruptions and File Cases. Our Prosecutors and the Legal System look understanding of the complexities involved in the Financial Crimes.

However, since 1/11 Anti-Corruption Drive in Bangladesh Got Momentum The Corrupt People are Under Legal Scrutiny The Financial Intelligence Unit (FIU) in Bangladesh Bank is working with the help of US Embassy The Cooperation Agreement with the Other Central Banks are Needed to carry out the investigation work against money laundering.

Effective Anti Money Laundering Mechanisms invariably include co-operation between the Bank Management, Regulators (i.e. the Central Bank) and the Law Enforcement Agencies. Therefore it is in the best interest to develop the interaction and co-ordination among the above parties.

MINISTRY OF FINANCE • The Banking Wing of the Ministry of Finance need to be strengthened with the Independent Professionals for Research and Developed Standard Operating Procedures, Monitoring and Compliances; • Constitute an Independent Body to monitor Debt Management, Recovery, Bad Debt, Written Off Loans and Advances and involvement of the Financial Scam of the Banks and other Financial Institutions; • A 3 Member High Power Committee may be formed in the Bank for evaluating the performances of the Board of Directors. The Members of the Committee shall be one from the Bangladesh Bank holding the position of at least Executive Director, one member from the Director of the Board and one from the Ministry of Finance holding the position of at least Joint Secretary; • Further amendment of the Bank Companies Act (amendment act of 2003) and the Bangladesh Bank (nationalization) order (2003) so that the Govt. owned Banks come under the sole supervision and regulation of Bangladesh Bank instead of the Ministry of Finance, and strengthening oversight through Appropriate Reformation of the Bangladesh Bank.

BANGLADESH BANK Organizational Issues Functional and Operational Issues Accounting and Financial Reporting Issues

Organizational Issues • Induction of the Professionals in the Board of Directors of Bangladesh Bank from the Private Sector to ensure that at least one each from Business, Economics, Chartered Accountants, Legal and Engineering background discouraging the appointment of the Retired Bureaucrats. • Ensure that Cash Dividend/Bonus shares and Incentive Bonus to employees not paid / issued out of Artificial Profit created by undercharging of the Expenditure and/or under -provision of the Classified Loan Loss and over accruing of the Investment Income or other Operating Income; • The terms and conditions of the Board of Directors of the Bangladesh Bank shall be Redefined emphasizing of close monitoring on the present state of Malpractices, Money Laundering and Defalcation of money from the Banking Sector in Bangladesh;

Bangladesh Bank should be kept free from all Political pressures. • Legal and Operational Independences of Bangladesh Bank should be ensured; • Establish an Ethical Standards Committee (ESC) in every Banks for ensuring of - The Ethical Standards are carefully developed and are firmly in place; The Ethics Officer and other key players have well-defined roles and are discharging their responsibilities properly; The Employees are behaving in an Ethical Manner as defined by the Organization; The organization is complying with all the Laws, Regulations, and Rules that affect it; There is a system in place for resolving Ethical Dilemmas; There is an effective and Robust System of compliance checks in place and all Significant Problems are reported to the ESC.

Functional and Operational Issues The tools and instruments used by the Department of the Offsite Supervision (DOS) and the Department of Banking Inspection (DBI) shall have to be upgraded and new effective Tools and Instruments i.e. new Measures to be introduced which are very capable to Controlling and finding out the Fraudulent Activities as are now being Committed in the Banking Sector; A Separate Management Audit Cell (MAC) may be established headed by the Governor of the Bank for checking and verification of the performance of the DBI and DOS Personnel on Regular Basis; Departmental Head, Dealing Boss and the other officers and staff of the DBI, DOS and the proposed Management Audit Cell should be changed with in 2 years. Accountability of all officers and staff of the Bank shall have to be established through necessary Amendments in the existing Bangladesh Bank Order-1972 (President's Order no.127 of 1972) and the Bangladesh Bank's (Nationalizations) Order 1972 (President’s Order no. 26 of 1972)

Accounting and Financial Reporting Issues • Accounting and Financial Reporting Policy as outlined in the BRPD Circular no. 14 dated 25 June 2003 issued by the Bangladesh Bank shall be redefined in line with the IASs, as adopted by the ICAB; • Bangladesh Bank shall redefine the Accounting and Financial Reporting Policies of all the Banks and the Financial Institutions in line with the best practices and ensure the Public Disclosure; • Establishing an Ethical Standards Committee (ESC) for adopting the Corporate Code of Ethics for the Board and the Management and ensuring the compliance thereof as part of their Employment Contract; • Ensuring induction of at least 2(two) independent Directors in the Board of Directors in every Banks and Financial Institutions (except the borrower, political allegiance and those who held office of profit from the Bank) one of them should have Economic back ground and another should be a Chartered Accountant having sufficient knowledge of the Banking and the other Financial Institution affairs ; • Adopting the policy of submitting quarterly Classification of Loans (CL) Statements to Bangladesh Bank along with the External Auditors reviewing Report thereof.

MANAGEMENT OF THE BANK • Board of Directors • The Board of Directors shall morally be obliged to carry out their responsibilities as outlined by the Regulatory Authority and the Controlling Authority. • Managing Director • Ensure the preparation of the Accounts and the Financial Reporting of the Bank which in compliance with all the BASs and the BFRSs as adopted by the ICAB and as per the BRPD Circular no. 14 dated 25 June, 2003; • Ensure of the Inter Branch Transaction Accounts which to be reconciled every week; • Ensure that the Rules of the Money Laundering Prevention Act-2002 which have been complied accurately in all the Branches of the Bank; • The Internal Audit Department should be kept free from the control of the Management. They should be allowed to report their actual findings to the Audit Committee;

One (1) Chartered Accountant should be appointed in every Bank as the Head of the Internal Control and Compliance Department for carrying out the Internal Audit in compliance with the Bank Companies Act- 1991, Rules, Regulations and Circulars issued by the Bangladesh Bank and the Office Circulars as issued by the Management from time to time; Confirm that of the Internal Audit Department which makes their report on the following Core Risks Management: Credit Risk Management; Assets Liabilities Risk Management; Prevention of Money Laundering; Internal Control and Compliance Management; Foreign Exchange Risk Management; Information and Communication Technology Management One (1) Chartered Accountant should be appointed in every Bank as the Head of the Financial Control Department for maintaining the Books of Accounts, preparation of Financial Statements and Reporting in compliance with the BASs and BFRSs adopted by the ICAB and in compliance with the Bank Companies Act-1991, Companies Act-1994, the Securities and Exchange Commission Rules-1987, Rules, Regulation and Circulars issued by Bangladesh Bank.

Each and every big Branch of the Bank should have a "Audit Cell." The Audit Cell at the end of the Transaction hours of each and every day will check the Vouchers/ Transaction of all the Risky Sectors such as; Credit related Transaction and Vouchers; Cash Payment Vouchers; Out ward Clearing Special Monitoring Cell regarding the big amount of Loans to be created in each and every Branch / Regional Office / Head Office. Special care for regular monitoring to be taken at the Regular Interval. Board Audit Committee may over see the Monthly Report of this Cell. The Beneficiaries of the Bank Guarantees (up to certain amount) may be sent to the Head Office for verification / reconfirmation; Cheque Frequency Machinery must be available in the big Branches; Verification of the Land and Building Documents to be done by the Government approved Surveyor. A certificate from the Surveyor / Branch should be obtained stating that the properties are in the possession of the Mortgagor; Ensure of the decentralization of the Inter Branch Clearing Work; Ensure of the Reconciliation of the Nostro Accounts timely etc.

The Institute of Chartered Accountants of Bangladesh (ICAB) Being the member of the IFAC the ICAB shall take necessary steps immediately to adopt the following pending issues for keeping the Members with the up to date knowledge of the present requirement of the IFAC: ISA (International Standards on Auditing) ISAs - 701 Modifications to the Independent Auditors Report. IAPS (International Auditing Practice Statements) IAPS - 1006 Audits of the Financial Statement of Banks IAPS - 1012 Auditing Derivative Financial Statements Being the Regulatory Body of the Chartered Accountants the Institute shall ensure that its members have been rendering their Professional Responsibilities in compliance with its By-laws and the Council Directives. The Institute shall also ensure that its members have been rendering their Professional Responsibilities in compliance with BASs and BFRSs and BSAs and BAPSs and in compliance with the section 39(3) Kha of the Bank Companies Act-1991 and the other applicable section of the Bank Companies Act-1991, the Rules, Regulations and the Circulars issued by the Bangladesh Bank, the Companies Act- 1994, the Securities and Exchange Commission Rules-1987, the Income Tax Ordinance-1984 and the other applicable Rules and Regulations.

Quality Control Department The Institute shall have a Quality Control Department through which it can exercise to Close Monitoring, Supervising, Reviewing, Controlling and maintaining the quality of audit of Banks and Financial Institutions as audited by its auditors. Investigation and Disciplinary Committee The Institute should strengthen its Investigation and Disciplinary Committee for taking proper action against the Auditors those who have failed to conduct the Audit of the Banks and the Financial Institutions in compliance with the Bangladesh Standards on Auditing (BSAs), BFRS, BAPS and in compliance with the applicable section of the Bank Companies Act -1991, the Rules and Regulations issued by the Bangladesh Bank, the Companies Act-1994, the Securities and Exchange Commission Rules 1987, the Income Tax Ordinance 1984 and the other applicable Rules and Regulations and those who have also violated the By- laws of the Institute of Chartered Accountants of Bangladesh and the Coun1cil Directives.

Before conclusion, I would like to express my sincere thanks and gratitude to some of the middle level and high officials of the present Govt. and also to some high officials and auditors of DBI & DOS of Bangladesh Bank for their kind cooperation and support in discharging my professional responsibilities successfully as mentioned at the out set of my speech.