Download

1 / 19

220 likes | 360 Views

Systematic Investment Plan Concept Demystified. You must have heard this statement more than n times now that … “SIP is the best investment style” So let’s understand why SIP has emerged as the most powerful style of investing in recent times through some real life examples….

E N D

You must have heard this statement more than n times now that … “SIP is the best investment style” So let’s understand why SIP has emerged as the most powerful style of investing in recent times through some real life examples….

There are basically three points that makes SIP such a strong concept • Rupee Cost Averaging • Power of Compounding • Market timing irrelevance Let us simplify these terms in next few slides…

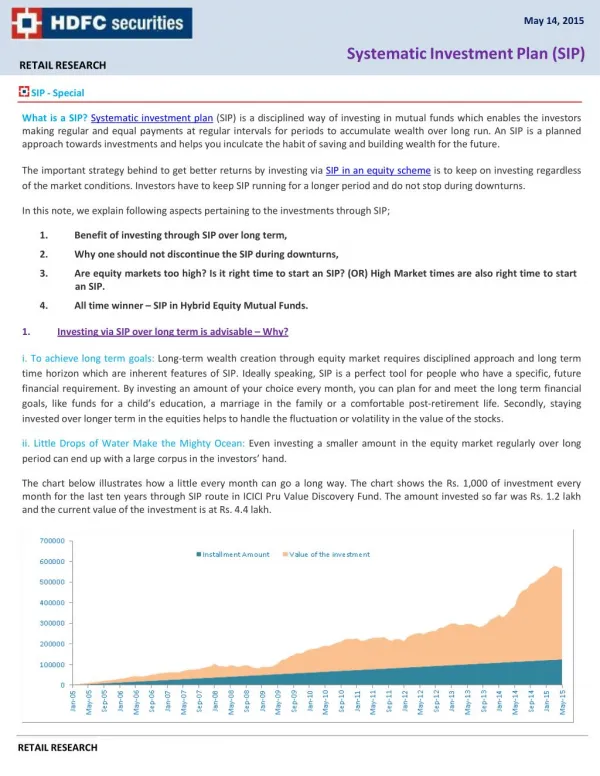

Rupee Cost Averaging To understand this concept more practically look at the illustration below. The SIP investor finishes with an investment that is worth more than the lump sum investor after six months - even though the starting price and finishing price are exactly the same. Unlikely but it is true. Check the figures yourself ….This is the first thing what SIP does; it averages the buying cost automatically.

This mathematical formula of compounding : FV = PV (1 + r) nis known to all of us but is seldom understood in terms of investing. Let’s use an example : If you invested Rs. 100000 PV (Present Value) in a instrument that grows @ 15% per year (the r) for a period of 25 years (the n), its FV (Future Value) will become Rs.3291895. Unbelievingly the amount multiplied to a whopping 33 times Power of Compounding Now the let’s see how the same compounding plays in a SIP over a period of time. The table below justifies all statements of the Power of Compounding. A meager amount of Rs. 1000 per month over 25 years at an annualized growth rate of 15% accumulates to a humongous number of approximately Rs. 33 lakhs

Market timing is irrelevant Data Source : Bloomberg Let’s look at the above analysis in the next slide whether it actually happens …

Time in the market matters; not timing Data Source : Bloomberg *CAGR (Compound Annual Growth Rate) -The year-over-year growth rate of an investment over a specified period of time

Now that we have seen the Power of SIP; let’s try to address this point … “When SIP works best for us” Few slides from hereon will explain this more clearly

SIP will work best if following acts are done: • Start Early • Invest Regularly • Invest for Long Term • Invest in the Right Asset Class • Let’s look at each aspect from a practical angle…

Start Early – Let’s flip around and see Cost of Delay through “Ram aur Shyam ki Kahani” RamShyam • Starts investing at the age 28 48 • Monthly Investments Rs.5,000 Rs.15,000 • Returns (assumed) p.a. 15% 15% • Both invest till the age 58 58 • Total investment 18,00,000 each • Accumulation at 58 350.49 lacs 41.79 lacs To catch up with Ram, Shyam has two choices Earn on his investment OR Save per month @ 45% p.a. Rs. 1,25,000

Invest for Long Term Data Source : Bloomberg • Lower the risk • Greater the effect of compounding • More predictable average returns Hence longer your SIP Period

Invest in the Right Asset Class Undoubtedly Equity is the winner overtime…

Now that we have seen why and how SIP can best work - a question still remains unanswered …. Can SIP help individuals like you and me in real life situation to meet our financial goals ? Let’s try to answer this question through a simple case study and see whether benefits of SIP really work …

Case Study – Real Life Situation • Assume – • You are 30 yrs of age; have a wife and kid • Current Annual expenditure of Rs. 5,00,000 • Retirement expected at age 60 yrs • More – • Average prices (i.e. inflation) will rise by 7% pa • After 30 yrs when you retire, the low risk rate of return will be 6% pa (Considering you put all your accumulated corpus post retirement in a bank deposit) • You will live for more 20 years post retirement So let’s see what will be the corpus required at the time of your retirement to maintain the same current lifestyle additionally with enhanced medical expenses

Your Target Current Expenditure Rs.5,00,000 p.a. Inflated at 7% p.a. for 30 years Expenditure at the time of Retirement Rs. 36,00,000 p.a. Therefore to generate this income every year post retirement you need to accumulate a corpus Income to be generated post Retirement Rs. 36,00,000 p.a. Your first reaction Impossible! It cannot be achieved. But then there is a solution… Corpus Required at the time of Retirement 8 crore

So what’s the Solution… Just one simple thing Subscribe for an SIP of Rs.15,000 per month in a good diversified equity fund for 30 years and forget it • You still don’t believe it that it can be that simple; let us validate our conviction with actual returns generated in a equity fund over the years • From the table it is crystal clear that if an investor did an SIP of Rs.15000 per month in HDFC Equity Fund for 15 years, he would have invested 27 lacs and that would have grown to a whopping number of 3.4 crore as on date; in spite of so many pitfalls in equity markets in last 15 years.

Time to Retirement (yrs) 30 25 15 10 Investment Required Monthly 15,000 21,000 48,000 80,000 Annual 1,80,000 2,32,000 5,76,000 9,60,000 Still need to think; No pressure but see this what the delay can cost in the same case study Today After 5 years from now After 15 years from now After 20 years from now With every passing year the time to retirement is reducing and increasing the burden of investment required. Now the choice is our whether we want TO START NOW OR STILL WAIT Current Age : 30 years Retirement Age : 60 years Retirement Corpus to be accumulated : 8 cr. Assumed Rate of Return on Investment : 15% p.a.

We're here to help 1800-11-0444 rrinvestors@rrfcl.com www.rrfcl.com www.rrfinance.com