Download

1 / 35

370 likes | 477 Views

Thinking Outside the Stocks: The Private Equity Ecosystem. Thunderbird School of Global Management. April 2008. Presented by. JORDAN ROBINSON Vice President, Global Private Equity AIG Investments. This material must be read in conjunction with the Disclosure Statement. Agenda.

E N D

Thinking Outside the Stocks:The Private Equity Ecosystem Thunderbird School of Global Management April 2008 Presented by JORDAN ROBINSON Vice President, Global Private Equity AIG Investments This material must be read in conjunction with the Disclosure Statement.

Agenda • I. Where Are We Today? - Current Market Conditions • II. Portfolio Building Blocks • III. Where Are We Going Tomorrow? - Looming Questions • IV. Where We You Going Tomorrow? - Job Search Thoughts

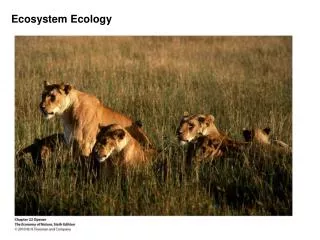

The Ecosystem Private equity has developed a true ecosystem ec·o·sys·tem [ek-oh-sis-tuh m] –noun: the complex of a community of organisms and its environment functioning as an ecological unit

Record Global Fundraising 14.5% 9.3% 9.5% 72.5% 76.6% 75.6% 4.9% 3.8% 75.3% 78.4% 13.0% 14.1% 14.9% 19.8% 17.8% Source: Venture Economics, EMPEA

Emerging Markets Fundraising Source: Emerging Markets Private Equity Association. Data as of March 2008.

Allocations: expected to increase Despite the recent slowdown in private equity deal-making, strong fundraising is expected to continue, driven by increasing allocations to private equity by institutional investors LPs planning to increase their private equity allocations over the next 12 months (Winter 2005-2006 to Winter 2007-2008) Current and Expected Allocation to Private Equity Source: Coller Capital Global Private Equity Barometer Winter 2007-08, Citigroup Global Markets CIO Survey September 2007.

Purchase prices pre-2008: have increased Average LBO Purchase Price as a Multiple of Non-adjusted Pro Forma Trailing EBITDA for Total Sources of $500 million or More 9.87 6.28x for $250-499 MM 8.51x for $250-499 MM 8.46 8.42 7.52 6.91 6.70 6.68 6.40 40.6% 40.0% 39.5% 35.1% 32.1% 33.6% 32.9% 37.8% Source: Standard & Poor’s. As of December 31, 2007.

Purchase prices in 2008: have declined Comparable Deal Analysis Industry #2 in Mkt. Share (Revenues $10-20 Bil) Industry #3 in Mkt. Share (Revenues $5-10 Bil) x 14.5x Senior Debt 46.1% 6.7 EBITDA L + 170 9.6x 35.5% (And all asset backed) 3.4x EBITDA L + 200 Sub Debt 22.5% 3.2x EBITDA Rate: 9% 1.6x EBITDA Rate: 12.5% 16.1% 48.4% Equity 31.4% What a difference a year makes!!! Sources: AIG Internal Data

Convergence: has slowed • Private equity & hedge fund convergence has slowed • Concerns about liquidity (hedge funds) • Uncertain inflows (hedge funds) • Concerns about portfolios (private equity)

Global Summary • Lots of committed capital • Access to credit acute for large transactions • Convergence has slowed down • Emerging markets are hot • Returns holding up (so far)

Ecosystem Private equity has matured into a true ecosystem ec·o·sys·tem [ek-oh-sis-tuh m] –noun: the complex of a community of organisms and its environment functioning as an ecological unit

Club Deals Funds Flows China Distressed Debt Credit Statistics Convergence Succession KKR IPO Alpha Greed Brazil Activist Investors Overhang Short Durations India “Fire inthe Belly” LBO PurchasePrices Redemptions Leverage BDCs Beta

Portfolio Company Lifecycle • Private equity investments address opportunities across company lifecycles Buyouts Venture Capital • Seed Stage • Early Stage • Late Stage • Pre-IPO • Growth • Leveraged Buyouts • Distressed/“Turn-Around”

A Broad Menu of Private Equity Strategies Indirect Other Direct Indirect • Real Estate • Bridge Funds • Distressed Debt • Fund of Funds • Secondaries • Co-Investments • Buyouts • Venture Capital: Early Stage • Venture Capital: Late Stage • Growth Equity • Co-Investments (Direct) • Natural Resources • Infrastructure • Turnaround • Mezzanine

The Direct Investment Process is Relevant to Every PE Segment ResearchInsight-Driven Deals Portfolio Management/Value Creation Structuring/Negotiations Due Diligence Exit Access/Origination • Research/Insight-Driven Deals – Top-to-Bottom; Opportunistic • Access/Origination – Information Arbitrage • Due Diligence – Intense Scrutiny • Structuring/Negotiations – Governance; Shareholder Rights • Portfolio Management/Value Creation – Management Oversight, Investor Add-Value • Exit – Timing; Multiple Options (IPO, Strategic Sale, Structured Arrangement)

Secondary Investment Process – Key Beneficiary of the Ecosystem Development • Knowledge - Primary fund commitments, Co-investments, direct equity investments and mezzanine debt, Emerging markets direct investments • Insight – Industry Performance, Sectors, Regions, Facilitators, Blockers • Relationships - General Partners (quality of portfolio, transfer process efficiency), Limited Partners (Awareness of deals, Ability to negotiate) Global Secondary Investments • Relationships Information Expertise

Analysis Framework Macroeconomic and capital market conditions Private equity capital flows – segment, sector, country Manager quality and availability Fundraising cycles Regulatory environment Performance cycle analysis Portfolio Construction – Creating an Investment Framework Develop a macro “point of view” Analyze available manager opportunity set Investment Framework Rigorous analysis with flexibility to capture attractive investment opportunities as they present themselves

Building a Private Equity Portfolio Strategies Direct Indirect

Building a Private Equity Portfolio Strategies Direct Indirect

Building a Private Equity Portfolio Strategies Direct Indirect

Building a Private Equity Portfolio Strategies Direct Indirect

Building a Private Equity Portfolio Strategies Direct Indirect

Emerging Markets Hot Macro Environment • Compelling GDP growth • Stability of Political, Legal and Accounting Characteristics • Trade Interdependence and Surpluses • Lower/Stable Inflation and Interest Rates • Improved Credit Ratings Emerging Markets: Attractive PE Opportunity • Emerging markets companies competing and winning globally • Capital markets growing quickly • Strong IPO receptivity; Strategic Acquisitions • Market correlations are lower • Less competition (despite recent fundraisings) • Large opportunity set

PE in Asia: Asset Class Penetration Potential PE Deal Value as a % of GDP 6.9x 3.9x Source: Bain study. Data as of end 2006.

100% Top Five 19% 80% Top Five 51% 60% Others 40% 81% Others 49% 20% 0% Brazil EU-25 Brazil – How to access these growing markets? Sugar Industry Market Share in 2005 Ibovespa Index Capital Goods & Services Construction & Transportation Basic Materials Basic Materials Consumer Cyclical Source: F.O. Licht and LMC International. Consumer Non-Cyclical Brazil Credit Card Market Basic Materials & Energy account for 57% share of the Ibovespa index Telecom Energy Financial Source: Bovespa. Source: Bank of Brazil and Brazilian Association of Credit Card Companies and Services.

Building a Private Equity Portfolio Strategies Direct Indirect

Is Now a Good Time To Invest In Private Equity? • Market dislocations create opportunity for private market investors • Private equity should generate a significant premium over public market equities Source: Cambridge Associates, pooled mean and median net IRR to limited partners by vintage year as of 9/30/07.

How will $500 Billion in Dry Powder Be Spent? Emerging Markets ? New Markets PIPES Base Old New Old Products

Competition: Are Sovereign Wealth Funds Changing the Game? Sources: World Economic Forum, Thomson Financial

Where are You Going Tomorrow? Job Search Thoughts • Focus on satisfaction, right motives • Private Equity is endgame; Doesn’t need to be first career move • Experience not brand • Industry or regional expertise helpful to eventually develop • The Ecosystem has much to offer

Private Equity Endnotes • Interests in open funds (“the Funds”) are offered only pursuant to the terms of a Confidential Private Placement Memorandum (the “Memorandum”), which is furnished to qualified investors on a confidential basis for their consideration in connection with the private offering of limited partnership interests (the “interests”) in the Fund. The Information contained in this presentation may not be reproduced or redistributed without the written approval of AIG Investments. • No person has been authorized to make any statement concerning the Funds other than as set forth in the Memoranda, and such statements, if made, may not be relied upon. The information contained herein is qualified in its entirety by the more complete information contained in the Memoranda. This presentation is not an offer to sell or a solicitation of interests in the Funds. The Manager, its affiliates and AIG Equity Sales Corp. make no representation as to the accuracy or completeness of the information contained herein. • Additionally, investors should note the following regarding private equity investments: • They are not subject to the same regulatory requirements as mutual funds, including mutual fund requirements to provide certain periodic and standardized pricing and valuation information to investors; • They are speculative and involve a high degree of risk; • Investors could lose all or a substantial amount of their investment; • Interests may be illiquid and there may be significant restrictions in transfer. There is no secondary market for interests, and none is expected to develop; • They may be leveraged, and their performance may be volatile; • They have high fees and expenses that will reduce returns; • They may involve complex tax structures; • They may involve structures or strategies that may cause delays in important tax information being sent to investors; • They and their managers/advisers may be subject to various conflicts of interest; • They may hold concentrated positions with a limited number of investments; • They, or their underlying fund investments, may invest a substantial portion of their assets in non-U.S. securities, which could mean higher risk; • The list set forth here is not a complete list of the risks and other important disclosures associated with such investments and is subject to the more complete risk and disclosures contained in the applicable confidential offering documents; • The investment manager has total trading authority over fund investments. The use of a single adviser applying generally similar trading programs could mean lack of diversification and, consequently, higher risk. • Certain materials contained herein constitute “projections,” “forecasts” and other “forward-looking statements” relating to certain investments and do not reflect actual results. These projections, forecasts and other forward-looking statements are based primarily upon applying assumptions retroactively to certain historical financial information relating to the investments. The projections, forecasts and other forward-looking statements presented herein are, therefore, valid only as of the date shown on the front page of this presentation. • AIG Equity Sales Corp., member FINRA, is acting as a placement agent for the Funds in the United States only. AIG Investments Web Address: www. aiginvestments.com Rev. 11/05/07

Disclosure Statement • AIG Investments Europe Limited is authorised and regulated by the Financial Services Authority ("FSA"). In the UK this communication is a financial promotion solely intended for professional clients as defined in the FSA Handbook and has been approved by AIG Investments Europe Limited. • AIG Global Real Estate Investment (Europe) Ltd. is an Appointed Representative of AIG Investments Europe Limited. • Approved by AIG Investments Ireland Limited and AIG Investments Fund Management Limited, both regulated by the Financial Regulator in Ireland. • In Australia, this document is intended for a limited number of wholesale clients as such term is defined in chapter 7 of the Corporations Act 2001 (CTH). The entity receiving this document represents that if it is in Australia, it is a wholesale client and it will not distribute this document to any other person whether in or outside of Australia. • AIG Global Investment Corp. (Middle East) Limited is regulated by the Dubai Financial Services Authority. In Dubai this document is intended for wholesale customers only and not Retail Customers and the financial products and services to which this material relates will only be made available to wholesale customers who meet the regulatory criteria to be treated as a client of AIG Global Investment Corp. (Middle East) Limited. • AIG Investments is a group of international companies that provide investment advice and market asset management products and services to clients around the world. • AIG Investments is a service mark of American International Group, Inc. (AIG). Services and products are provided by one or more affiliates of AIG. • Readership: This document is intended solely for the addressee(s). Its content may be legally privileged and/or confidential. • Opinions: Any opinions expressed in this document may be subject to change without notice. We are not soliciting or recommending any action based on this material. • Risk Warning: Past performance is not indicative of future results. Our investment management services relate to a variety of investments, each of which can fluctuate in value. The value of portfolios we manage may fall as well as rise, and the investor may not get back the full amount originally invested. The investment risks vary between different types of instruments. For example, for investments involving exposure to a currency other than that in which the portfolio is denominated, changes in the rate of exchange may cause the value of investments, and consequently the value of the portfolio, to go up or down. In the case of a higher volatility portfolio the loss on realization or cancellation may be very high (including total loss of investment), as the value of such an investment may fall suddenly and substantially. • In making an investment decision, prospective investors must rely on their own examination of the merits and risks involved. • Unless otherwise noted, all information contained herein is sourced with AIG and/or AIG Investments internal data. • The content included herein has been shared with various in-house departments within the member companies of AIG Investments and/or AIG Private Bank Ltd., in the ordinary course of completion. All AIG Investments member companies comply with the confidentiality requirements of their respective jurisdictions. • Parts of this presentation may be based on information received from sources we consider reliable. We do not represent that all of this information is accurate or complete, however, and it may not be relied upon as such. • AIG Global Investment Corp. (Switzerland) Ltd. is a wholly owned subsidiary of AIG Private Bank Ltd. AIG Investments Web Address: www. aiginvestments.com Rev. 7/13/07