Download

1 / 31

310 likes | 394 Views

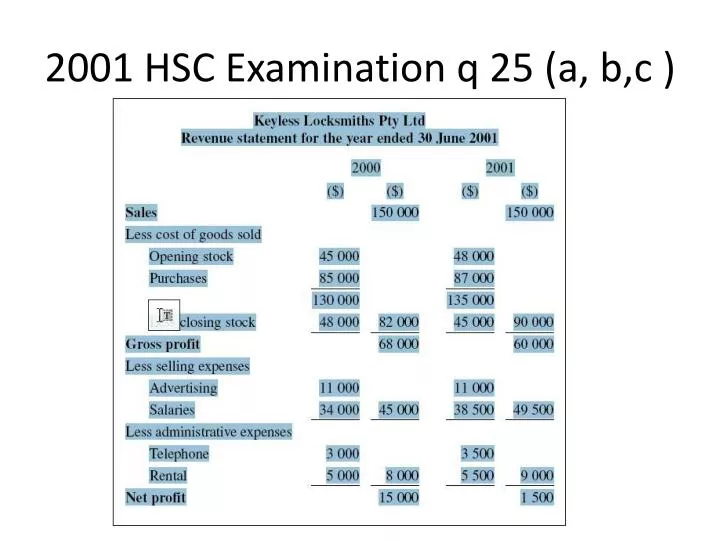

2001 HSC Examination q 25 (a, b,c ). Calculate the gross profit ratio for 2001. (Show all working.). Calculate the gross profit ratio for 2001. (Show all working.). GP = GP x 100 sales 60000 = 40 % or .4: 1 150000

E N D

Calculate the gross profit ratio for 2001. (Show all working.)

Calculate the gross profit ratio for 2001. (Show all working.) • GP = GP x 100 sales 60000 = 40 % or .4: 1 150000 The decline in profitability from 10 % in 2000 to 1 % in 2001 could have been due to two of the following

The net profit ratio has decreased from 10% in 2000 to 1% in 2001. State TWOpossible reasons for the change in profitability.

The net profit ratio has decreased from 10% in 2000 to 1% in 2001. State TWOpossible reasons for the change in profitability. • The decline in profitability from 10 % in 2000 to 1 % in 2001 could have been due to two of the following: • An increase in the selling expenses such as salaries which increased from S34 000 in 2000 to $ 38 500 in 2001 • An increase in administrative expensese such as telephone or rental , which both increased by $ 500.

Propose and justify TWO marketing strategies that Keyless Locksmiths Pty Ltdcould adopt to improve their profitability.

Propose and justify TWO marketing strategies that Keyless Locksmiths Pty Ltdcould adopt to improve their profitability. • Keyless Locksmith could improve profitability by adopting any of the strategies in the 4 Ps • Change the brand name and image to clearly distinguish the product against the competition • Change the way prices are set • Change the advertising campaign to reach a larger market • ( link these to profitability by making explicit the reduction of costs or the increase in sales)

2003 HSC q 22 • Ajax Computers Ltd is considering making a takeover bid for a controlling block • of shares in Gigabyte Computers Ltd. The financial report obtained from • Gigabyte Computers includes the following information: • • Return on owners’ equity has averaged 10% for the past two years • (industry average is 15%). • • The accounts payable turnover period is 37 days (credit period is • 21 days). • • Inventory turnover has increased from 27 days to 35 days in the last • 12 months. • • Plant and equipment is valued at $1.75 million. • • The current ratio is 1.5 : 1 (industry average is 2.5 : 1).

Outline TWO indicators of problems with effective cash-flow managementexperienced by Gigabyte Computers Ltd.

Outline TWO indicators of problems with effective cash-flow managementexperienced by Gigabyte Computers Ltd. • The following are possible responses • Poor current ratio of 1.5 : 1 compared to industry average of 2.5: 1 so the value of current assets such as cash at bank has decreased • Long accounts payable turnover period of 37 dats when the credit polciy is 21 days so the customers are not adhering to the business’s credit policy • Stock turnover has slowed down from 27 days to 35 , tying up more funds in stock for a longer period

Explain ONE strategy that Ajax Computers Ltd could implement to improve theprofitability of Gigabyte Computers following the takeover.

Explain ONE strategy that Ajax Computers Ltd could implement to improve theprofitability of Gigabyte Computers following the takeover. • Make the link between profitability and increasing sales or reducing costs explicit. • Possible strategies include : reducing expenses , reducing the amount of stock held to reduce COGS , boost net profits , increasing sales to improve gross profit and net profit

The accounts of Wizard Pinball Manufacturing Pty Ltd include the following information • Accounts Payable 180 000 • Accounts Receivable 80 000 • Cash 20 000 • Intangibles 50 000 • Inventories 150 000 • Mortgage 250 000 • Overdraft 70 000 • Plant and Equipment 300 000

Calculate and interpret the current ratio of Wizard Pinball Manufacturing Pty Ltd.

Calculate and interpret the current ratio of Wizard Pinball Manufacturing Pty Ltd. • 80 000 + 20 000 +150 000 180000 +70 000 250 000 = 1 250000 1 This means that for every one dollar of current assets there are one dollar of current libailities

Describe ONE method that could be used to control inventory at Wizard Pinball

Describe ONE method that could be used to control inventory at Wizard Pinball • Just in time • Electronic scanning - quick and efficient re ordering • Computerized inventory policy – stock levels are monitored by staff to re order

Analyse how the use of factoring and leasing could change the working capitalposition of Wizard Pinball Manufacturing Pty Ltd.

Analyse how the use of factoring and leasing could change the working capitalposition of Wizard Pinball Manufacturing Pty Ltd. • Factoring is a process whereby accounts receivables are sold to a finance company. In order to receive the value of the accounts receivable now ( except for a fee). This means that the firm has funds available for it to pay its financial obligations at they fall due , current liabilities will be reduced hence improving the liquidity of the firm. • Leasing is the process of renting machinery , vehicles, premises instead of buying them right out. This frees up cash which can be out to other uses such as reducing the overdraft or paying the accounts payables.

Financial ratios for Maurice’s Trading Companyfor 2004 and 2005 • 2004 2005 • Current ratio 2:1 1:1 • Gross profit ratio 35% 35% • Net profit ratio 30% 25% • Accounts receivable 12 times 6 times • turnover ratio per annum per annum • Return on owner’s equity 15% 10%

State ONE reason for the change in the net profit ratio for Maurice’s TradingCompany, and propose ONE strategy to deal with this situation.

State ONE reason for the change in the net profit ratio for Maurice’s TradingCompany, and propose ONE strategy to deal with this situation. • One possible reason is that expenses have increased . This could include such things as telephone and electivity costs rent increases and advertising costs . Strategies would include: • Reducing the expenses of the business – cutting wages by reducing staff or cutting back overtime, find alternate and cheaper sources of ………………

Analyse the effect on working capital of TWO changes in measures of efficiencyfor Maurice’s Trading Company

Analyse the effect on working capital of TWO changes in measures of efficiencyfor Maurice’s Trading Company • Two measures of efficiency are the expense ratios and the accounts receivables turnover ratio • The a/ r turnover ratio fell from 2004 and 2005. The customers are paying their debts less frequently and so money is coming in at a slower rate . This influences liquidity because it means that the business may not be able to meet its financial obligations when they fall due because they have not received the accounts which are due. • The expense ratio looks at how expensive it is for the business to sell its products. The lower the ratio the better because the firm is able to generate profits with lower costs. The business will have funds available to settle their accounts as they fall due.

Pizza & Pasta Restaurant Industry • Revenue statement year ended 30 June 2006 average • $ $ • Sales 150 000 200 000 • Cost of goods sold 105 000 100 000 • Gross profit 45 000 100 000 • Operating expenses • Administrative 5 000 12 000 • Selling & distribution 7 000 15 000 • Financial 3 000 3 000 • Net profit 30 000 70 000

Identify and calculate ONE profitability ratio for Pizza and Pasta Restaurant

Identify and calculate ONE profitability ratio for Pizza and Pasta Restaurant • Use either the gross profit ratio or the net profit ratio • Gross Profit 30 % 45/150 • Net profit 20 % 30/ 150

Explain the purpose of comparative ratio analysis for a business.

Explain the purpose of comparative ratio analysis for a business. • In order to fully evaluate the results of a business a comparison needs to be made either against similar businesses , over time or against industry standards . The information gained is then used to inform business practices.

Evaluate TWO ways the owners of Pizza and Pasta Restaurant could use the financial information provided in the revenue statement to improve profitability.