Download

1 / 58

580 likes | 592 Views

This article discusses the five major forces driving change in the Australian Agrifood sector, including the impact of supermarket oligopoly, the rise of private labels, global competitiveness, and corporatization and technology. It explores the effects of these forces on the industry and highlights the challenges faced by food producers and processors. The article also examines the implications for consumer choice, job loss, and the competitiveness of the Australian market.

E N D

Five forces of change in the Australian Agrifood sector • Dr David McKinna • July 2013

The agrifood sector is undergoing its biggest shift in history . . . . . . and regional Australia is feeling the impact!

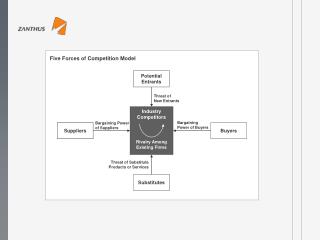

2 Private Label Renaissance 1 Supermarket Oligopsony 4 Corporatisation & technology 5 Water 3 Global competitiveness This change is being driven by 5 forces . . . with apologies to Michael Porter

1 Supermarket Oligopsony

Collectively Coles and Woolworths account for 70%+ of retail food sales

The ‘big two’ are in a head-to-head battle • Aggressive price negotiations to achieve deep cost cuts. • Range rationalisations • Supply chain restructuring e.g. primary freight • Differentiating fresh food offering • Locked Down Low Prices • Sophisticated data mining tools • Revamp of private label offering • British management at Coles ruthlessly pursuing performance targets.

Large scale food producers have no option but to roll the dice with the devil

Most major food companies have over 60% of their business with Coles and Woolworths

Down, down, down goes category value • Category value is being destroyed • Profitability is declining for all processors • Reduced investment in R&D and innovation • Product de-engineering • Multinationals are rewriting their Australian strategies • SMEs are a threatened species – many are in receivership

Supermarkets are using smart cards to build data bases on shopper behaviour

Supermarkets don’t profit more from their power • Consumers are the main beneficiaries of the price war - at least in the short term. • This is why ACCC wont step in. • Supermarket margins are low, they work on shopper traffic and volume. • In the longer term, consumers will have less choice and many Australians will lose their jobs.

Most food companies have had enforced price cuts despite significant cost increases

Over the past three years Australian consumers have enjoyed a 4% deflation in food prices!

$ 1Milk has resulted in a transfer of value of approximately $2 billion p.a from processors and and producers

Processor margins are not sufficient to support the reinvestment needed to remain globally competitive

“The Australian market is the worst market . . . (to do business in)” Bill Johnson Heinz Global Chair

2 Private Label Renaissance

Based on overseas markets, private label market share is likely to grow Australia 1/4 USA 1/3 UK More than 1/2 28

Private label is seriously eroding the value of most food categories • It is benchmarked against market leaders, • Sold at 30-50% discount. • Takes shelf space from proprietary brands. • Proprietary brand owners are forced to discount to protect market share and shelf-space. • The profit margins for producing private label are razor thin. • For products that can be economically shipped, there is direct competition from low cost imported product.

Valrhona Chocolate Simon Johnson $21.95 Private Label Chocolate Aldi $2.49

Strong proprietary brands generate the margins required to fund innovation and category growth 32

3 Global competitiveness

In most agrifood products with a high labour component, Australia is hopelessly uncompetitive

Factors in Australia’s lack of competitiveness • Labour • Input costs • Energy - electricity has gone up 40% in 3 years • Flow-on effects of carbon tax • Compliance • Freight and logistics • Disposal of trade waste

The weighted average labour cost in a processing plant is:Australia: $56 per hourNew Zealand: $18 per hour China: $4 per hour

Freight and distribution costs are higher than manufacturing for bread Goodman Fielder cost breakdown for bread: Source: AFR, 11 February 2012

$AUD needs to be around 70-80c to the $USD for Australia to be competitive.Economists predict it will stay at around 90c for the next five years

The free trade agenda benefits some industries at the expense of others

For multinationals, margins are no longer sufficient to manufacture in Australia 40

4 Corporatisation& technology

The critical importance of scale • Major improvements in overhead recovery • Farms have to double in size every 10 years to produce the same income. • Farm productivity is growing at 2% PA. • Commodity prices are cyclical but on average are not keeping up with inflation rates.

Demand for capital is driving corporate farming models Corporate models demand: • Scale • Geographic spread • Production volume • Capital • Best practice technology and IP • Logistics capability • Tight cost control

In most horticultural industries fewer than 8 businesses supply 70+% of the market

There is a growing interest in Australian agrifood assets by foreign investors • They see assets agrifood assets as undervalued • Anticipate growing demand for food • Expect long term capital gains • Ensuring food supply for sovereign needs

Technology reduces need for labour • Direct seeding • Large GPS controlled machinery • Robotics • Self-guided vehicles • Drones • Smart phone apps

Because of efficiency, corporatisation can be profitable and substantially reduce costs Smaller farm businesses aren’t viable at these prices

5 Water