Download

1 / 11

110 likes | 317 Views

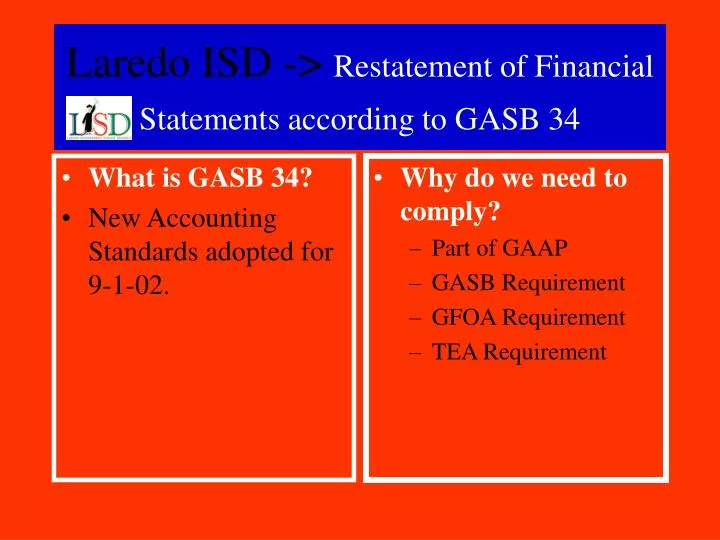

What is GASB 34? New Accounting Standards adopted for 9-1-02. . Why do we need to comply? Part of GAAP GASB Requirement GFOA Requirement TEA Requirement. Laredo ISD -> Restatement of Financial Statements according to GASB 34. New Financial Statement Only reported at year end

E N D

What is GASB 34? New Accounting Standards adopted for 9-1-02. Why do we need to comply? Part of GAAP GASB Requirement GFOA Requirement TEA Requirement Laredo ISD -> Restatement of Financial Statements according to GASB 34

New Financial Statement Only reported at year end Accounts Activities of Primary Government Total Assets $160,708,139 Total Liabilities $123,637,904 Net Assets $37,070,235 Statement of Net Assets Exhibit 1

New Financial Statement Only reported at year end Accounts for revenues and expense activities Reports cost of government Reports Net change in assets Total Expenses –net of grants and contributions $109,563,705 Total revenues $122,573,265 Net Assets change $13,009,560 Statement of Activities Exhibit 2

- Capital Assets $36,586,154 Certain bond costs not recorded at fund level $39,750 Receivables collected but deferred $3,530,623 Change in receivable accounts due to changes in deferred revenues $-26,458 Long term liabilities not recorded in the current period $106,138,501 Reconciliation of Balance sheet to Net Assets Exhibit 5

Capital outlay exceed depreciation $5,966,469 Deferral of revenues for current activity $129,474 Expenses deferred in govt wide financials $258,283 Bond proceeds exceed repayments $3,553,862 Expenses not requiring the use of current resources $66,208 Expenditures and Changes in Fund Balance of Government Funds to Statement of Activities Exhibit 5

Only General Fund meets the criteria to be reported as a Major Fund 10% of assets and liabilities of each type of government -enterprise fund AND greater than 5% of total assets , liabilities of the district. Major Programs

Step 1 record capital assets Step 2 record Acc. Dep. Step 3 record Long term debt Step 4 record interest payable Step 5 record begin-deferred revenue Step 6 (ISF) N/A Step 7 record current asset additions and reverse capital outlay Step 8 record asset depreciation activity Journal Entries that affected Statement of Net Assets and statement of Activities Exhibit 4

Step 9 record fixed assets deletions under $5,000 Step 10 record transfer of capital assets Step 11 reverse principal payment for bond reduction Step 12 record current year interest expense Step 13 reclass capital expenses Step 14 capitalize QZAB issuance costs Step 15 record current bond issuance Continued

Step 16 record new loan Step 17 reverse bond proceeds Step 18 recognize change in deferred revenue (G/F) Step 19 recognize change in deferred revenue (D/S) Step 20 eliminate inter-funds transactions Step 21 reclassify current portion of long term liabilities Step 22 reclassify fund balances to net assets Step 23 record capital appreciation Step 24 reclassify unspent bond proceeds Continued

Staff resources: Director of Accounting Staff and Senior Accountants Fixed Assets Coordinator CFO Padget , Strateman LLP Other Resources: T.E.A. FASRG GASB 34 Manual Staff sources: Food Services Director Transportation Director Risk Management Coordinator Internal Auditor Resources and Training

Cost of conversion Audit Cost $5,000 Training Cost $1,500 Inventory Cost $25,000 What is Next? Submission to TEA, GFOA, Financial Rating Agencies, Data Depositories Summary