Download

1 / 2

20 likes | 113 Views

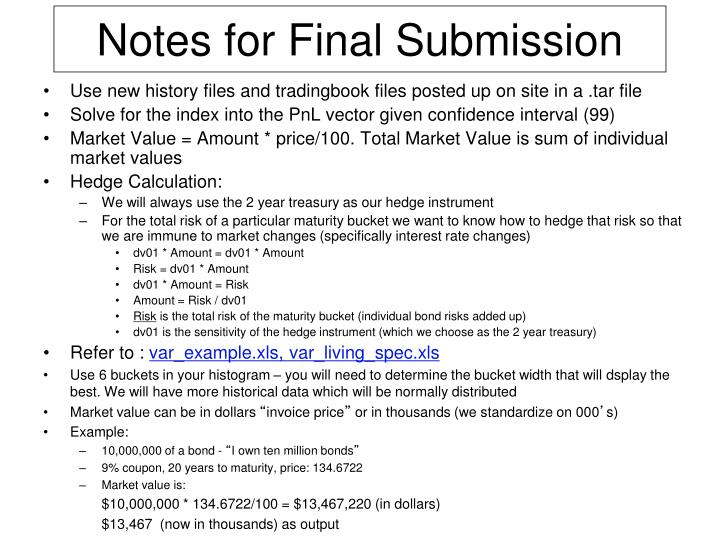

Notes for Final Submission. Use new history files and tradingbook files posted up on site in a .tar file Solve for the index into the PnL vector given confidence interval (99) Market Value = Amount * price/100. Total Market Value is sum of individual market values Hedge Calculation:

E N D

Notes for Final Submission • Use new history files and tradingbook files posted up on site in a .tar file • Solve for the index into the PnL vector given confidence interval (99) • Market Value = Amount * price/100. Total Market Value is sum of individual market values • Hedge Calculation: • We will always use the 2 year treasury as our hedge instrument • For the total risk of a particular maturity bucket we want to know how to hedge that risk so that we are immune to market changes (specifically interest rate changes) • dv01 * Amount = dv01 * Amount • Risk = dv01 * Amount • dv01 * Amount = Risk • Amount = Risk / dv01 • Risk is the total risk of the maturity bucket (individual bond risks added up) • dv01 is the sensitivity of the hedge instrument (which we choose as the 2 year treasury) • Refer to : var_example.xls, var_living_spec.xls • Use 6 buckets in your histogram – you will need to determine the bucket width that will dsplay the best. We will have more historical data which will be normally distributed • Market value can be in dollars “invoice price” or in thousands (we standardize on 000’s) • Example: • 10,000,000 of a bond - “I own ten million bonds” • 9% coupon, 20 years to maturity, price: 134.6722 • Market value is: $10,000,000 * 134.6722/100 = $13,467,220 (in dollars) $13,467 (now in thousands) as output

Notes for Final Presentation • Name your team • Roles in the team • Client-side language and tool choice • Demo client side • Include entering a spread of 50bp in the 30 year bucket • Shift up and and down • Highlight your use of graphics • Take one question from me • Each team will pick one other team that they think presented the best: • Quality of presentation • Quality of the product