Download

1 / 13

130 likes | 141 Views

Learn how to use cash flow and discounting techniques to value future cash flows, and understand the importance of time value of money in short-term decisions. Apply the NPV technique to select value-enhancing proposals and see how short-term decisions fit with EVA. Also, discover how to value changes in the cash conversion period and recognize difficulties in selecting an appropriate discount rate.

E N D

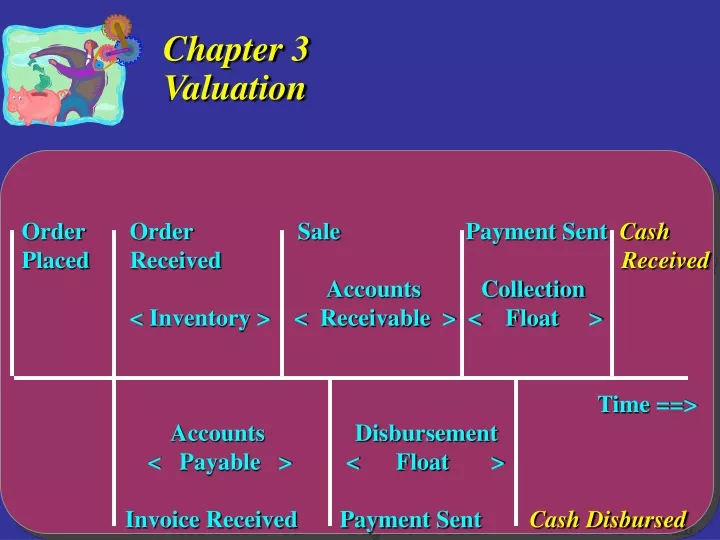

Chapter 3Valuation • Order Order Sale Payment Sent Cash • Placed Received Received • Accounts Collection • < Inventory > < Receivable > < Float > • Time ==> • Accounts Disbursement • < Payable > < Float > • Invoice Received Payment Sent Cash Disbursed

Objectives • Use cash flow timeline and discounting techniques to value future cash flows. • Explain importance for using time value of money in short-term decisions. • Apply the NPV technique to select value-enhancing proposals. • Explain how short-term decisions fit with EVA. • Apply NPV to value changes in the cash conversion period. • Recognize difficulties in selecting appropriate discount rate.

Two Financial Decision-Making Approaches • Financial statement approach • Valuation approach

Financial Statement Approach • Approach • compute incremental revenue and expense effects of proposal • calculate anticipated profit effect • Calculation steps • estimate unit sales and multiply by profit margin • estimate capital costs of additional required investments such as receivables, inventory, etc. • estimate additional bad-debt loss if new credit terms • calculate overall profit effect • Decision criteria • if anticipated profit is >=0, proposal would contribute profit • if anticipated profit is <0, proposal would not contribute profit

Valuation Approach • Approach • accounts for timing of cash flows • accounts for present values • results in making value enhancing decisions • Four steps • determine relevant cash flows • determine timing of cash flows • determine appropriate discount rate • discount cash flows • Decision criteria • if NPV >= 0 invest • if NPV < 0 do not invest

Economic Value Added • Incorporates elements from both financial statement approach and valuation approach • EVA = Operating profit(1-T) - (Cost of capital)(Capital employed) • Advantage: provides better company-wide understanding of importance of improved working capital management • Caution: can be misused if user does not take a long-term view

NPV Calculations • Simple interest • 1PV = FV x ------------------- k (1 + (------) x n) 365 • Compound interest • 1 PV = FV x -------------- k (1+ -------)n 365

........ Basic Valuation Model note: i = k/365 CFo CF1 CF2 CF3 CFn CF1 CF2 CF3 CFn NPV = CFo + ------------- + ------------- + ------------ + .... + ------------ (1 + i x 1) (1 + i x 2) (1 + i x3) (1 + i x n)

Valuation Using NPV • Solving DigiView’s financial dilemma

Valuing Changes in the Cash Conversion Period • - Purchase Sale NPVCCP = --------------- + ---------------- (1 + i ) DPO (1 + i) DIH + DSO • NPV CCP-Aggregate = NPVCCP x Daily Sales / i • - Purchase Sale NPVCCP = [ -------------- - --------------- ] ln(1 + i) (1+i)OC-CCPP (1+i)CCPO+DPO

Corporate Cash Holdings and Value • Late 80’s to mid 90’s: keep cash holdings low • long-term cost of funds > return on cash • cash holdings viewed as negative debt • Late 90’s to current: bond rating agencies penalizing for too little liquidity • Current trend: reduce working capital requirements but increased cash holdings • Pinkowitz and Williams (2002): investors mark up stock value $1.26 per $1 of cash holdings

Choosing the Discount Rate • Three unique problems • funds are rarely raised specifically to fund short-term type projects • short-time horizon implies short-term not long-term rate • risk should be accounted for, but may be ambiguous. • One-shot projects • if net borrower, use short-term borrowing rate • if net investor, use short-term investment rate • Multi-year projects • maybe appropriate to use cost of capital • Formulation • kadj = krf + kavg + k

Summary • Short-term financial decisions can impact firm value by: • altering operating cash flows • changing the length of the cash conversion cycle • changing company risk posture • impacting net interest income • and by changing accuracy and timeliness of critical information. • Both financial statement approach and valuation offer insight in working-capital management decisions. • Choosing appropriate discount rate is an issue when trying to assess valuation impact.