Download

1 / 83

830 likes | 998 Views

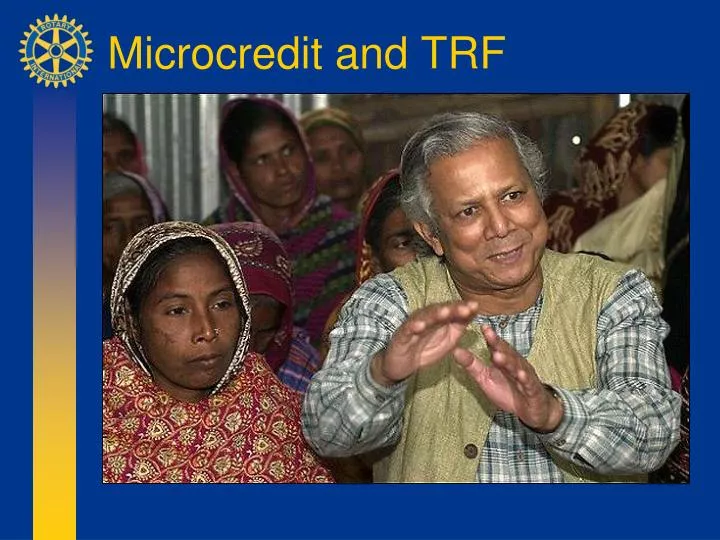

Microcredit and TRF. Microcredit and TRF. At the 1999 RI International Convention Prof. Muhammad Yunus received the ‘Rotary Award for World Understanding’.

E N D

Microcredit and TRF • At the 1999 RI International Convention Prof. Muhammad Yunus received the ‘Rotary Award for World Understanding’. • In 2006, he and the Grameen Bank received the Nobel Prize “for their efforts to create economic and social development from below”. • Microcredit is now known world-wide.

Microcredit and TRF • TRF uses the term “Revolving Loans”. • There is no special Revolving Loan Fund grant from The Rotary Foundation. • A Revolving Loan project is simply one eligible activity under 3-H, Matching, and District Simplified Grants.

Microcredit and TRF • The earliest known TRF grant for microcredit was part of a 3-H Grant in Bangladesh in 1981. • At least 25 3-H Grants have included microcredit components since then.

Microcredit and TRF • It is unclear when the first Matching Grant for microcredit was awarded. • About 400 Matching Grants have been awarded for microcredit since 1992.

Microcredit and TRF • TRF grants (3-H, MG, DSG) are intended to support Rotarians in two of the ‘Four Paths of Service’: Community, and International Service. • For this reason grants are only awarded to Rotary Clubs or Districts, for projects initiated and controlled by Rotarians.

TRF Revolving Loans Policy • Commitment “The Rotary Foundation has a commitment to microcredit, village banks and other programs to facilitate small economic self-help enterprises. “It is the policy of the Foundation to support microcredit and revolving loan funds as an important and successful mechanism to alleviate poverty.”

TRF Revolving Loans Policy • 1. Club Initiatives “Clubs and districts are encouraged to establish their own* revolving loan programs, whether they involve money, animals, equipment, or other types of loan programs, as a way of undertaking sustainable development projects.” * Emphasis added

TRF Revolving Loans Policy • 2. Grants for Capital “Grant funds may be used for revolving loan capital for up to US$10,000 per credit group. “One grant may support multiple credit groups.”

TRF Revolving Loans Policy • 3. Administrative Expenses “Grant funds may be used for Rotary club and district start-up costs to support revolving loan projects until the loan fund is self-sustaining.”

TRF Revolving Loans Policy • 4. Use of Interest and Fees “Interest and fees generated by revolving loan fund capital may be used for administrative expenses that support the revolving loan project.”

TRF Revolving Loans Policy • 5. No Loan Guaranty Systems “The Rotary Foundation will not fund loan guaranty systems.” (Grant funds should be used as loan capital, not placed on deposit to guarantee loans from another source.)

TRF Revolving Loans Policy • 6. Training and Payback Schedules “Revolving Loan grant projects must include training and detailed information regarding recipient payback schedules.”

TRF Revolving Loans Policy • 7. Credit Group Agreements “Grant sponsors must adopt a Revolving Loan Fund Agreement for each credit group before funds are released for that credit group.” Each agreement specifies loan policies for that credit group, including interest rates, loan amounts, and payback schedules.

TRF Revolving Loans Policy • 8. Continuity Plan “Grant sponsors must adopt a continuity plan to ensure that capital from The Rotary Foundation continues to be used for revolving loans after reporting to The Rotary Foundation has stopped.”

TRF Revolving Loans Policy • 9. Review by Cadre “Grant applications for revolving loan projects must be reviewed by the Cadre of Humanitarian Grants Advisors.” The cadre look for technical soundness and long-term viability prior to approval.

TRF Revolving Loans Policy • 10. Reporting Requirements Each annual grant report must include a Report Supplement describing the use and recovery of the loan funds. Grant funds for loan capital must be loaned at least twice before the grant can be closed.

TRF Revolving Loans Policy • 11. Ultimate Disposal of Funds “In the event that the Rotarian project sponsors decide to discontinue the revolving loan fund, the loan capital is to be returned to The Rotary Foundation.”

TRF Revolving Loans Policy • 12. Cooperating Organizations “Supervision and control of the project must rest with the club or district. “The organizations must meet the requirements of The Rotary Foundation and significantly involve Rotarians in the activities.” [Note: Grant funds may not be donated to another organization]

Eligible Expense Direct lending of funds Ineligible Expense Cash donations to individuals or other organizations TRF Revolving Loans Policy

Eligible Expense Short-term or contracted labor for project implementation Ineligible Expense Salaries for individuals already working for another organization[unless the salary is fully attributable to the Rotary project] TRF Revolving Loans Policy

Eligible Expense Administrative expenses for project activities Ineligible Expense Normal ongoing operating or administrative expenses of another organization TRF Revolving Loans Policy

TRF Revolving Loans Policy • Closing the Grant • TRF considers a grant completed and ready to close if all of the capital has been loaned, repaid, and loaned again. • TRF reserves the right to audit any grant project, even after it has been “closed”. • Any cooperating organization must agree to allow its related accounts to be audited.

TRF Revolving Loans Policy • TRF requirements (summary): • An Application Supplement, including • Assurance that this is a Rotary service project • Plans for training • A continuity plan • A technical review by Cadre • A Credit Group Agreement for each group • A Report Supplement • The return of capital after the initiative

District Simplified Grants • District Simplified Grant (DSG) funds may be used for revolving loans. • However, the time needed to implement and report on a revolving loan project makes this activity inconvenient for the one-year DSG reporting cycle. • DSG-funded revolving loan projects also require Cadre review before implementation.

Practical Considerations • Microcredit is a form of banking, and requires specialized experience. • Microcredit is more labor-intensive than normal banking. Multiple small loans require multiple loan agents. • Loan agents must also provide training.

Practical Considerations • Most microcredit programs are run by “Microfinance Institutions” (MFIs) • 3,100 MFIs world-wide are now serving 100 million at the “bottom of the pyramid” • Some microfinance institutions are even competing against each other for clients.

Practical Considerations • Most TRF Revolving Loan grant projects involve partnering with an MFI. • Rotarians should carefully consider the experience and capacity of potential MFI partners (there are agencies that rate the capacity and performance of MFIs). • A written Memorandum of Agreement with the MFI is strongly recommended.

Practical Considerations • Investors are now joining donors and development agencies in providing funds. • An estimated $4 billion is currently invested in microfinance, with a potential market demand estimated at $300 billion. • Investors prefer to support established, sustainable MFIs.

Practical Considerations • To become sustainable, an MFI must have enough capital on loan to generate enough income to cover costs. • This requires that interest rates should be at or above normal market rates. • It also requires economies of scale to break even.

Practical Considerations • Industry experience says it can take about US$250,000 in working capital to break even. • Microfinance Institutions with less than US$1 million are considered “small” • A $10,000 revolving loan fund is not generally considered sustainable.

Practical Considerations • Most MFIs focus on the less-poor.

Practical Considerations • The poorest of the poor often do not have the ability to participate in microcredit. • This population needs basic services first – potable water, food security, basic health. • These services can be provided through TRF grants, laying the foundation for microcredit projects.

The Future of Microfinance • Savings and loans(most common) • Electronic fund transfers(new technology) • Life & health insurance • Property & disability insurance • Micro-franchising • Bottom-of-the-pyramid ‘social businesses’

Alternative Approaches • There is no one ‘correct’ way to structure a Rotary microcredit project. • There are, however, some ‘incorrect’ ways to do it.

Model 1 Credit Groups funded and serviced by Rotary Club (hard work) Rotary Club

Model 2 Credit Groups serviced by MFI, funds from Rotary Club (caution!) Microfinance Inst. Rotary Club

Model 3 Rotary Credit Groups funded by Rotary Club, serviced under contract by MFI Microfinance Inst. Rotary Club

Model 4 Credit Groups serviced and funded by MFI, support services from Rotary Club Microfinance Inst. Rotary Club

Case Study # 1 • Club plans to lend to 20 individuals • Estimates $350 per individual loan • Requests $7000 for revolving loan capital • Club will provide training and mentoring

Case Study # 1 • Club plans to lend to 20 individuals • Estimates $350 per individual loan • Requests $7000 for revolving loan capital • There is no “revolving” in this project. • If capital is re-loaned, they will need at most only half of the total amount, $3500, to accomplish the same thing.

Case Study # 2 • Three MFIs are successfully providing loans and other services in the area • Rotarians want to get involved • Rotarians submit a grant request for loan capital

Case Study # 2 • Three MFIs are successfully providing loans and other services in the area • Rotarians want to get involved • Rotarians submit a grant request for loan capital • There is no need for the Rotary Club to compete in the loan business. Support services may be more appropriate.

Case Study # 3 • Club will deposit $10,000 with local financial institution • Club will identify loan applicants • Financial institution will make loans • At end of project $10,000 will be returned

![[CRF] = Q.R.W [TRF]](https://cdn2.slideserve.com/4138927/slide1-dt.jpg)

![[CRF] = Q.R.W [TRF]](https://cdn2.slideserve.com/5156157/slide1-dt.jpg)