Download

1 / 24

240 likes | 404 Views

THE ROLE OF FISCAL RULES IN OIL REVENUE MANAGEMENT-NIGERIAN EXPERIENCE. Dr. Bright E. Okogu, D. Phil (Oxon.) Senior Special Advisor to the Honorable Minister of Finance, Nigeria Presentation to a Workshop organized by the Angolan Government Luanda, 15-19 May, 2006. Order of Presentation.

E N D

THE ROLE OF FISCAL RULES IN OIL REVENUE MANAGEMENT-NIGERIAN EXPERIENCE Dr. Bright E. Okogu, D. Phil (Oxon.) Senior Special Advisor to the Honorable Minister of Finance, Nigeria Presentation to a Workshop organized by the Angolan Government Luanda, 15-19 May, 2006

Order of Presentation • Introduction • Oil: How a potential blessing can become a curse • Some theory: strategies to ensure effective management of oil revenue • From theory to practice: Nigerian experience of oil revenue management • The Nigerian Fiscal Responsibility Bill/Law • Summary and closing thoughts

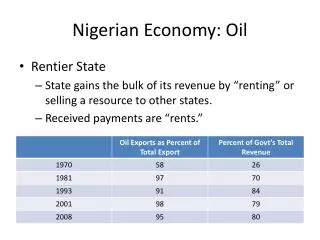

Oil as a potential economic ‘curse’ • Conventional wisdom of resource endowment as source of wealth (Adam Smith & David Ricardo) • Resource ‘curse’ a direct contradiction • Resource rich countries found to grow more slowly (Gelb, 1988); higher corruption, greater income inequality, poverty & conflict (Palley, 2003; Hoeffler, 1998, 2001), etc. • Numerous country examples (Africa & elsewhere) • Transmission channels include: • ‘Dutch Disease’ effects; • macroeconomic volatility (discourages investment & growth); • rent-seeking behavior (Aizenman and Marion, 1993; Fátas and Mihov, 2003 ); poor quality of capital spending; weak public expenditure management, etc.

In the case of Nigeria… • Most of the negative effects were experienced: • Macroeconomic volatility (see charts in next 2 slides) • Corruption • Uncoordinated budget implementation; so aggregate demand unpredictable • Low level conflict, etc.

Nigeria exhibited procyclical expenditure behavior before reforms

OVERVIEW OF OIL PRICE TREND Major Events and World Oil Prices (1970-2004) Refiner Acquisition Cost of Imported Crude Oil (Saudi Light Official Price for 1970-73) Source: EIA Major World Events impact on Oil Prices

Strategies for Managing Oil Revenue • Key issues • Protection of the budget process (stabilize level of expenditure) • Exhaustibility of oil resources (planning for the future; fiscal sustainability) • Intergenerational equity considerations • Suggested approaches • Choice of, & adherence to, a rule fiscal(to de-link expenditure from oil revenue) • Rule must be explicit and publicized to protect implementers • Build consensus around it & must have strong political support • Pay attention to the choice of benchmark oil price: moving average (3, 5, 10-year average?) • Danger is if moving average is used, and actual price deviates significantly from this, the fund could be jeopardized due to large withdrawals • Integrate adaptive expectations into system, e.g., automatic cuts after a certain level of deviation plus some withdrawal • IMF had suggested 3-5 year average for Nigeria (Katz et al, 2005) • Target a level of international financial reserves, but how much?

Types of Funds…I • Stabilization fund(to protect the budgeting process; guarantee minimum expenditure levels) • Build up fund in boom times • draw down in weak market periods • Weakness relates to behavior of the oil price: random walk; weak mean reversion feature • Fund can quickly become exhausted if actual price is below benchmark price for longer than envisaged • Stabilization fund has disadvantage that it looks after the interest of present generation only; no guarantee of savings for future generations • But…if well run, will leave strong economy for future generations (physical & social capital)

Types of Funds…II • Savings fund (mostly to protect future consumption; intergenerational equity) • Require given percentage of revenue or expenditure to be saved in fund (example of Kuwait) • Idea is to build up fund to a comfortable level; convert oil assets into financial assets • Limit consumption to income flows from stock of assets, thus keeping value of wealth constant • More stringent version is keeping per capita wealth constant • An even more stringent version is the so-called “bird-in-hand” approach (obsolescence argument) • For these issues, see, e.g., Davies et al (2001); Barnett and Ossowski (2002); Davies et al (2003). • Problems include • Complexity of operation (capacity issues; political support) • Assets can grow indefinitely; problematic for developing country with huge needs • Always a tempting target for succeeding governments, which may then waste it; this fear could discourage governments building it • Examples of Kuwait, State of Alaska, Venezuela (mixed results)

Types of Funds…III • Financing Fund (Norwegian model) • Fiscal policy operated as though there was no oil revenue • Oil revenue used to finance non-oil deficit; it’s a below-the-line item • Stock of funds used to pay for long-term obligations, e.g. pensions • Problem is that it is not easily adaptable for Developing Countries where non-oil revenue is small (Nigeria non-oil primary balance now about 40% even under the PSI)

Practical steps for improving oil revenue management • Diversify the economy • Broaden the tax base • Discourage ‘white elephant’ projects • Watch quality of capital spending • Reform public procurement procedures. Due Process has saved Nigeria about $3bn in last 4 years • Get into a transparency pact, e.g. the EITI

OIL REVENUE MANAGEMENT IN NIGERIA • Public expenditure management at the core of the reforms for better oil revenue mgt • Price-based fiscal rule introduced since 2004 ($25/b in 2004; $30/b in 2005; $35/b in 2006) • Any revenue above this price is saved in an Excess Crude Oil Account • It is a mixture of stabilization & savings fund • Savings provided resources for clearing Paris Club debt; part of it being used for power projects • Medium-term expenditure framework (to force hard choices & minimize abandoned projects syndrome) • Cash management committee

Some Results of Reforms/Oil Fund • Strong fiscal performance • Surplus of 10% of GDP in 2004; 10.6% in 2005 (consolidated) • $5.9bn in oil fund account in 2004; another $13.4bn in 2005 • Foreign reserves rose from $7bn at end 2003 to $17bn at end 2004; & $28.3bn at end 2005 • No resort to borrowing from CBN/comm. banks • Broad money targets met for first time in decades • Inflation down from 23% in December 2003 to 10% at end 2004, and 11.6% at end 2005 • Strong performance set backdrop for Paris Club debt deal & sovereign ratings (BB-) by Fitch and S & P.

Institutionalizing the Process: The Fiscal Responsibility Bill • Sets of rules to be embodied in legislation committing all tiers of government to: • Fiscal prudence and sound financial management • Withdrawal from the fund only when commodity price falls below predetermined level for 3 consecutive months • Greater transparency and accountability in public finance. • Improve inter-governmental fiscal coordination to secure greater macroeconomic stability

Institutionalizing the Process: EITI • For confidence building among population, Nigeria was first country to sign up for EITI • Sector generally seen by Nigerians as corrupt & non-transparent • Carried out financial, physical & process audit of oil & gas sector, 1999-2004; results shared widely with public • Standard templates now being designed for regular reporting; will help to institutionalize process.

Some Features of the Bill • Section 2.- of the FRB empowers Fiscal Responsibility Council to: • (a) compel any person or government institution to disclose information relating to public revenues and expenditure; • Section 39. sets the basis for the savings fund: (1) Where the Reference Commodity Price rises above the predetermined level, each Government in the Federation shall save its share of the resulting excess proceeds in accordance with subsection (2) of this section. • The savings of each Government in the Federation in pursuance of subsection (1) of this section shall be deposited in a separate account, which shall form part of the respective Governments Consolidated Revenue Fund to be maintained at the Central Bank of Nigeria by each Government. • 5-year moving average; but due to recent high oil price, a 10-year average will be used initially plus spread </= $5/b

Why the Law ? • The Law is a key ingredient of NEEDS. Without it, our economic reforms won’t work. • Need to secure greater macroeconomic stability • Nigeria’s 3 tiers of government have constitutional autonomy. But together they make up ONE NIGERIAN ECONOMY. • FG controls less than 50% of revenue but has responsibility for macroeconomic stability. • Bad fiscal decisions taken by some tiers of government have had drastic effects on inflation, exchange rates, interest rates, etc. • Need to instill and institutionalize transparency and accountability in economic management

The Medium Term Economic Framework • Conceives budgeting as multi year exercise • Efficiently reconciles needs with available resources • Allocates money to strategic priorities among and within sectors • Commences with the preparation of a macroeconomic framework and guidelines • Forms basis for preparing projects and programmes in the annual budgets

More from the FRB • Under Section 2C, the Council shall cause to be prepared: • An Expenditure and Revenue Framework setting out – • (i) estimates of aggregate revenues for the Federation for each financial year in the next three financial years, based on the predetermined Commodity Reference Price adopted; • (ii) aggregate expenditure ceiling for the Federation for each financial year in the next three financial years; • (iii) aggregate tax expenditure for each financial year in the next three financial years; and • (iv) minimum capital expenditure floor for each financial year in the next three financial years;

Expected Impact on Nigeria Fiscal System The Fiscal Responsibility Law will: Commit all tiers of government to a set of efficient rules for economic management • Standardized planning and control of public expenditure • Bring a long-term, as well as annual focus to budgeting • Bring harmony between fiscal and monetary policy

Enforcement mechanisms • The Fiscal Management Council will be responsible for monitoring and enforcement • investigates and forwards violations to the Attorney General for prosecution • One year imprisonment and N500, 000 fine for officers who failure to perform obligation or false statement (Section 56). • 3 years minimum jail sentence for contraventions • Finance Minister/Commissioners held liable and subject to punishment

Lessons Learned • Need strong political support • Ownership of program essential • Build consensus among key arms of government; compromise if necessary (we shared 50% of saved amount in 1st year to encourage buy-in • Some quick wins needed (e.g. publicize balance) • Management of fund must be open & transparent; let public know • Top tier of government must lead by example in prudent fiscal management.

Closing Thoughts • Oil resources can be the blessing it should be; the key is efficient mgt of revenue thru appropriate fiscal rules • There are different approaches to this: each country will have to decide which model is most appropriate to it • Nigerian experience has been relatively successful, but still ad hoc; FRB to underpin & institutionalize it • Essential to have a buy-in of key stakeholders; ownership is critical; political support essential