Download

1 / 29

290 likes | 412 Views

CHAPTER 10 The Cost of Capital. Sources of capital Component costs WACC Adjusting for risk. As a financial manager in a firm. You are often faced with the decision whether to invest in some potential projects. For example, should a firm buy a new production line?.

E N D

CHAPTER 10The Cost of Capital Sources of capital Component costs WACC Adjusting for risk 350 Li

As a financial manager in a firm • You are often faced with the decision whether to invest in some potential projects. • For example, should a firm buy a new production line? 350 Li

Discount rate = required return • From the project, we need to earn at least the required return to compensate our investors for the financing they have provided. • The required return is the same as the appropriate discount rate and is based on the risk of the cash flows from the project. • How to decide the appropriate discount rate (to discount future FCFs from the project)? 350 Li

Estimate discount rate in a project • One simple approach is to ASSUME that the new project has the same risk as the existing business or assets in the firm. • We can estimate what is the required return on the firm’s existing assets. • Then use this required return as the discount rate for the new project. • Of course, if the new project has risk very different from the existing business, one CANNOT do this. 350 Li

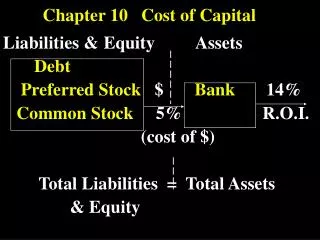

Cost of Capital • Company Cost of Capital (COC) is the required return on the existing firm assets. It is based on the risk of assets. • The risk of firm’s overall assets is equal to the weighted average risks of firm’s debt, preferred stock and common equity. • Thus the cost of capital of a firm equals the weighted average of the cost of debt, the cost of preferred stock, and the cost of common equity. 350 Li

What is the required return on the firm’s existing assets? • A firm’s cost of capital is the required return on the firm’s existing assets; it is also the weighted average required rates of return for all investors of the firm. • Investors may include debt investor, preferred stock investor, and common stock investor. 350 Li

Firm Cost of Capital = WACC • WACC is the weighted average of the after-tax cost of each of the sources capital used by a firm to finance its project, where the weight reflect the proportion of total financing raised from each source. 350 Li

Calculating the weighted average cost of capital WACC = wdrd(1-T) + wprp + wcrs • The w’s refer to the firm’s capital structure weights. wc refers to weight on common stock. • The r’s refer to the cost of each component. 350 Li

rd , rp , rs • rd: cost of debt=required rate of return for debt investors. • rp : cost of preferred stock= required rate of return for preferred stock holders. • rs: cost of equity= required rate of return for common stock holders. 350 Li

How are the weights determined? WACC = wdrd(1-T) + wprp + wcrs • Use market value to determine weights. 350 Li

cost of debt WACC = wdrd(1-T) + wprp + wcrs • rd is the cost of debt capital. • The yield to maturity on outstanding L-T debt is often used as a measure of rd. • Why tax-adjust, i.e. why rd(1-T)? 350 Li

cost of debt • We are concerned with after-tax cash flows, so we need to consider the effect of taxes on the various components of costs of capital. • Interest expense reduces our tax liability • This reduction in taxes reduces our cost of debt • After-tax cost of debt = rd(1-T) 350 Li

A 5-year, 12% annual coupon bond sells for $1,075.81. What is the cost of debt (rd)? 5 -1075.81 120 1000 INPUTS N I/YR PV PMT FV OUTPUT 10 350 Li

cost of debt • Interest is tax deductible, so After-Tax rd = Before Tax rd (1-T) = 10% (1 - 0.40) = 6% 350 Li

cost of preferred stock WACC = wdrd(1-T) + wprp + wcrs • rp is the cost of preferred stock. • The rate of return investors require on the firm’s preferred stock. 350 Li

What is the cost of preferred stock? • The cost of preferred stock can be solved by using this formula: rp = Dp / Pp = $10 / $111.10 = 9% 350 Li

cost of preferred stock • Preferred dividends are not tax-deductible, so no tax adjustments necessary. Just use rp . • rp = Dp / Pp 350 Li

cost of equity WACC = wdrd(1-T) + wprp + wcrs • rs is the cost of equity. • The cost of equity is the return required by equity investors given the risk of the cash flows from the firm 350 Li

Two ways to determine the cost of common equity, rs • CAPM: rs = rRF + (rM – rRF) β • DCF: rs = (D1 / P0) + g • DCF stands for “discounted cash flow model”, also called the dividend growth model. 350 Li

If the rRF = 7%, RPM = 6%, and the firm’s beta is 1.2, what’s the cost of common equity based upon the CAPM? rs = rRF + (rM – rRF) β = 7.0% + (6.0%)1.2 = 14.2% 350 Li

If D0 = $4.19, P0 = $50, and g = 5%, what’s the cost of common equity based upon the DCF approach? D1 = D0 (1 + g) D1 = $4.19 (1 + .05) D1 = $4.3995 rs = (D1 / P0) + g = ($4.3995 / $50) + 0.05 = 13.8% 350 Li

A firm’s capital consists of has 30% in debt, 10% in preferred stock, and 60% in common equity. T=40%, rd=10%,rp=9%, rs=14%. WACC = wdrd(1-T) + wprp + wcrs = 0.3(10%)(0.6) + 0.1(9%) + 0.6(14%) = 1.8% + 0.9% + 8.4% = 11.1% 350 Li

What factors influence a company’s composite WACC? • Interest rates • Tax rates. • The firm’s capital structure and dividend policy. • The firm’s investment policy. Firms with riskier projects generally have a higher WACC. 350 Li

The risk of a project • When calculating the discount rate of a potential investment project, we have often assumed that the project to be taken has the same risk as the existing business or assets of the firm. If this assumption is valid, then we can use WACC as our discount rate to discount future cash flows from a project. • Of course, if the new project has very different risk from existing business, one cannot do so. 350 Li

Should a company use the composite WACC as the hurdle rate for any of its projects? • Ok for a project with average risk. • The composite WACC reflects the risk of an average project undertaken by the firm. Therefore, the WACC only represents the “hurdle rate” for a typical project with average risk in the firm. • Not Ok for a project with very different risk. 350 Li

Using WACC for All Projects - Example • What would happen if we use the WACC for all projects regardless of risk? • Assume the WACC = 15% Project Required Return Expected Return A 20% 17% B 15% 18% C 10% 12% 350 Li

If using one WACC for all projects • You might mistakenly reject project C and take project A. That is, you tend to favor risky projects. • If you keep making such mistakes, the firm may become more and more risky. 350 Li

We should consider the project’s risk • If the project is more risky than the firm, use a discount rate greater than the WACC • If the project is less risky than the firm, use a discount rate less than the WACC 350 Li

Questions • What are the approaches for computing the cost of equity? • How do you compute the cost of debt and the after-tax cost of debt? • How do you compute the capital structure weights required for the WACC? • What is the WACC? • What happens if we use the same WACC as the discount rate for projects with very different risk levels? 350 Li