Download

1 / 5

50 likes | 63 Views

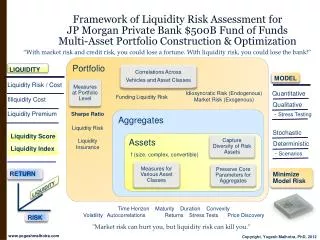

Explore the application of Liquidity Coverage Ratio (LCR) from Basel III framework in a payment system network. Calculate liquidity buffers for large financial institutions using transaction-level data to assess the impact of failing to meet LCR requirements. Investigate the spread of contagion caused by initial liquidity shortfalls and examine the concept of "too big to fail" versus "too connected to fail."

E N D

ArgyrisKahros Market Infrastructure ExpertEuropean Central Bank Discussion on‘Liquidity Coverage Ratio in a payments network’Richard Heuver and Ron Berndsen 15th Payment and Settlement System Simulation Seminar August 31 – September 1, 2017 Helsinki, Finland

Apply the idea of the Liquidity Coverage Ratio (LCR) from the Basel III framework to a payment system network. Calculate liquidity buffers for large financial institutions based on the LCR framework, using LVPS transaction-level data. Investigate the effects on a payment system network of a large financial institution not appropriately meetings its LCR. Monitor the spread of contagion from the imposed initial liquidity shortfall. In addition to being too big to fail can banks also be too connected to fail? What are the authors attempting to do? Discussion on 'Liquidity Coverage Ratio in a payments network'

Calculate liquidity buffers for large banks based on net incoming/outgoing payments over a 30-day period using LCR equals 1 + α. For one bank, induce a liquidity shortfall by decreasing the liquidity buffer, and thus that bank’s LCR. As payments flow, the liquidity shortfall generated by a single bank will reduce its ability to meet outgoing obligations, thereby creating liquidity shortfalls in other banks. The spread is quantified by monitoring the change in LCR for all banks and when LCR<1, this bank is labelled as stressed. How do the authors do it? Discussion on 'Liquidity Coverage Ratio in a payments network'

Magnitude of liquidity shortfall is the most important factor. Liquidity above that associated with LCR=1 (i.e. α) quickly deteriorates. Large banks inflict the most damage. Ability to identify nodes (i.e. banks) that are most efficient at instigating a stress cascade. What do the authors find? Discussion on 'Liquidity Coverage Ratio in a payments network'

Discussion … vs. Discussion on 'Liquidity Coverage Ratio in a payments network'