Download

1 / 9

120 likes | 141 Views

Dive into the world of OLS Regression with Professor Olsson, exploring parameter estimation, error term characteristics, assumption testing, and application in econometric models.

E N D

GRA 6020Multivariate StatisticsThe regression modelOLS Regression Ulf H. Olsson Professor of Statistics

Regression Analysis Ulf H. Olsson

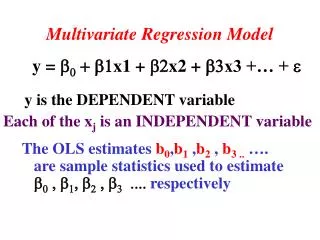

OLS Regression parameter St.error T-value P-value Confidence interval R-sq R-sq.adj F-value The error term Regression analysis Ulf H. Olsson

The error term has constant variance The error term follows a normal distribution with expectation equal to zero The x-variables are independent of the error term The x-variables are linearly independent The dependent variable is normally distributed Regression Analysis Ulf H. Olsson

Y is stochastic, x1, x2,….,xk are not Linearity in the parameters The error term has const.variance The error term is norm. Distributed with expectation equal to zero The error terms are independent The x-variables are linearly independent Classical Assumptions Ulf H. Olsson

GAUSS-MARKOV • OLS is BLUE given the Classical Assumptions • B = Best • L=Linear • U=Unbiased • E=Estimator Ulf H. Olsson

Econometric Model • Klein’s Model (1950) Ulf H. Olsson

Making Numbers (OLS and TSLS) • CT = 16.237+0.193*PT+0.0899*PT_1+0.796*WT, R² = 0.981 • (1.303) (0.0912) (0.0906) (0.0399) • 12.464 2.115 0.992 19.933 • CT = 15.324+0.0763*PT+0.186*PT_1+0.828*WT, R² = 0.979 • (1.453) (0.138) (0.146) (0.0439) • 10.546 0.553 1.275 18.844 Ulf H. Olsson

Estimate Klein’s equations by OLS Regression Ulf H. Olsson