Download

1 / 23

230 likes | 244 Views

This study delves into why capital is crucial in insurance, exploring frictional insolvency costs and double taxation. It examines the base cost of capital, frictional capital costs, and financial pricing models. Learn how to allocate capital costs effectively and the Myers-Read method for determining solvency measures. Practical applications, including layer beta properties and numerical examples, are discussed.

E N D

Allocating the Cost of Capital CAS Spring Meeting May 19-22, 2002 Robert P. Butsic Fireman’s Fund Insurance

Why is Capital Necessary? • The answer is not obvious: • We can’t have enough capital to eliminate insurance insolvency • So why not have minimal capital and let guaranty funds protect policyholders? • Answer is: frictional insolvency costs • Additional system costs due to insolvency: • Legal fees, market disruption, extra claims handling costs

Optimal Capital Level Frictional Insolvency Costs Frictional Capital Costs Capital Amount

What is the Cost of Capital? • Investor supplies capital and expects return commensurate with risk to which the capital is exposed • This return is the cost of capital • Traditional view of insurance management • But, look from the modern finance perspective

Base Cost of Capital • A: Investor invests capital in a levered fund • borrow cash and invest all assets • identical to the insurer’s assets • Investor’s expected return in A is called Base Cost of Capital • B: Insurer has same balance sheet • But insurer has higher COC

Frictional Costs of Capital • The insurance mechanism will introduce extra costs • Government, regulation and organization • Illiquid nature of insurance liability • Information asymmetry (opaqueness) • These are frictional costs of capital • key one is double taxation • Most easily quantified

Double Taxation Example • Investor can directly invest in security with 10% return, but invests in ABC Insurance, who puts money in same security • ABC gets 10% return, pays 35% tax and gives 6.5% net back to investor • A losing deal unless PH can make up the difference

Other Frictional Costs • Regulatory costs • Capital can’t be easily moved, so investment is illiquid • Agency costs • Misalignment of owners’ and managers’ interests (Enron a classic example) • Financial distress costs • Legal fees • Distressed sale of assets

Financial Pricing Model • Fair premium = total present value of • loss & LAE (including risk margin) • UW expenses • Frictional capital costs • Note that traditional (base) cost of capital is embedded in risk margin

Risk Margin and COC Example • Assumptions • Fair premium is $1000, paid up front, $1040 loss paid in one year • Risk-free rate of 6%, $500 of capital required • No frictional COC, taxes or expenses • Calculation • Initial assets of $1500 grow to $1590, leaving $550 for a 10% return (COC) • Risk margin is $18.87 = 1000 - 1040/1.06

RM and COC Example, Cont. • Which comes first, the RM or the COC? • Each implies the other • In determining a fair premium, it must be the risk margin: • Products have different levels of risk • What COC should a riskless coverage have? • Thus, the COC is not fixed for an insurer -- it varies by product

Allocating Capital Costs • For pricing or performance measurement, must allocate capital costs to product • If we know the RM, then we need to allocate the frictional COC • If we don’t know the RM, and use a COC pricing model, then we allocate both frictional and base COC

Capital Allocation • In order to assess capital costs by product, we first need to allocate capital to product • There are many methods • Lots of ad hoc models • Very few economically sound models • One of them is the general Myers-Read method

Myers-Read Method • Uses the expected default (PH deficit) as a solvency measure • Others, such as default (ruin) probability will also work (and may be better) • Major assumptions • predetermined capital ratios exist: • A marginal change in the line mix keeps the default measure at a constant rate:

More on M-R Model • Other inputs • Probability distribution of loss and asset values • Means, correlations and volatilities • We solve for capital ratio • Result: • Beta is covariance/variance • Z is distribution-dependent

Loss Beta • Relevant risk measure for capital allocation is loss beta • Volatility, correlation with portfolio and weight determine loss beta • Strong parallel with asset pricing, CAPM, portfolio optimization • Capital allocation is exact; no overlap • No order dependency

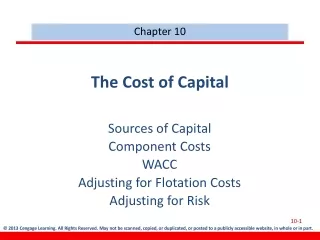

Application to Coverage Layers • For policy/treaty, capital allocation to layer depends on covariance of layer with that of unlimited loss • Layer covariance depends only on loss size distribution • Layer beta and capital/loss increase with limits

25.00 20.00 15.00 10.00 5.00 0.00 0 50 100 150 200 250 300 350 400 x General Layer Beta Properties • Monotonic increasing with layer, with zero layer beta at lowest point layer • Generally unbounded Legend: RHS top to bottom Pareto Lognormal Exponential Gamma Normal

Practical Applications • Best measure of capital is economic (fair) value • As an approximation, capital is proportional to the loss/layer beta • For allocating a company’s capital, the relevant time horizon is one year • Allocation base is reserves plus next year’s AY incurred losses

Summary • Importance of frictional costs in theory of solvency and capital allocation • Myers-Read method is economically sound, with friendly (to user) results • We’ve still got a long road ahead before common agreement on capital allocation methodology

Further Reading • John Hancock, Paul Huber, Pablo Koch, 2001The economics of insurance: How insurers create value for shareholders, Swiss Re Publishinghttp://www.swissre.com/ • Myers, Read, 2001, Capital Allocation for Insurance Companies, Journal of Risk and Insurance, 68:4, 545-580 • Butsic, 1999, Capital Allocation for Property Liability Insurers: A Catastrophe Reinsurance Application. Casualty Actuarial Society Forum, Fall 1999http://www.casact.org/pubs/forum/99spforum/99spftoc.htm

Further Reading II • Butsic, Cummins, Derrig, Phillips, 2000, The Risk Premium Project, Phase I and II Report, CAS Website, http://casact.org/cotor/rppreport.pdf