Download

1 / 20

200 likes | 212 Views

Explore the impacts of liberalized financial flows, from money laundering to tax evasion, and the potential solutions like international conventions or stronger national controls. Dive into the dynamics of illegal money flows, AML regime, and the challenges faced in combating economic crimes through deterrence and forfeiture. Understand the interplay between AML efforts and tax enforcement, dissecting the nuances of black money and its economic ramifications.

E N D

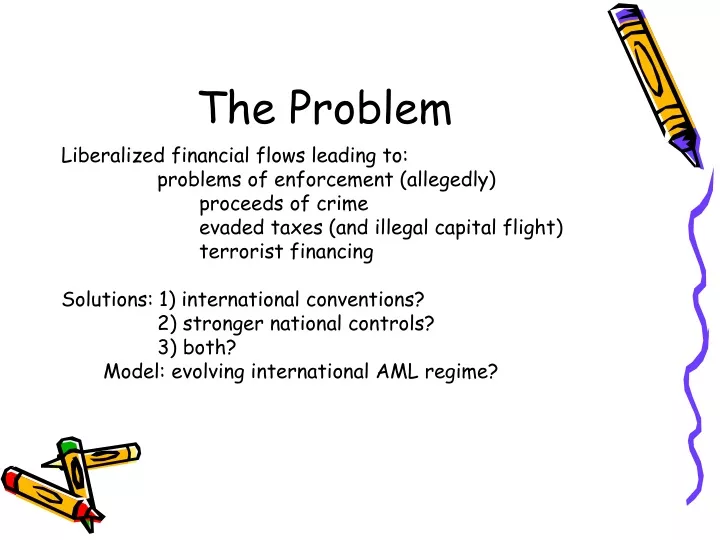

The Problem Liberalized financial flows leading to: problems of enforcement (allegedly) proceeds of crime evaded taxes (and illegal capital flight) terrorist financing Solutions: 1) international conventions? 2) stronger national controls? 3) both? Model: evolving international AML regime?

Illegal Money Flows: • Legal Origin Rendered Illegal by Tax Evasion and/or by (Illegal) Capital Flight 2) Illegal Origin Rendered Apparently Legal by Money Laundering Which is the bigger threat? Which attracts the most attention?

The Five Issues • Logic and efficacy of AML regime • Amenability of five target forms of illegal finance • Particular problems of AML for tax evasion • Alternative techniques previous used against “black money.” • Broader trends in evolving fiscal environment

AML Regime – Main Elements • New crime “money laundering” • Extraordinary reporting requirements target “proceeds of crime” • Loosening legal criteria to facilitate confiscation • Extending regime to entire domestic financial apparatus • Internationalizing scope

AML Theory of Deterrence Forfeiture (aka confiscation) removes: • Motive for more crimes • Means to commit more crimes • Capacity to infiltrate and corrupt legal economy

The Reasons Why? • Vast hordes of criminal capital • Special danger from “cartels” • Threat to legal economy • Simplistic view of criminal motivation • Unflattering police opinion of bankers • Fear US banks lose competitive edge

Illicit FundsCategories and Characteristics ProceedsFlight KEvaded TaxesTerror $ always illegal mainly legal almost all legal mainly legal exit IC exit DC exit IC exit DC covert covert overt (?) usually overt (?) ID change ID change ID change ID change (?) returns takes refuge returns to IC enters IC IC covert in IC covert covert or overt legal C or I legal I legal C or I illegal use

Fifth Column?Preceeds (Pre-Seeds?) of Crime always legal origin leaves IC overtly (if taxed) or covertly changes ID abroad returns to IC covertly spent (I) illegally ---morphs to criminal proceeds cycle

Predatory – redistribution of existing wealth Commercial – redistribution of existing income Market-based – generation of new income flow Restitution No fiscal effects 2) Restitution and Fines Unlikely fiscal effects 3) Forfeiture Fiscal effects Three Forms of Economic Crime

Five Categories Differ in: • Motives for initial acquisition • Point of illegality • Relative amounts • Amenability to control via AML

Gross income – costs = net income (profit) Costs paid to legal suppliers illegal suppliers investors – aware - unaware Net income can be: consumed saved underground (reinvested in crime?) saved overground (via laundering) Overground savings for: – passive investments - active investments businesses operated legally businesses operated illegally The Path of the Proceeds

Targets of AML Block Facilitate infiltrationexfiltrationforfeiture Proceeds maybe no maybe Terror $ rare rare rare Evaded taxes no no maybe Flight capital no rare no Preceeds no no no

Objective: Deterrence At Three Levels motivemeanscapacity Proceeds maybe maybe delirium Evaded taxes redundant irrelevant reverse flow Flight K redundant irrelevant reverse flow Terror $ no no irrelevant Preceeds minor no reverse flow (risk seeking behavior)

Conflicts: AML and Tax Enforcement • Criminals few, tax evaders many • Trivializes offense • Division of spoils or prohibition? • Criminal procedures only last resort • Only works against market-based • Theory of deterrence inappropriate • Destruction of trust from end of privacy

Tax Enforcement as Alternative to AML • Starts by targeting gross proceeds • Requires proof of “costs” • Add interest and penalties • No need for “money laundering” • Civil procedures no loss due process • Fits deterrence theory

Features of “Black Money”Higher Propensity to… • consume (ie lower propensity to save) • consume untraceable services or luxuries • Import (smuggle) luxuries • evade taxes • invest in luxury real estate, services, etc. • internal capital flight (gold, US $ etc.) • external capital flight

Impact of “Black Money” Economic Plane/Policy Objective Monetary Increase deposits in banks Fiscal Increase public fiscal resources B of P Increase access to forex

The Forgotten Options AccommodationLegitimationNeutralization Monetary bank-secrecy cash amnesties demonetization Fiscal state whitener bonds “illegal bearer-bonds & tax amnestiesenrichment” Payments forex capital flight stronger forex bearer bonds amnesties controls

Liberalized financial flows leading to: -homogenized world financial system! -loss of national economic control! -regressive redistribution of income and wealth! -accelerated environmental destruction! -(allegedly) problems of criminal or anti-terror enforcement? National versus international approaches? Special positions of tax havens: co-conspirators or file clerks? Shift in the fiscal environment The Broader Context

Current: Micro Excise (sins ag. society) Retail Sales Value Added Macro Personal Income Capital Gains Corporate Net Income Future: Micro Excise (sins ag. nature) “Green” – virgin resources etc Macro Personal Expenditure Physical Wealth Business Costs Fiscal Systems: Reform or Transform?