Download

1 / 5

50 likes | 133 Views

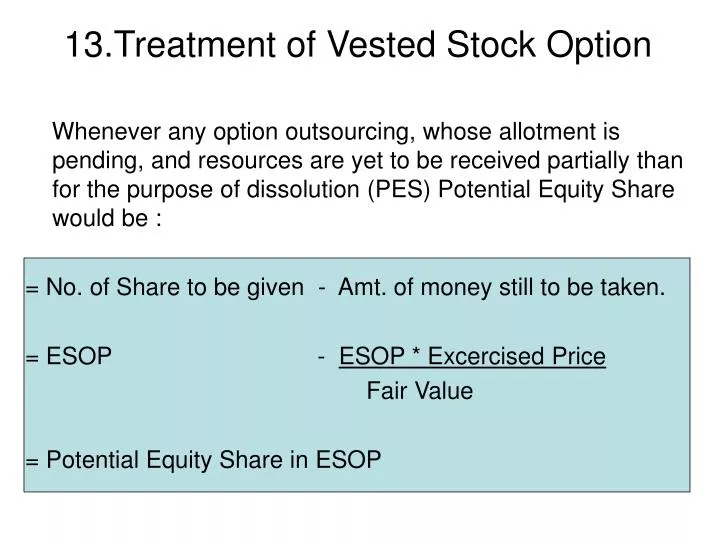

13.Treatment of Vested Stock Option. Whenever any option outsourcing, whose allotment is pending, and resources are yet to be received partially than for the purpose of dissolution (PES) Potential Equity Share would be : = No. of Share to be given - Amt. of money still to be taken.

E N D

13.Treatment of Vested Stock Option Whenever any option outsourcing, whose allotment is pending, and resources are yet to be received partially than for the purpose of dissolution (PES) Potential Equity Share would be : = No. of Share to be given - Amt. of money still to be taken. = ESOP - ESOP * Excercised Price Fair Value = Potential Equity Share in ESOP

15. Disclosure Requirement • Basic @ Diluted EPS will be disclosed on Face of P&L A/c. • Even if Basic @ Diluted EPS is Negative than also disclosed on the face of P&L A/c. • EPS will be disclosed for Stand Alone ( Single Co.) and Consolidated Statement (Statement of Subsidiaary Co.). • EPS will be calculated for share holders based on : * Earning after Extraordinary Item and * Earning before Extraordinary Item.

Specimen Disclosure as per Para 48 Profit and Loss Account Net Profit Ratio in Bracket are restated

v) A Reconciliation will be given for • Earnings (BEPS, DEPS) with Net Profit. AND • Wt Avg of Share in BEPS with wt Avg of Share in DEPS. ( Only Current Year ) Note: • In case of small and medium companies DEPS need not be disclosed. 2. In case of small and medium companies reconciliation are not required.