Download

1 / 9

120 likes | 276 Views

Using Historic Tax Credits in New York. Joel Cohn, CPA Reznick Group www.reznickgroup.com 410-783-4900 joel.cohn@reznickgroup.com. Keeping the Credits or Selling Them?. If the Developer Can Use Them, The Credits Are Most Valuable When Kept

E N D

Using Historic Tax Credits in New York Joel Cohn, CPA Reznick Group www.reznickgroup.com 410-783-4900 joel.cohn@reznickgroup.com

Keeping the Credits or Selling Them? • If the Developer Can Use Them, The Credits Are Most Valuable When Kept • If They Are to be Sold, Remember That ‘Selling Credits’ is a Misnomer • The Drop Dead Date to Close on The Sale of the Credits is The Date of Completion of All or a Portion of the Building Reznick Group Building Business Value

Pricing Metrics for Credits • Credits Are Priced Based on Each $1.00 of Credit • e.g. Buyer Pays $0.95 for Each $1.00 of Credit Generated • The Pricing Depends on The Magnitude of Credits • Big Deals vs. Small Deals • Big Deals Can Be Priced Over $1.00/$1.00 of Credit • Small Deals Usually Less Than $1.00/$1.00 of Credit • Pricing Also Depends on How Quickly Developer Needs/Wants Money from Credit Buyer • Pricing Also Depends on Typical Underwriting Criteria: of the project, developer, etc. Reznick Group Building Business Value

Where Credits Fit in The Capital Stack • It’s Not Just a Question of How They Fit But Also When • Need to Consider the Bridge Financing Need and the Cost to Bridge • In the Final Capital Stack, the Tax Credit Equity Is No More Than +/- 20% of Total Development Costs, and Probably Less • The Gross Price is The Proceeds Available to Get the Building Built Reznick Group Building Business Value

It’s The Net Price That Matters in the End • Economic Returns Are Required by Credit Buyers • Cash on Cash Return – Typically 2-3%/year for 5 years, based on Contributed Capital • Exit Fee – 10-15% of Contributed Capital • Plus a Portion of Depreciation – At Least 10% • Potential Tax Liability Payments • Transaction/Closing Costs • Ongoing Administrative Costs • Loss of Any Building Efficiencies to Meet Standards Reznick Group Building Business Value

Who Are The Buyers of the Credit? • Public Companies • Not Subject to Some of the Same Limitations in Using This Credit As Are Individuals and Closely-Held Companies • Small Universe of Buyers– Today There Are Less Than 10 Active Buyers • Choosing a Buyer: Consider All Deal Terms, Not Just Gross Credit Price Reznick Group Building Business Value

Plain Vanilla Reznick Group Building Business Value

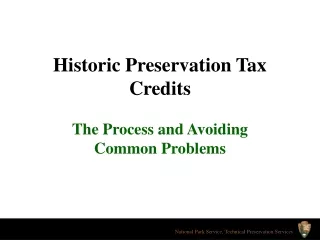

Not So Plain Vanilla Historic Deal Structure Tax Credit Investor 99% LP Project Sponsor 90% Credits, Profits, Losses Equity Investment 99% Credits, Profits, Losses Equity $$ 10% Losses, Profit, 10% Residual, Tax Credit Pass Through Real Estate Partnership/ Property Owner/ Master Lessor Operating Partnership/ Master Lessee Entity Master Lease Rent Equity $$ Rent Mortgage Tenant Group Reznick Group Building Business Value