Download

1 / 30

370 likes | 574 Views

Lecture 5 - Financial Planning and Forecasting. Strategy. A company’s strategy consists of the competitive moves, internal operating approaches, and action plans devised by management to produce successful performance. Strategy is management’s “game plan” for running the business.

E N D

Strategy • A company’s strategy consists of the competitive moves, internal operating approaches, and action plans devised by management to produce successful performance. • Strategy is management’s “game plan” for running the business. • Managers need strategies to guide HOW the organization’s business will be conducted and HOW performance targets will be achieved. 2

Strategic Planning • Strategic planning is a systematic process through which an organization agrees on and builds commitment among key stakeholders to priorities that are essential to its mission and are responsive to the environment. • Strategic Planning guides the acquisition and allocation of resources to achieve these priorities. 3

Strategic Planning versus Operational Planning • Operational Planning • implementation • how • means • plans • efficiency • control • Strategic Planning • formulation • What, where • ends • vision • effectiveness • risk 4

Financial Planning and Pro Forma Statements • Financial plans evaluate the economics behind the strategy and operations. They consist of six steps: • Project financial statements to analyze the effects of the operating plan on projected profits and financial ratios. • Determine the funds needed to support the plan. • Forecast funds availability. • Establish and maintain a system of controls to govern the allocation and use of funds within the firm. • Develop procedures for adjusting the basic plan if the economic forecasts upon which the plan was based do not materialize • Establish a performance-based management compensation system. 5

Steps in Financial Forecasting • Forecast sales • Project the assets needed to support sales • Project internally generated funds • Project outside funds needed • Decide how to raise funds • See effects of plan on ratios and stock price 6

Sales Forecast • Sales forecasts are usually based on the analysis of historic data. • An accurate sale forecast is critical to the firm’s profitability: Sales Forecast Under-optimistic • Company will fail to meet demand • Market share will be lost Over-optimistic Too much inventory and/or fixed assets • Low turnover ratio • High cost of depreciation and storage • Write-offs of obsolete inventory • Low profit • Low rate of return on equity • Low free cash flow • Depressed stock price 7

The Percent of Sales Method • This is the most common method, which begins with the sales forecast expressed as an annual growth rate in dollar sale revenue. • Many items on the balance sheet and income statement are assumed to change proportionally with sales. 9

Step 1 - Analyze the Historical Ratios * * *Spontaneous generated funds - increase spontaneously with sales 10

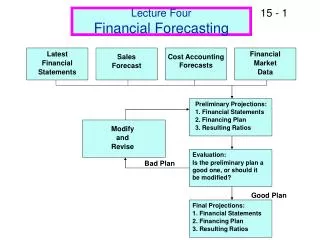

How to Forecast Interest Expense • Interest expense is actually based on the daily balance of debt during the year. • There are three ways to approximate interest expense. Base it on: • Debt at end of year • Debt at beginning of year • Average of beginning and ending debt More… 12

Basing Interest Expense on Debt at End of Year • Will over-estimate interest expense if debt is added throughout the year instead of all on January 1. • Causes circularity called financial feedback: more debt causes more interest, which reduces net income, which reduces retained earnings, which causes more debt, etc. Basing Interest Expense on Debt at Beginning of Year • Will under-estimate interest expense if debt is added throughout the year instead of all on December 31. • But doesn’t cause problem of circularity. 13

Basing Interest Expense on Average of Beginning and Ending Debt A Solution that Balances Accuracy and Complexity • Will accurately estimate the interest payments if debt is added smoothly throughout the year. • But has problem of circularity. • Base interest expense on beginning debt, but use a slightly higher interest rate. • Easy to implement • Reasonably accurate 14

2009 Balance Sheet(Millions of $) Cash & sec. $ 10 Accts. pay. & accruals $ 200 Accounts rec. 375 Notes payable 110 Inventories 615 Total CL $ 310 Total CA $ 1000 L-T debt 754 Common +pr stk 170 Net fixed Retained 1000 assets earnings 766 Total assets $2,000 Total Liabilities $2,000

2009 Income Statement (Millions of $) $3,000.00 Sales 2616.00 Less: COGS (87.2%) 100.00 Dep costs EBIT $ 283.80 88.00 Interest EBT $ 195.80 Taxes (40%) +pr.div 82.30 Net income $ 113.50 $57.50 Dividends (Com+Pr Add’n to RE $56.00

AFN (Additional Funds Needed):Key Assumptions • Operating at full capacity in 2009. • Each type of asset grows proportionally with sales. • Payables and accruals grow proportionally with sales. • 2009 profit margin ($113.5/$3,000 = 3.80%) and retention ratio (56/114) = .49 will be maintained. • Sales are expected to increase by $300 million. 19

Assets Assets = 0..667sales 2,200 Assets = (A*/S0)Sales = 0..667($300) = $200. 2,000 Sales 0 3,000 3,300 A*/S0 = $2,000/$3,000 = 0.667 = $2200/$3,300. Assets vs. Sales

Definitions of Variables in AFN • A*/S0: assets required to support sales; called capital intensity ratio. • ∆S: increase in sales. • L*/S0: spontaneous liabilities ratio • M: profit margin (Net income/sales) • RR: retention ratio; percent of net income not paid as dividend. 21

If assets increase by $200 million, what is the AFN? AFN = (A*/S0)∆S - (L*/S0)∆S - M(S1)(RR) AFN = ($2,000/$3,000)($300) (0.667) x $300 - ($200/$3,000)($300) (0.067) x ($300) - 0.0380($3,300)(0.49) = $118 million AFN = $118 million. 22

How Would Increases in Various Items Affect the AFN? • Higher sales: • Increases asset requirements, increases AFN. • Higher dividend payout ratio: • Reduces funds available internally, increases AFN. • Higher profit margin: • Increases funds available internally, decreases AFN. • Higher capital intensity ratio, A*/S0: • Increases asset requirements, increases AFN. • Pay suppliers sooner: • Decreases spontaneous liabilities, increases AFN. 23

Implications of AFN • If AFN is positive, then you must secure additional financing. • If AFN is negative, then you have more financing than is needed. • Pay off debt. • Buy back stock. • Buy short-term investments. 24

What if Balance Sheet Ratios are Subject to Change • We have so far assumed that ratios of both assets and liabilities to sales are constant over time • Sometimes this assumption is incorrect. 25

1,100 1,000 Declining A/S Ratio Assets Base Stock Sales 0 2,000 2,500 $1,000/$2,000 = 0.5; $1,100/$2,500 = 0.44. Declining ratio shows economies of scale. Going from S = $0 to S = $2,000 requires $1,000 of assets. Next $500 of sales requires only $100 of assets. Economies of Scale

1,500 1,000 Assets 500 Sales 500 1,000 2,000 A/S changes if assets are lumpy. Generally will have excess capacity, but eventually a small S leads to a large A. Lumpy Assets – Buying Discrete Units

Capacity sales = Actual sales % of capacity $3,000 0.96 = = $3,125. Thus, if sales increase to $3,300 fixed assets would only have to increase to 3,300 x .32 = $1,056 What if 2009 fixed assets had been operated at 96% of capacity: Target Fixed Assets/Sales = = = 32% Actual Fixed Asset $1,000 Full Capacity Sales $3,125

Summary: How different factors affect the AFN forecast. • Excess capacity: lowers AFN. • Economies of scale: leads to less-than-proportional asset increases. • Lumpy assets: leads to large periodic AFN requirements, recurring excess capacity. 29