Download

1 / 50

500 likes | 513 Views

The Effects of Vertical Integration on the Medicare Trust Fund. Gerald N. Rogan, MD, FACEP National Heritage Insurance Company Carrier Medical Director. Graphics by Rachael Brown Medicare Payment Safeguard Unit. The Story You Are About To See Is True. The names have been

E N D

The Effects of VerticalIntegration on the Medicare Trust Fund Gerald N. Rogan, MD, FACEP National Heritage Insurance Company Carrier Medical Director Graphics by Rachael Brown Medicare Payment Safeguard Unit

The Story You Are About To See Is True. The names have been changed to protect the innocent! VERTICAL INTEGRATION

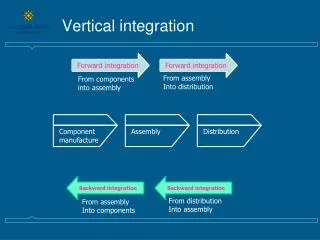

Definition of Vertical Integration • Vertical Integration is the linkage of independent businesses serving different stages of the health care service process into one ownership entity. • Linkages may be among hospitals, primary care physicians, primary-specialty IPAs, specialty groups, clinical laboratories, special disease clinics, health care equipment manufacturers, pharmaceutical companies, home health agencies, and insurance company functions. • This becomes a creative challenge for enforcement of the Stark laws because the physicians are no longer in charge.

What is Driving Vertical(and horozontal)Integration ? • The traditional health care business is just breaking even today: * Includes income from investments, contributions & diversified businesses ** Based on results for the first three quarters PROFIT PERCENT YEAR Source: Economic Trend/AHA Panel Survey

How Physician Acquisitions by Hospitals Have Grown • Market forces and the ascendance of managed care have fostered a medical-practice buying frenzy by management companies: • Caremark • PhyCor • MedPartners/ Mulliken • Hospital acquisitions * Number of full-time-equivalent physicians in acquired practices Source : The 1995 Physician Practice Acquisition Resource Book

Percent of Practice Acquisitions by Region (through 1995) • There is a boom in hospital practice purchases East North Central Region Northeast Far West 20% 7% Near West 20% 36% South 17% Source: The 1995 Physician Practice Acquisition Resource Book

Types of Practices Hospitals Have Purchased • Three-fourths of hospital acquisitions involved family and internal medicine practices. 7 % 5 7 % 7 % 9 % 2 0 % Source: The 1995 Physician Practice Acquisition Resource Book

Percent of Medicare Beneficiaries Enrolled in Risk Plans, by State, December 1996 Acquisition and risk plan areas are not correlated East North Central Region Northeast 10% + 10% Far West Near West 2 - 10% 2 - 10% 10 % + South 2% 10% + Source: PPRC report to congress 2/27/97 (approximated)

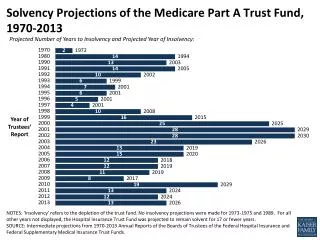

Medicare Payments B of B B of A 9 % 1 5 % Source: Congressional Budget Office, Medicare Baseline, January 1997.

Average Rate of Annual Growth in Medicare Payments per Enrollee 10.6 % 10 % Source: Based on projections from Congressional Budget Office, Medicare Baseline, January 1997. H O H O 5% 3.9 % P P * Includes hospital outpatient, clinical laboratory, and other non-physician Part B services.

Strategic Rationale for Hospital Integration • Hospital needs Managed Care business to survive. • Hospital Health Network will capture market share for the hospital and aligned specialists. • Hospital capture of HMO & some PPO Contracts • Legal opportunities to contribute hospital funds to aligned physicians • Consolidation with “our” doctors • Bring independent primary care physicians into the hospital camp • Control local market • Leverage for regional alliances • Increase market strength and recognition • Expand primary care capacity for hospital referrals Hospital Strategy

Hospital-Physician Integration DIRECT PHYSICIAN EMPLOYMENT HEALTH CARE NETWORK FOUNDATION MSO MSO CLOSED PHO DEGREE OF VERTICAL INTEGRATION OPEN PHO CLOSED PHO OPEN PHO HOSPITAL SPONSORED IPA SOLO & SMALL GROUP PRACTICES SOLO MD's DOLLARS INVESTED

Provide physician recruitment for established practices Provide MSO services for practice management Provide MSO services for physician staff and billing services Provide MSO services for facility purchase and lease-back Organize hospital aligned, physician “owned” IPA Charge high per diem rates to all local IPAs Cause all local IPAs to fail, but Hide the hospital organized IPA losses through “controlled” accounting “Discover” the hospital controlled physician “owned”IPA is bankrupt Help its doctors by purchasing the IPA HMO contracts for the hospital health network Build a hospital health network primary care group founded on the MSO doctors already under control Obtain a 501c3 entity license (CA) Compete with independent renegade physicians and IPAs for market share and referrals Stages of Integration:

Convincing a few of the remaining independent primary doctors to sell

Visibility / Reputation of Organization (brand name product) Growth potential Access to Hospital Funds More patients via hospital advertising Access to Tax-Exempt Bond Market No Company Property or Income Taxes Revenues from donations Easier Recruitment of new physicians Physician buy-in or buy-out, not required Practice stability Effective Managed Care Strategy Convert goodwill to cash for current use Anticipate the coming doctor consolidation Loss of practice control (20% rule) No Equity in the practice “Defacto” Hospital Employee Status “At will” physician employment contract Referral patterns might be changed Competitive disadvantage for those not joining Hospital Physician Health Network Pro and Con For Physicians PRO CON

“Consolidation” of MD’s means that some MD’s may be Eliminated. WILL WORK FOR FOOD John Doe, MD Jane Smith, MD DOCTOR’S CAB CO.

Therefore, please join Our Good Ship “Hospital” and sail across the seas of managed care to the safety of the land of tax free dollars.

My Doctors Primary Care FORMERLY INDEPENDENT PRIMARY CARE MEDICAL GROUP BALANCE SHEET - AUGUST 31, 1995 ASSETS LIABILITIES PARTNERS CAPITAL

My Doctors Primary CareHealth System Purchase OfferAllocation of Purchase Price For6 FTE Group Family Practice CATEGORY ALLOCATION Accounts Receivable $ 360,000 Fixed Assets 142,600 Intangible Assets Noncompete Agreement 851,400 Total 1,354,000

My Doctors Primary CarePer Partner Net Value • INDEPENDENT APPRAISAL $98,000 • NET PURCHASE PRICE $315,000 • GAIN PER PARTNER $217,000 ( 3 Partners)

Medical Society Foundation Admar Aetna Open Choice PPO American Health Network Beech Street PPO Benefit Panel Services Blue Cross Prudent Buyer Blue Shield Preferred Cigna/Equicor/Intracorp John Hancock Preferred Lifeguard MetLife PPO Pacificare Preferred Health Network Private Healthcare Systems PruNet PPO PruNetwork PPO Takecare Preferred Network Travelers Managed Care Travelers Preferred What Patients Come Over ? Formerly Independent Primary Care Medical Group Contracts

Daley Hope Medical Group Purchase Price, Net $600,000 $1,200,000 per physician • all but $300,000 down • balance over 5 years • plus interest

Physician Practice SalePrice is Inflated • Inflated goodwill value paid to doctor - (inurement) • No doctor would pay this much. - (contrived market) • Managed care patients carry less goodwill since patients often switch plans and doctors. • Managed care patient fees are discounted, reducing non-network doctor income and practice “profit” potential.

Understanding Vertical Integration “Follow the Money” Hospital and Network Negotiate Full-Risk contracts as a Joint Entity HEALTH MAINTENANCE ORGANIZATION Full risk capitation contract Joint Hospital-Physician Contracting Organization lower per diem rate capitation amount Health Network Physicians Hospital “hidden extras” $ $ Surplus

Example of Hospital Health Network Everyone’s Community Health System Everyone’s Community Medical Center Everyone’s Community Health Network Mount Everyone’s District Hospital My Medical Staff IPA My Doctors Primary Care Renegade Doctors IPA AFTER TAX IPA Ahwahnee Physician Management Services = owned or controlled = contractual or independent MD MD MD MD MD MD

Ahwahnee Primary Care Management Services • PRACTICE GROWTH SERVICES • Physician recruiting services (referrals) • Net revenue guarantee through Everyone’s Community hospital (referrals) • Practice consolidation/mergers into My Doctors Primary Care (referrals) • PRACTICE MANAGEMENT AGREEMENTS • Manage operations of medical practice (control) • Provide billing and collection services • Practice employees become Ahwahnee Management Employees (control) • Provide Physician income guarantees (referrals) • Provide hospital leased space (control) • Provide tenant improvements (control)

Ahwahnee Primary Care Management Services Con’t. • MARKETING SERVICES • Health fair promotion • Marketing services for managed physicians • Hospital referral service

My Medical Staff IPA Support From: Everyone’s Community Health Network Increase My Medical Staff IPA Capitation by $4.00 pmpm MD Hospital Tax Free $$

Development CostsEveryone’s Community Health NetworkCapitalization Requirements

Independent IPAs Get Less $ Hospital Controls Income of Independent IPA’s HMO Capitation Payment Renegade IPA Hospital-My Doctors Contracts Committee Higher Perdiem Rate Hospital SURPLUS

Everyone’s Community Hospital • Non profit hospital • Maximizes cost reports (?) • Pays for referrals from profits via inflated purchase price, generous doctor salaries, and special hospital management jobs • Converts services from “B of B” to “B of A” for higher reimbursement • Amortizes Vertical Integration costs into cost report

Hospital Next Step How To Recover The Money ? • Improve clinical decision making. • Improve care quality for competitive edge • Get more $ from HMOs by controlling the local market • Streamline information transfer • Refer non-managed care patients to hospital out patient services. • Refer non-managed care patients to hospital based specialists • Arrange global capitation contracts and reduce expensive patient services. • Employ lower cost physician extenders for managed care patients

Next Step How To Recover The Money ? (Con’t) • Replace non compliant physicians with team players. • Reduce resource utilization for capitated patients. • Gain tertiary referral from distant network physicians • Reduce salaries of controlled physicians • Reduce capitation amounts paid to captured specialists • Out reach for “well” Patients • Encourage sicker patients to dis-enroll from managed care

Costs of Medical Managed Care Patients as Percentage of Average FFS Medicare Spending per Beneficiary 1 6 0 % six months following HMO Dis-enrollment 6 3 % Six months before HMO Enrolment Source: PPRC analysis of 1989-1994 Medicare claims and denominator files

Part B of B vs Part B of Atypes of services INDEPENDENT PROVIDER HOSPITAL OUT-PATIENT OUT-PATIENT Outpatient Physical Therapy00/pt 00/pt Radiation Oncology T C 00/pt 00/pt Diagnostic Radiology T C 00/pt 00/pt Diagnostic Card iology T C 00/pt 00/pt Clinical Laboratory 00/pt 00/pt Ambulatory Surgery Center 00/pt 00/pt

Part B of B vs Part B of A Beneficiary Costs INDEPENDENT PROVIDER HOSPITAL OUT-PATIENT OUT-PATIENT Physical Therapy (7 codes) : 20% of limiting charge 20% of retail Physical Therapy (7 codes) : maximum $900/yr no maximum Occupational Therapy (1 code) 20% of limiting charge 20% of retail Rad. Onc. Technical Component ?? Diagnostic Rad. Technical Component ?? Diagnostic Card Technical Component ?? Clinical Laboratory ?? Ambulatory Surgery Center ??

Other Examples of Vertical Integration • Slick Comprehensive Cancer Centers • Wunderkind Dialysis • Columbine Hospital Network • Tax Free Hospital Foundation

Columbine Hospital Network • For profit hospitals • Maximizes cost reports • pays for referrals from profits via stock and dividends • Converts service site from “B of B” to “B of A” for higher reimbursement STOCKS AND DIVIDENDS

SLICK Comprehensive(AKA rent a hospital license) • Converts a doctors office to a hospital • out patient facility. • Subleases a portion of the facility back • to the doctor as a “doctors office” • Charges hospital rates for the drugs • and the “facility services” DOCTORS OFFICE HOSPITAL OUTPATIENT FACILITY • Adds a facility fee for cancer • Chemotherapy infusion • Develops value for a • $300,000,000 sale to Wonder • Drug International which, • Manufactures cancer drugs.

Part B of B vs Part B of ACancer Chemotherapy INDEPENDENT PROVIDER HOSPITAL OUT-PATIENT OUT-PATIENT Chemotherapy Infusion 96410 100110 Room Fee zero 220 IV start 20 55 Infusion Pump zero 122 Piggyback antiemetic 5 110 Chemotherapy Drug Fee 95% of AWP Hosp prices Valet parking N/A included

Wunderkind Dialysis • Manufactures dialysis machines • Owns dialysis centers • Contracts with Nephrologists to manage clinic patients • Owns an ESRD lab • Adds extra “Part B” lab income to its “Part A” composite payment LAB

Vertical integration’s Golden Rule “Whoever has the gold, makes the rules”

Vertical Integration’s Paradigm Shift Hospitals are righteous institutions serving community need. Their costs may be properly supported as a matter of public policy. Hospitals now battle to capture market share, employ primary care physicians, and maximize their bottom line.

Vertical Integration’sParadigm Shift Physicians as controlled employees Physicians as righteous independent agents MD Dr. Smith

Vertical Integration’sParadigm Shift Physician Employee bound to Integrated Entity Independent Physician as Medicare Omdudsman MD Dr. Smith

SOLUTIONS • Use out patient DRG’s for payment • Pay for non-critical outpatient services the same regardless of ownership • Eliminate cost report payment methodology • Eliminate Vertical Integration costs from hospital cost reports • Restrict Vertical Integration to managed care only. TRASH

SOLUTIONS Con’t • Penalize individuals responsible for hospital cost report fraud congruent to penalties for physician fraud. • Implement hospital outpatient line item charges review congruent to the carrier process • Compare and contrast hospital cost reports with hospital reports for tax free bond funding • Ask the IRS to review the methodolgy for physician practice valuation as it relates to possible inurement • Ask the IRS office of Exempt Organizations to consider the Medicare trust fund within its review process of hospital health system tax free license applications.

SUMMARY vertical integration Vertical Integration of hospitals and independent physicians is financed with Medicare funds. Payment differentials for the same service based on ownership must be revisited due to the paradigm shift of vertical integration. Medicare Trust Fund

Off-site hospital clinics Physician practice purchase IRS inurement audit process Hospital marketing costs Hospital interest costs Hospital capital costs Hospital legal costs Hospital landlord functions Closure of independent practices Line item charges and frequency for “Part B of A” services Changes in physician referrals within VI entities Where To Look In The Future