Download

1 / 13

130 likes | 135 Views

Learn about the basics of Gross Domestic Product (GDP) and the three approaches used to measure it - expenditures approach, income approach, and value added approach.

E N D

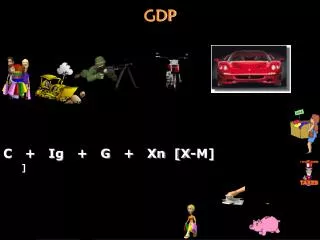

The Expenditures Approach Formula C + Ig + G + Xn C = personal Consumption in the economy • 67% of the economy! • The purchase of all finished goods and services except for new homes

C + Ig + G + Xn Ig = Gross Private Business Investment • Factory equipment maintenance • New factory equptrment • Construction of new housing • Unsold inventory of products built in a year, but not sold that year

C + Ig + G + Xn G = Government Spending • Any government purchase of products or services

C + Ig + G + Xn Xn = Net Foreign Factor of Trade (exports minus imports) • Exports = dollars in • Imports = dollars out • Since WWII, Xn is usually a negative number, AKA a trade deficit

Items that do not count towards GDP • Used goods/second-hand goods • Gifts or “transfers” (private or public) • Stock/Equity/Securities purchases • Unreported business activity conducted in cash • Illegal activities • Financial transactions between banks and businesses • Intermediate goods to avoid double counting • Ex: the wool to make a sweater is an intermediate good. The sweater is a final good. • Nonmarket activities such as volunteering

The Income Approach Formula W + R + I + P + SA W = Wages R = Rents I = Interest P = Profits SA = Statistical Adjustment

The Value Added Approach • Add together the value added for each good and service (intermediate or not) produced in an economy. • Value added is simply the difference between the cost of inputs and the price of outputs at any stage in the overall production process.