Download

1 / 8

80 likes | 97 Views

Utilize a three-month moving average and exponential smoothing with an alpha of 0.2 to forecast sales for April to June. Learn how to apply the naive method for exponential smoothing initiation.

E N D

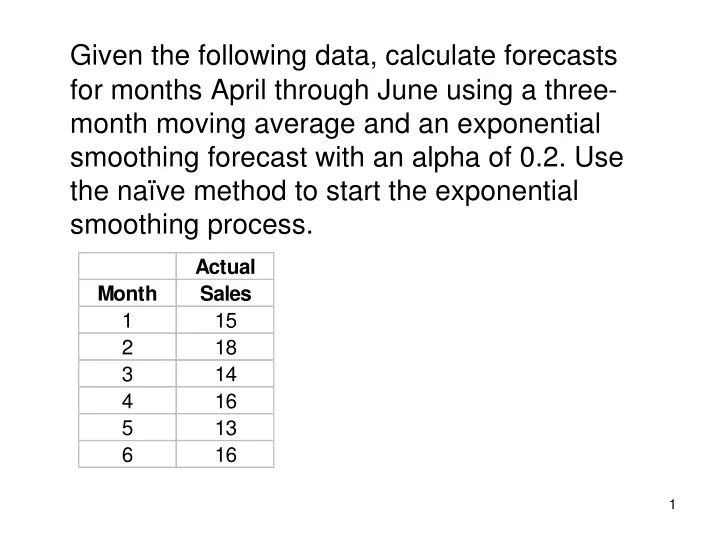

Given the following data, calculate forecasts for months April through June using a three-month moving average and an exponential smoothing forecast with an alpha of 0.2. Use the naïve method to start the exponential smoothing process.

A 3-month moving average forecast for April is the average of the actual sales figures of January, February, and March.

A 3-month moving average forecast for May is the average of the actual sales figures of February, March and April.

A 3-month moving average forecast for June is the average of the actual sales figures of March, April and May.

Using the naïve method to start the process means the forecast of February is assumed to be the actual of January (i.e., F2=A1).An exponential smoothing with a = 0.2 forecast for March is computed by the formula a x Actual of February + (1-a) x Forecast of February.

An exponential smoothing with a = 0.2 forecast for April is computed by the formula a x Actual of March + (1-a) x Forecast of March. The forecast of March is its exponential smoothing forecast computed in the previous slide.

An exponential smoothing with a = 0.2 forecast for May is computed by the formula a x Actual of April + (1-a) x Forecast of April. The forecast of April is its exponential smoothing forecast computed in the previous slide.

An exponential smoothing with a = 0.2 forecast for June is computed by the formula a x Actual of May + (1-a) x Forecast of May. The forecast of May is its exponential smoothing forecast computed in the previous slide.