Download

1 / 21

210 likes | 403 Views

BENEFITS OF MORTGAGE INSURANCE . Presented by: MGIC, Suzanne LaCaria, Senior Account Manager Essent , Donny Rosenthal, Senior Account Manager Radian, Randi Gocinski, Senior Account Manager. Private MI Premium plans. Monthly Singles - Borrower-paid - Lender-paid Splits.

E N D

BENEFITS OF MORTGAGE INSURANCE • Presented by: • MGIC, Suzanne LaCaria, Senior Account Manager • Essent, Donny Rosenthal, Senior Account Manager • Radian, Randi Gocinski, Senior Account Manager

Private MI Premium plans • Monthly • Singles - Borrower-paid - Lender-paid • Splits

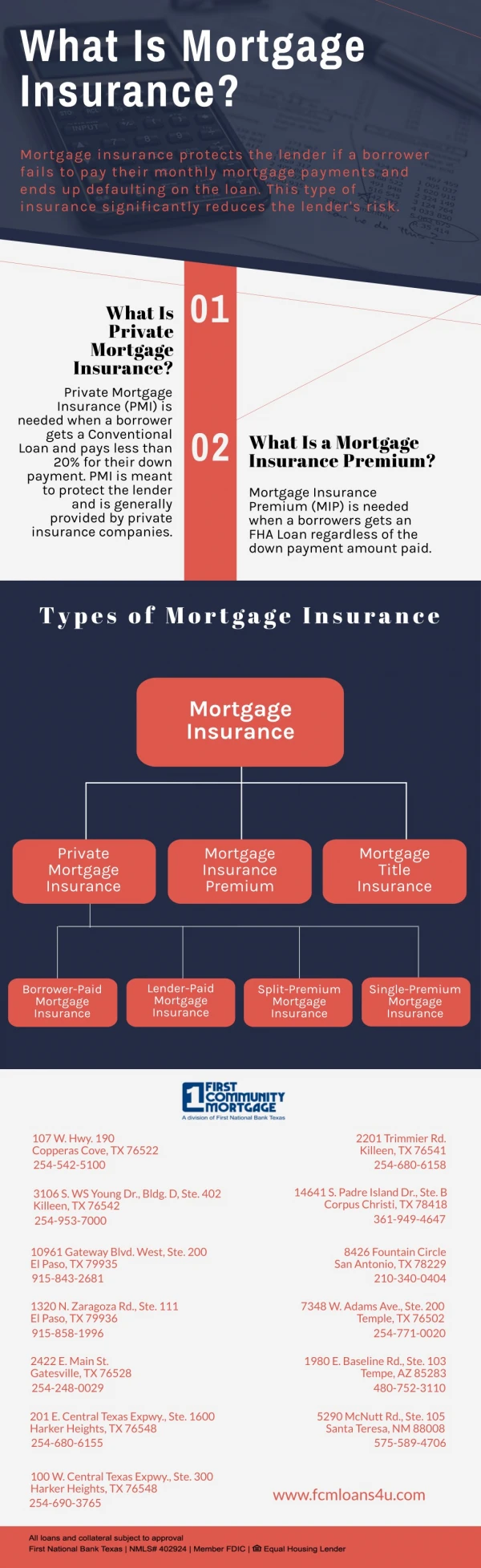

Monthly MI • Paid monthly w/mortgage payment • Versatile • May be cancelled • No up-front costs

Single Premium – Borrower-paid • Premium paid up front or financed into the loan amount • Paid by borrower, seller, builder or 3rd party • Portion may be refundable when cancelled (if refundable premium option is chosen) • Be aware of maximum CLTV depending on who loan is being sold to

Single Premium – Lender-paid • Paid by lender or 3rd party • Lender recoups cost via • Higher interest rate • Fees

Splits • Up-front premium combined w/lower monthly renewal • Up-front premium may be paid by borrower, 3rd party or financed • May be cancelled

MI Cancellation – original value Automatic Termination @ 78% LTV78% of original value, based solely on the initial amortization schedule Borrower requested @ 80% LTV 80% oforiginal value, based solely on the initial amortization schedule OR on the date the loan balance actually reaches 80% of the original value: no subordinate liens good payment history borrower must satisfy Lender’s requirementproperty value has not declined

MI Cancellation – current value Fannie Mae and Freddie Mac typically require: the loan must be seasoned at least 2 years AND the borrowers have an acceptable payment history AND the LTV based on a current appraisal is: 75% LTV or lower if less than 5 years have elapsed since the loan originally closed OR 80% LTV or lower the LTV if more than 5 years have elapsed since the loan originally closed

FHA to Increase MIP FHA to increase the Annual MIP by 10 bps. Effective for case numbers assigned on or after April 9, 2012. FHA to increase the UFMIP. Effective for case numbers assigned on or after April 9, 2012. Effective June 11, 2012; FHA to add additional 25 bps to mortgages with base loan amounts exceeding $625,500.

MI Payment Comparisons What you get with BPMI Monthly No Upfront Premium Rate 1.75% Upfront Premium Rate What you get with FHA Radian’s BPMI Monthly vs. FHA on an 95% LTV Assumes: Purchase transaction with a 30 year FRM , a 4.00% interest rate on Radian BPMI and 3.75% interest rate for FHA, 760 FICO MONTHLY SAVINGS of $160! Reflects FHA Rates Effective April 2012 and Radian MI Pricing as of May 1st, 2012

MI Payment Comparisons • BPMI Monthly vs. FHA on an 95% LTV Sale Price Total Monthly Payment ~ $14,500 More home for the same monthly payment! Assumptions: 30 year amortization, 720+ FICO, Purchase, Reflects FHA Rates Effective April 2012

MI Payment Comparisons What you get with Borrower Paid Single Conv. MI Upfront Premium Rate Per MI Co. 1.75% Upfront Premium Rate What you get with FHA BPMI Single Financed vs. FHA on a 95% LTV Assumes: Purchase transaction with a 30 year FRM, 740 FICO, Conv MI reflects note rate of 3.875 while FHA reflects note rate of 3.750 MONTHLY SAVINGS of $259! Reflects FHA Rates Effective April, 2012

MI Payment Comparisons What you get with FHA What you get with Borrower Paid Single Conv. MI Upfront Premium Rate per MI Co. 1.75% Upfront Premium Rate BPMI Single Financed vs. FHA on a 95% LTV Assumes: Purchase transaction with a 30 year FRM with a 740 FICO More than 30% more home for the same monthly payment! Reflects FHA Rates Effective April, 2012

MI Payment Comparisons What you get with FHA What you get with Borrower Paid Single Conventional Upfront Premium Rate 1.75% Upfront Premium Rate BPMI Single Paid in Cash vs. FHA on a 95% LTV Assumes: Purchase transaction with a 30 year FRM, 740 FICO The same payment . . . ~$55,000 more buying power! Reflects FHA Rates Effective April , 2012

MI Payment Comparisons What you get with FHA Lender Paid MI Premium Rate 4.25% Note Rate 1.75% Upfront Premium Rate 3.75% Note Rate LPMI Single vs. FHA on a 95% LTV, with .5% increase Monthly Savings of $285! What you get with Lender Paid Singles Assumes: 740 FICO, Purchase transaction with a 30 year FRM Reflects FHA Rates Effective April , 2012

MI Payment Comparisons LPMI Premium Rate 4.25% Note Rate 1.75% Upfront Premium Rate 3.75% Note Rate What you get with Lender Paid Singles What you get with FHA Monthly Savings of $189! LPMI Singles vs. FHA on a 95% LTV, with a .75% increase P&I + MI P&I + MI $1,168 $1,357 Assumes: 740 Fico, Purchase transaction with a 30 yr FRM. Reflects FHA Rates Effective April , 2012

Close More Loans Based on a 30-year 95% LTV loan, a base loan amount of $285,000 and a FICO of 720; interest rate is 3.75% for BPMI and 3.25% for FHA (Based on April 2012 FHA MIP Increases)

BENEFITS OF MORTGAGE INSURANCE • Presented by: • MGIC, Suzanne LaCaria, Senior Account Manager • Essent, Donny Rosenthal, Senior Account Manager • Radian, Randi Gocinski, Senior Account Manager