Download

1 / 6

70 likes | 497 Views

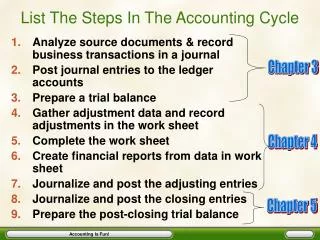

Introduction to ProBanker’s Balance Sheet. ProBanker Bank Balance Sheet. Assets. Liabilities. Rate & Fee Set Deposits : Retail Demand Deposits (DDR) Corporate Demand Deposits (DDC) Passbook Savings (PASS) 2Q Retail CD (RCD) 8Q Retail Time (IRA) Quantity Set Liabilities :

E N D

Introduction to ProBanker’s Balance Sheet

ProBanker Bank Balance Sheet Assets Liabilities Rate & Fee Set Deposits: Retail Demand Deposits (DDR) Corporate Demand Deposits (DDC) Passbook Savings (PASS) 2Q Retail CD (RCD) 8Q Retail Time (IRA) Quantity Set Liabilities: 1Q, 2Q, 4Q Wholesale CDs (CD) Federal Funds Purchased (FFP) Net Worth “Capital” (NW) Discount Window Advances (DWA) Rate & Spread Set Loans: 1Q Fixed-Rate Corporate (FR) 2Q Floating Rate Corporate (FL) 4Q Installment (INST) 8Q Mortgages (MORT) - Loan Loss Allowance (LLA) Quantity Set Assets: Reserves (RR + ER) 1Q to 8Q Bonds (BOND) Federal Funds Sold (FFS) Fixed Assets (FA)

Determining rates or fees on “customer” deposits • Begin by pricing them off of the bank’s marginal cost of deposit funding. In most cases this will be the equivalent maturity wholesale CD rate (e.g., LIBOR). For a sound bank, this rate equals the equivalent maturity government bond yield. • Add to this wholesale CD rate the annualized CD operating cost and the FDIC deposit insurance premium to get an all-in cost of the CD, say rCD. • From rCD, you can make sure you never pay more on PASS, RCD, IRA, DDR, and DDC taking into account their annualized operating and advertising costs, and FDIC assessment. • DDR and DDC have zero rates, but you need to set fees to cover the cost of reserve requirements in addition to their other costs. There costs should not be more than rCD(1-), where = 10%.

Determining rates or spreads on “customer” loans • Starting with rCD , recall that a bank’s return on equity is • or rearranging this we find the the rate on non-reserve assets is • Given that ROE should be at least equal to the 1Q CD rate, we can make sure that the return on customer loans equals at least rN,where rN is the loan rate net of annualized operating and advertising expenses and the expected loan default rate.

Provision for Loan Losses and LLA • LLA is a contra asset that should be management’s best guess of losses from default on the bank’s current loans. Management adjusts it by setting the Provision for Loan Losses (PLL). • Bank regulators examine banks and will assess a penalty for forcing the bank to increase PLL if LLAt is inadequate. Note that PLL is an expense that reduces net income. • Regulators require that LLAt be at least a given proportion of the bank’s Non-Performing Loans. See Economic Environment Report for regulators’ required LLA.

Adequate capital (NW) • Without adequate capital, a bank could end up paying a default risk-premium on CDs and FFP and could also lose DDC. • The Basel Capital Standards define Risk-Weighted-Assets as • Tier I Capital equals NW. Tier II Capital equals LLA (and subordinated debt) up to 1.25% of RWA. Letting TA be total assets, adequate capital then requires