Download

1 / 10

100 likes | 111 Views

Many consumers today are wondering which card program is superior over the other. But in truth, secured credit cards are not necessarily better than unsecured credit cards, and vice-versa. After all, credit cards are not made one and the same. In fact, these lines of credit are designed to meet the widely-varying needs, spending habits, and financial capabilities of consumers.<br><br>Check our review of unsecured credit cards for bad credit https://www.newhorizon.org/Info/unsecured.htm

E N D

What Should I Sign up for – Secured or Unsecured Credit Cards?

Many consumers today are wondering which card program is superior over the other. But in truth, secured credit cards are not necessarily better than unsecured credit cards, and vice-versa. After all, credit cards are not made one and the same. In fact, these lines of credit are designed to meet the widely-varying needs, spending habits, and financial capabilities of consumers. Still, if you’re interested to know how you can pick an excellent line of credit among all the card programs offered in the market, then we suggest that you pay close attention to the paragraphs below.

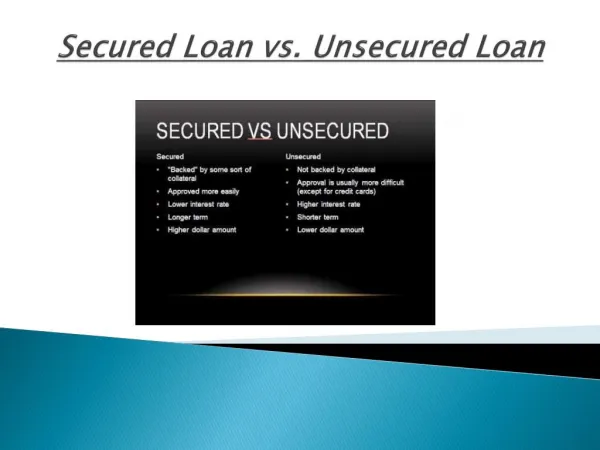

You don’t wish to make huge payments on interest. This is because secured cards tend to carry the lowest interest rates of all card programs available in the market. No wonder these lines of credit are often considered the cheaper alternatives to unsecured card accounts.

You don’t mind making a huge initial deposit to your card issuer. Secured lines of credit in general require the provision of collateral or security to guarantee repayment. In the case of secured card accounts, issuers will surely ask you to make an initial deposit before you can be granted a line of credit. Your initial deposit serves two important functions. First, it guarantees the repayment of your future credit card charges. In case you default on your credit card bills, your issuer can easily tap on the security deposit you have provided to settle all your unpaid charges. Second, it serves as the basis for the spending limit that will be imposed on your card account. For instance, if you were asked to make a deposit of $800 then you can use as much as $800 on your secured line of credit.

You have impulse buying or uncontrolled spending problems. After all, secured cards usually have low spending limits which will surely discourage you from buying on impulse and indulging in lavish shopping sprees. This is because should you exceed the limit set on your credit card, for sure you will be penalized with huge overdraft charges and declined transaction fees – pesky fines that might eat up a significant percentage of your monthly budget.

You plan to charge all your personal and household expenses on your credit card. This is because unsecured cards tend to have high spending limits. So, there’s no need for you to worry about charging huge transactions on your line of credit.

You can afford to pay high interest charges. After all, unsecured card programs usually carry high interest rates – a feature that card issuers use to compensate for the absence of a security or guarantee for repayment.

You have excellent credit standing. This is because most card issuers today extend unsecured lines of credit ONLY to consumers who have good- to excellent credit standing. This way, they can be assured that their cardholders will live up to the terms and conditions of their card programs and that they will pay their credit card bills on time and in full, each month.