Download

1 / 28

350 likes | 754 Views

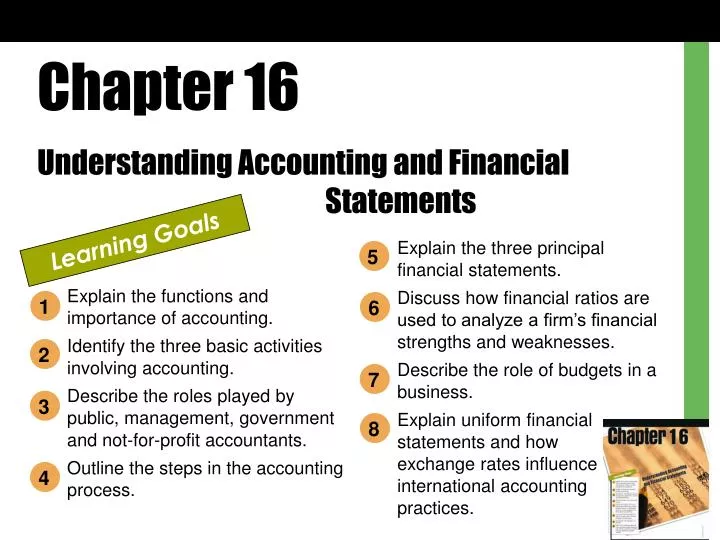

Chapter 16 Understanding Accounting and Financial Statements. Learning Goals. Explain the three principal financial statements. Discuss how financial ratios are used to analyze a firm’s financial strengths and weaknesses. Describe the role of budgets in a business.

E N D

Chapter 16 Understanding Accounting and Financial Statements Learning Goals Explain the three principal financial statements. Discuss how financial ratios are used to analyze a firm’s financial strengths and weaknesses. Describe the role of budgets in a business. Explain uniform financial statements and how exchange rates influence international accounting practices. 5 Explain the functions and importance of accounting. Identify the three basic activities involving accounting. Describe the roles played by public, management, government and not-for-profit accountants. Outline the steps in the accounting process. 1 6 2 7 3 8 4

Accounting Process of measuring, interpreting, and communicating financial information to support internal and external business decision making. • USERS OF ACCOUNTING INFORMATION

• Open book management Sharing sensitive financial information with employees and teaching them how to understand and use financial statements. • • Viewing financial information may help them better understand how their work contributes to the company’s success. • • Outsiders use financial data to evaluate investment opportunities. • • Accountants serve public good. • • Example: Volunteer programs that provide free help for low- and middle-income senior citizens file their taxes.

BUSINESS ACTIVITIES INVOLVING ACCOUNTING • • Accounting plays a key role in each of a businesses three key areas: • • Financing activities Provide necessary funds to start and expand a business. • • Investing activities Provide valuable assets required to run a business. • • Operating activities Focus on selling goods and services, but they also consider expenses as important elements of sound financial management.

ACCOUNTING PROFESSIONALS • Public Accountants • Public accountant Accountant who works for an independent accounting firm. • • Provide three basic services to clients: • • Auditing, or examining, financial records. • • Tax preparation, planning, and related services. • • Management consulting for an independent accounting firm. • • Four largest firms dominate the industry: Deloitte & Touche, Ernst & Young, KPMG, and PricewaterhouseCoopers. • • Legislation limits the types of consulting services auditors can provide. • Certified public accountant (CPA) Accountant who meets specified educational and experiential requirements and has passed a comprehensive examination on accounting theory and practice.

Management Accountants • • Management accountant Accountant employed by a business other than a public accounting firm. • • Collects and records financial transactions and prepares financial statements used by the firm’s managers in decision making. • • Answers questions such as: • Where is the company going? • • What opportunities await it? • • Do certain situations expose the company to excessive risk? • • Does the firm’s information system provide detailed and timely information to all levels of management? • • Often specialize (e.g., internal auditor, tax accountant). • Government and Not-for-Profit Accountants • • Perform professional services similar to those of management accountants.

THE ACCOUNTING PROCESS • Accounting process Set of activities involved in converting information about transactions into financial statements.

The Impact of Computers and the Internet on the Accounting Process • • Simplifies the accounting process by automating data entry and calculations. • • Available products are customized for businesses of different sizes. • • Entrepreneurs and small businesses: QuickBooks, Peachtree, and BusinessWorks. • • Larger firms: Computer Associates, Oracle, and SAP. • • Software that handles accounting information for international businesses is also available. • • Some systems are Web-based.

The Foundation of the Accounting System • • Generally accepted accounting principles (GAAP) Principles that encompass the conventions, rules, and procedures for determining acceptable accounting practices at a particular time. • • Financial Accounting Standards Board (FASB) Organization primarily responsible for evaluating, setting, or modifying GAAP in the U.S. • • Monitors changing business conditions. • • Enacts new rules. • • Modifies existing rules when necessary.

Sarbanes-Oxley Act A response to cases of accounting fraud. • • Created the Public Accounting Oversight Board, which sets audit standards and investigates and sanctions accounting firms that certify the books of publicly traded firms. • • Added to the reporting requirements for publicly traded companies. • • Senior executives must personally certify that the financial information reported by the company is correct. • • Resulted in increase in demand for accountants.

The Accounting Equation • Assets Anything of value owned or leased by a business. • • Tangible: Equipment, buildings, inventory. • • Intangible: Patents, trademarks • Liability Claim against a firm’s assets by a creditor. • Owner’s equity All claims of the proprietor, partners, or stockholders against the assets of a firm, equal to the excess of assets over liabilities. • Basic accounting equation Relationship that states that assets equal liabilities plus owners’ equity. • Double-entry bookkeeping Process by which accounting transactions are entered; each individual transaction always has an offsetting transaction.

FINANCIAL STATEMENTS • • Provide managers with information for evaluating organization’s ability to meet current obligations and needs, its profitability, and its overall financial health. • The Balance Sheet • Balance sheet Statement of a firm’s financial position—what it owns and the claims against its assets—at a particular point in time.

The Income Statement • Income statement Financial record of a company’s revenues, expenses, and profits over a period of time. • • Helps decision makers focus on overall revenues and the costs involved in generating these revenues. • • Sometimes called a profit-and-loss, or P&L, statement. • This gentleman has clearly encountered more loss than profit….

The Statement of Cash Flows • Statement of cash flows Statement of a firm’s cash receipts and cash payments that presents information on its sources and uses of cash. • Accrual accounting Accounting method that records revenue and expenses when they occur, not necessarily when cash actually changes hands. • • Inadequate cash flow is a reason for many business failures.

FINANCIAL RATIO ANALYSIS • • Ratio analysis Tool for measuring a firm’s liquidity, profitability, and reliance on debt financing, as well as the effectiveness of management’s resource utilization.

Liquidity Ratios • • Liquidity ratios Firm’s ability to meet short-term obligations when they must be paid. • • Current ratio compares current assets to current liabilities. • • Example: Shasta • • Ratio of 2 to 1 is generally considered to indicate satisfactory liquidity. Total current assets Total current liabilities

• Acid-test (or quick) ratio measures the ability of a firm to meet its debt payments on short notice. • • Example: Shasta Cash and equivalents + short-term investments + accounts receivable Total current liabilities

Activity Ratios • • Activity ratios Measure the effectiveness of management’s use of the firm’s resources. • • Inventory turnover ratio indicates the number of times merchandise moves through a business. • • Example: Shasta • • Inventory turnover rates can vary widely from industry to industry. Net sales Average of inventory 1/31/07 and 1/31/06

• Total asset turnover ratio indicates how much in sales each dollar invested in assets generates. • • Example: Shasta • • Higher ratios indicate greater efficiency. Net sales Average of total assets 1/31/07 and 1/31/06

Profitability Ratios • • Profitability ratios Measure the organization’s overall financial performance by evaluating its ability to generate revenues in excess of operating costs and other expenses.

Leverage Ratios • • Leverage ratios Measure the the extent to which a firm relies on debt financing. • • Total liabilities to total assets ratio > 50 percent indicates that a firm is relying more on borrowed money than owners’ equity.

BUDGETS • Budget Planning and control tool that reflects a firm’s expected sales revenues, operating expenses, and cash receipts and outlays. • • Preparation is generally time-consuming, involving people throughout the organization. • • Cash budget Tracks the firm’s cash inflows and outflows.

INTERNATIONAL ACCOUNTING • • Global firms must translate financial statements of the firm’s international affiliates, branches, and subsidiaries and convert data about foreign currency transactions to dollars. • Exchange Rates • • Ratio at which a country’s currency can be exchanged for other currencies. • • Consolidated financial statements must reflect gains and losses due to changes in exchange rates. • • Can have significant impact on financial statement. • • Over a recent three-year period, foreign currency adjustments effectively added more than $1.5 billion to Procter & Gamble’s earnings.

International Accounting Standards • • International Accounting Standards Committee (IASC) promotes worldwide consistency in financial reporting practices. • • Working to create one worldwide set of accounting rules.