Download

1 / 29

290 likes | 502 Views

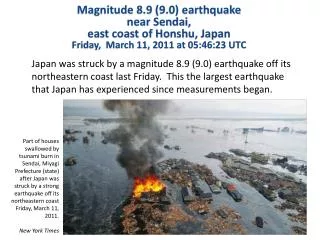

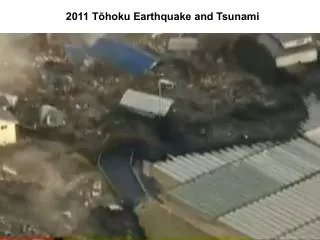

Sendai Earthquake and Tsunami First-Party Coverage Implications June 22, 2011. Presented by: Jeffrey S. Weinstein Mound Cotton Wollan & Greengrass.

E N D

Sendai Earthquake and TsunamiFirst-Party Coverage ImplicationsJune 22, 2011 Presented by: Jeffrey S. Weinstein Mound Cotton Wollan & Greengrass

The following presentation is for educational purposes only and is not intended for any other use. It does not represent the view of any firm, insurer, or reinsurer.

What is a Captive Insurer? • An insurer wholly-owned by another organization (generally noninsurance), the main purpose of which is to insure the risks of the parent organization (Single Parent Captives) http://www.guycarp.com/portal/extranet/utility/glossary_c.html • Other arrangements: • Association Captives - owned by a trade, industry, or service group for benefit of members • Group Captives - jointly owned by a number of companies; created to provide a vehicle to meet common insurance needs • Agency Captives - owned by an insurance agency or brokerage firm • Rent-a-Captives - provide “captive” facilities to other companies for a fee, while protecting itself from losses under individual programs, which are also isolated from losses under other programs within the same company; often used by companies that are too small to justify establishing their own captives • Fronting Captives

Purpose of Captives • Reduce the amount of premiums paid for coverage and to retain more control over the disposition of claims • Cost efficiency from eliminating underwriting and investment profits that would otherwise be earned by insurers • Any profit on premiums benefits the parent company and may be used to reduce future premiums

Capitalization of Captives Different captives have different capitalization structures • Some captives act as “real” direct or reinsurance writers • Some captives are mere shells and assume no true risk (Front?) • Some reinsure to other reinsurers-retrocessionaires

What is Fronting? An arrangement whereby one licensed insurer issues a policy on a risk for and at the request of an unlicensed insurer with the intent of passing the entire risk by way of reinsurance to the other insurer. Such an arrangement may be attacked if the purpose is to frustrate regulatory requirements. See http://www.guycarp.com/portal/extranet/utility/glossary_f.html

“Difference in Conditions”“Difference in Limits” • Used in master/global programs where local coverages are required • If underlying policy covers a risk, but at a smaller limit, DIC policy look like “excess” coverage • But if DIC policy covers a risk underlying policy does not, that coverage is provided at first dollar • “DIL” works more like a straight excess policy - with the focus on limits – but used in a master/global program context

US/UK DIC Market Non-Admitted Company (Captive or Other Insurer) Fronted by Licensed Insurer Insured Hypothetical Captive/Fronting Structure Question: Is this “DIC,” Reinsurance, or both? N.B. - Reinsurance Relationship

Continental Airlines • For Many (but not all) Reinsurers: • One Insured • One Occurrence • Two Claim Files DIC Local covers PD/BI CBI – not covered under Local

Claim Issues • Claims Control / Claims Cooperation Clause • Local Adjuster • Reporting Issues • Claims Handling Agreements • Steering Committee

SUBLIMITSEarthquake v. Contingent Time Element Key Policy Language: • “All Liability for loss or expense under this Policy for any one occurrence shall not exceed the smallest of . . . any applicable sublimits of liability entered elsewhere in this Policy” • Altru Health Systems v. American Protection Ins. Co., (8th Cir. 2001) – The Court held that the lesser flood sublimit, and not the civil authority sublimit, applied • “The maximum Sublimit amount collectible under this policy shall be the Sublimit applicable for all loss or damage resulting from a peril insured against by this policy, regardless of any other Sublimit involved in this policy” • Penford Corp. v. National Union Fire Ins. Co., (N.D. Iowa 2010) - The Court concluded that the policy was ambiguous with respect to what types of losses were subject to the flood sublimits

Contingent Time Element Elements of Coverage: • Necessary interruption of business? • resulting from direct physical loss or damage by a covered cause of loss? • to property of a type insured under the policy? • that prevents a supplier (or receiver) from rendering (or accepting) goods or services?

Contingent Time Element Civil Authority or Ingress/Egress Contingent Time Element provision: This policy, subject to all provisions and without increasing the limits of this policy, also insures against loss resulting from damage to or destruction by causes of loss insured against to property that wholly or partially prevents any Tier 1 or Tier 2 supplier of goods and/or services to the Insured from rendering its goods and/or services… • Requires physical damage to property (what if closure by civil authority or ingress/egress?) • The physical damage does not necessarily have to be to the supplier’s own property • By virtue of the structure of the CTE provision, if there is “damage . . . to property” but not necessarily covered damage to property, would CTE still be available? Thus, if there is earthquake damage (not necessarily to a supplier’s property) that causes a supplier not to be able to supply, then is there CTE coverage?

Contingent Time Element Civil Authority or Ingress/Egress Issue: Where a policy provides that CTE coverage arises from “direct physical loss or damage by a covered cause of loss,” is physical damage required or is loss of use sufficient to trigger coverage, such that prohibition/prevention of access under Civil Authority or Ingress/Egress provisions may provide a basis for Contingent Time Element coverage?

Contingent Time Element Civil Authority or Ingress/Egress Generally, courts recognize that physical damage is a prerequisite to CTE coverage Penton Media, Inc. v. Affiliated FM Ins. Co., (6th Cir. 2007) • The insured sustained loss of income when one of its trade shows was postponed because government agencies used the Javits Center for disaster relief following the September 11 terrorist attack • The court held that the civil authority provision did not cover the loss because the Javits Center was not a “described location” • In reaching its decision, the court observed that the loss of income was not covered under the CTE provision because the Javits Center did not itself suffer direct physical loss or damage • The court concluded that the CTE provision did not “extend the BI endorsement to cover actual losses directly resulting from prohibition of access by order of civil authority occurring at each supplier and customer”

Contingent Time Element Civil Authority or Ingress/Egress Pentair, Inc. v. American Guar. & Liab. Ins. Co., (8th Cir. 2005) • The court held that an insured was not entitled to CTE coverage where its loss was caused by loss of electricity to the supplier’s property, and not because of damage to the supplier’s property. • In reaching its decision, the court distinguished cases in which the Minnesota state courts held that functional impairment constituted “direct physical loss,” noting that, even in those cases, the insured property had been physically contaminated in some way. • The court further addressed whether loss of power could itself constitute property damage, holding that because the policy limited coverage to power outages at “Described Premises,” there was no coverage for power outages at supplier locations.

Contingent Time Element Civil Authority or Ingress/Egress as Predicate? • The wording of the policy can lead to broader coverage • Coverage would be limited to situations where a supplier’s property was physically damaged by a covered peril if the provision were re-worded to provide: This policy, subject to all provisions and without increasing the limits of this policy, also insures against loss resulting from direct physical damage or destruction, by causes of loss insured against, to propertyof a Tier 1 or Tier 2 supplier that wholly or partially prevents any Tier 1 or Tier 2 supplier of goods and/or services to the Insured from rendering its goods and/or services…

Contingent Time Element Original Wording Suggested Revisions This policy, subject to all provisions and without increasing the limits of this policy, also insures against loss resulting from direct physical damage to or destruction,by causes of loss insured against, to propertyof a Tier 1 or Tier 2 supplier that wholly or partially prevents any Tier 1 or Tier 2 supplier of goods and/or services to the Insured from rendering its goods and/or services… This policy, subject to all provisions and without increasing the limits of this policy, also insures against loss resulting from damage to or destruction by causes of loss insured against to property that wholly or partially prevents any Tier 1 or Tier 2 supplier of goods and/or services to the Insured from rendering its goods and/or services…

Contingent Time Element Territory Clause Park Electrochemical Corp. v. Continental Casualty Co., (E.D.N.Y. 2011) • US manufacturer unable to obtain necessary component from factory located in Singapore following an explosion at the factory • Contingent Time Element provision: [We] will pay for the loss resulting from necessary interruption of business conducted at Locations occupied by the Insured and covered under this policy, caused by direct physical damage or destruction to: • any real or personal property of direct suppliers which wholly or partially prevents the delivery of materials to the Insured or to others for the account of the Insured . . . • Insurer denied coverage because Singapore was not covered within the Territorial Limits of the policy • The court held that CTE provision did not cover physical damage, but financial shortfall and because the financial loss was sustained within Territorial Limits, there was coverage

Contingent Time Element Territory Clause • Auto parts manufacturer sustained no direct property damage as a result of the earthquake or tsunami, but its US facilities sustained income and extra expense losses when the plants’ primary customers, located in Japan, reduced or eliminated production • Contingent Time Element provision: This Policy covers the Actual Loss Sustained and EXTRA EXPENSE incurred by the Insured during the PERIOD OF LIABILITY: 1) directly resulting from physical loss or damage of the type insured; and • to property of the type insured, at any locations of direct suppliers or direct customers located within the TERRITORY of this Policy. • Unlike Park Electrochemical, the policy requires CTE: • result from physical loss or damage of the type insured • to “property of the type insured” • The Policy excludes Earthquake in Japan

Contingent Time Element Park Electrochemical Auto Parts Manuf. This Policy covers the Actual Loss Sustained and EXTRA EXPENSE incurred by the Insured during the PERIOD OF LIABILITY: directly resulting from physical loss or damage of the type insured; and to property of the type insured, at any locations of direct suppliers or direct customers located within the TERRITORY of this Policy. [We] will pay for the loss resulting from necessary interruption of business conducted at Locations occupied by the Insured and covered under this policy, caused by direct physical damage or destruction to: • any real or personal property of direct suppliers which wholly or partially prevents the delivery of materials to the Insured or to others for the account of the Insured . . .

Deductibles (Semiconductor manufacturer with two facilities in Sendai; sustained damage due to earthquake) • Earth Movement Deductible: 5% of the value per separate and damaged unit of insurance, subject to a minimum combined deductible of USD 25,000,000 per occurrence * * * In applying the deductible for EARTH MOVEMENT . . . value shall be determined on the same basis as is used to determine the amount of loss • “Unit of Insurance” is not defined • Reported values include: • Buildings/Leasehold Improvements • Machinery & Equipment Furniture & Fixtures • Inventory • Business Interruption

Deductibles • The determination of which deductible applies generally turns on the cause of the loss • Percent Deductibles Does the policy provide a basis for calculating the percentage deductible? • Terra-AdiInt'l Dadeland, LLC v. Zurich Am. Ins. Co., (S.D. Fla. 2007) "5% of the total insured values at risk" was found to be ambiguous as to whether it applied to the insured value of the entire project or the sub-limit for windstorm • Beverly Hills Condo, 1-12, Inc. v. Aspen Specialty Ins. Co., (S.D. Fla. 2007) Deductible provision specified that "[t]he application of a 'per location' deductible . . . is intended to apply to the TIV . . . of the entire premises, inclusive of all buildings, and is NOT applicable to a series of individual buildings regardless of the labeling in the statement of values . . ." was not ambiguous

Deductibles • Earth Movement Deductible: 5% of the value, per the VALUATION clause of the LOSS ADJUSTMENT AND SETTLEMENT section . . . at the Location where the physical damage occurred • Loss estimate $8,053,391 • Accountant applied 5% deductible on a “per location” basis ($3,655,890 deductible), rather than on the values of the entire business segment ($8,128,335) • Lead-in to Deductible provision states deductible applies on a per location basis, “if specified”; does not say where it is specified • Conclusion: apply deductible as a percentage of the value of the loss per the valuation clause, which will require assessing the damage at affected location(s) per the policy’s valuation clause

Reservation of Rights • When to Issue? • Receipt of notice • Receipt of formal claim • Early identification of potential issues • Delay to investigate (how do we look?) • Why to Issue? • Waiver potential Elizabethtown Water Co. v. Hartford Cas. Ins. Co., (D.N.J. 1998) (holding that a first-party insurer can waive its right to use an exclusion when it fails to raise it timely; whether a defense is timely will depend on whether the insured was prejudiced) Merchants Indem. Corp. v. Eggleston, (N.J. 1962) (holding that a third-party insurer can be estopped from raising a defense where it did not reserve its rights; whether notice of the defense is timely will depend upon the circumstances, in the case of a liability insurer, the court will consider whether the insurer undertook to defend the claim and whether the party that is to pay had an early opportunity to investigate) • Good faith • Does insured have a public adjuster?

Reservation of Rights • Types of Reservations of Rights • Aggressive (citing provisions with “early” indications) • Passive • Helpful (identify issues to investigate) • Tone • Measuring legal responsibility versus relationship issues • Who Issues? • Adjuster • Company • Attorney