Download

1 / 12

220 likes | 474 Views

Consumption Function. Shows the relationship between consumption and its determinants Consumption = f (disposable income, wealth, price, expected income, expected price, interest rate). Disposable income Income that remains after paying taxes

E N D

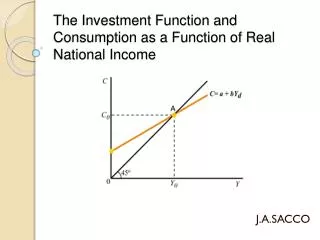

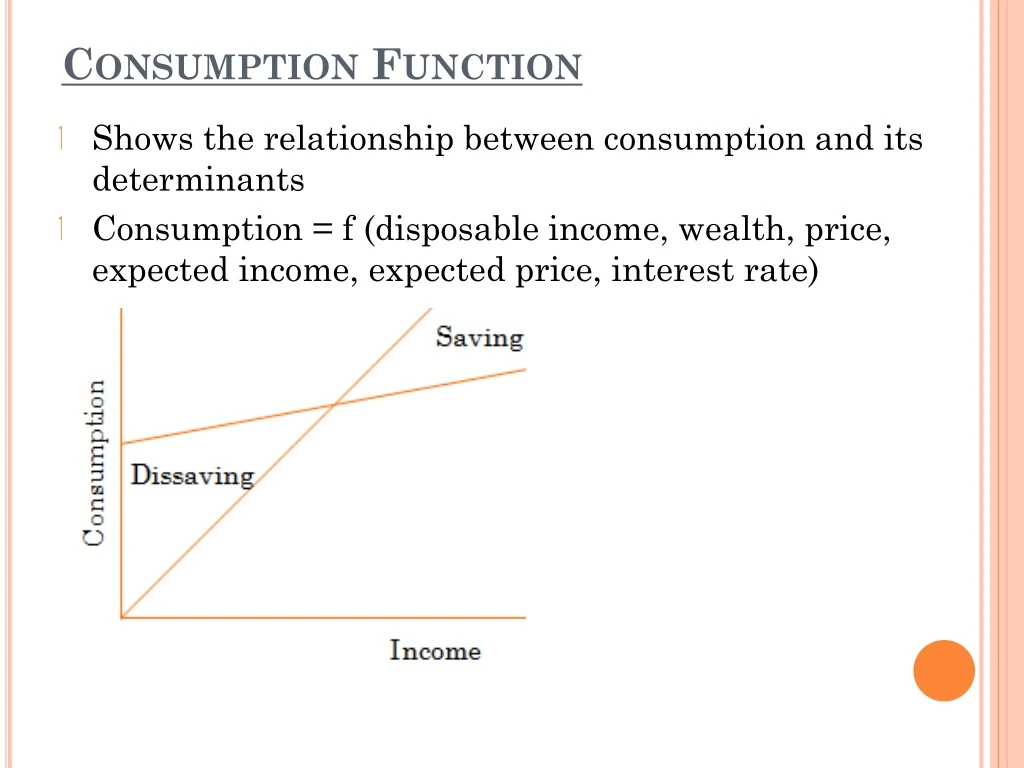

Consumption Function • Shows the relationship between consumption and its determinants • Consumption = f (disposable income, wealth, price, expected income, expected price, interest rate)

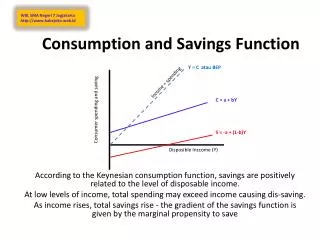

Disposable income • Income that remains after paying taxes • Disposable income is the most important variable in determining consumption • Psychological Law of Consumption • When income increases, people spend more on consumption but not by the same rate as the increase in income • Some part of the increased income is saved

Marginal Propensity to Consume (MPC) • Ratio of changes in consumption to changes in income • MPC = ∆C/ ∆Y • MPC = 1—MPS • MPS is the Marginal Propensity to Save

Saving Function • The portion of the income that is left after spending on consumption • Saving (S) = Income (Y)—Consumption (C) • Saving is a function of income just like consumption i.e. S = f(Y) • Positive relation with income • When income increases, Saving increases • When income decreases, Saving decreases

Investment Function • Does not include the transfer of ownership of an asset, for example: investing in stocks and bonds • Includes new addition to the stock of physical capital for example: land, building, machinery • New addition i.e. net investment increases aggregate demand • Increase in aggregate demand causes an increase in level of income and creates employment

Investment Multiplier • Investment multiplier = change in income / change in investment • Shows the increase in income that results due to increase in investment • The multiplier depends on marginal propensity to consume (MPC) • MPC shows the change in consumption when income changes • MPC = ∆C / ∆Y • Multiplier = 1/(1—MPC) • 0 < MPC < 1

National Income Accounting • Science of measuring aggregate output and income • Done by government to observe the changes in economic activities • National Income (NI) • Macroeconomic variable • Money value of flow of output of goods and services • Measured over a period of time • Estimate of the total economic activity in the country/region • 3 ways of measuring National Income • Product method • Income Method • Expenditure Method

Gross Domestic Product (GDP) • Value of output produced within the domestic boundaries • Measures the flow of output per time period • Exchanges and sale of second-hand goods and services are not included • GDP = market value of all final goods and services produced domestically • Gross National Product (GNP) • Value of output produced within domestic boundaries as well as outside as long as factors of production are domestic owned • GNP = GDP + Net foreign income

Product Method • Measures National Income from output/product side • Economy is divided into different sectors • Each sector contributes to the GDP • GDP = sum of all the production in each sector • Total value of output of goods and services produced • Advantages • Helps trace the origin of national income to different sectors • Shows the level of importance of each sector in the overall economy • Disadvantage • Tendency to double-count

Income Method (Sum of Factor Incomes) • Measures national income from distribution side • National income is computed as the sum of the incomes of all the individuals in the country/region • Total income generated through production of goods and services • GDP by factor income = income from employed people + profits of private sector + rent from land • These are excluded from calculations • Income not registered with Inland Revenue Department • Private transfers of money from one person to another • Transfer payments eg- pension, unemployment insurance etc.

Expenditure Method (Aggregate Demand) • Spending on domestic produced goods and services at current market prices • GDP = C+I+G+X—M • C= Consumer/household spending • I= Private Investment spending • G= Government spending • X=exports of goods and services • M= imports of goods and services

Difficulties in Measuring National Income • Lack of statistical data • Non-monetized sectors • Illiteracy/Ignorance • Lack of Occupational Specialization • Frequently changing prices • Double and multiple counting • Shadow/Underground Economy • Some goods and services do not have money value