Download

1 / 30

300 likes | 318 Views

Learn about bond markets, types of bonds, pricing, yields, risks, ratings, yield curve, and more. Discover how to calculate bond prices and yields with practical examples and insights for informed investment decisions.

E N D

Chapter 12 BOND PRICES AND YIELDS Figuring out the Assured Returns

OUTLINE • Changes in Bond Market • Bond Characteristics • Bond Prices • Bond Yields • Risks in Bonds • Rating of Bonds • The Yield Curve • Explaining the Term Structure • Determinants of Interest Rates • Analysis of Convertible Bonds

CHANGES IN DEBT MARKET THEN NOW • PLAIN VANILLA BONDS • BONDS WITH COMPLEX FEATURES • STABLE & ADMINISTERED • VOLATILE & MARKET- INTEREST RATES DETERMINED INTEREST RATES • SIMPLISTIC MEASURES OF • PRECISE MEASURES OF RETURN & LIFE RETURN & LIFE • RULES OF THUMB • ANALYTICAL METHODS • FEW PLAYERS • MORE PLAYERS • PASSIVE APPROACH • RELATIVELY MORE ACTIVE APPROACH • ILLIQUID MARKET • LIQUID MARKET ? • ABSENCE OF A REFERENCE • EMERGENCE OF A REFERENCE RATE RATE

BOND CHARACTERISTICS • A BOND IS AN IOU. IT IS DESCRIBED IN TERMS OF: • PAR VALUE • COUPON RATE • MATURITY DATE • GOVERNMENT BONDS ALSO CALLED GOVERNMENT • SECURITIES (G-SECS) OR GILT-EDGED SECURITIES. • THESE ARE GENERALLY MEDIUM TO LONG-TERM • BONDS ISSUED BY RBI ON BEHALF OF THE • GOVERNMENT OF INDIA AND STATE GOVERNMENTS. • CORPORATE BONDS OR CORPORATE DEBENTURES ARE • DEBT INSTRUMENTS ISSUED BY COMPANIES

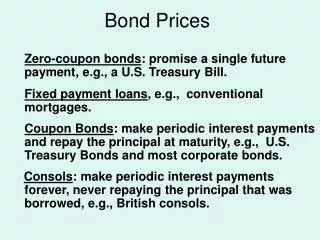

TYPES OF BONDS • STRAIGHT BONDS • ZERO COUPON BONDS. • FLOATING RATE BONDS • BONDS WITH EMBEDDED OPTIONS • COMMODITY-LINKED BONDS

BOND PRICING (VALUATION) nCMP = +t=1 (1+r)t (1+r)n 2nC/2 MP = +t=1 (1+r/2)t (1+r/2)2n

BOND PRICING A RS.600 FACE VALUE BOND CARRIES A COUPON RATE OF 12 PERCENT P.A. PAYABLE SEMI-ANNUALLY. THE BOND IS REDEEMBALE AT PAR AFTER 5 YEARS. IF INVESTORS REQUIRE A RETURN OF 9% PER HALF-YEAR PERIOD, WHAT WILL BE THE PRICE OF THE BOND.10 36 600P0 = +t=1 (1.09)t (1.09)10 = 36 x 6.418 + 600 x 0.422 = RS.484.25 1 – F P = C +r (1+r)n 36 x 6.418 + 600 x 0.422 = 484.25 1 (1+r)n

PRICE - YIELD RELATIONSHIP PRICE YEILD PRICE CHANGES WITH TIMEVALUE OF BOND PREMIUM BOND: rd = 11% A PAR VALUE BOND: rd = 13% B DISCOUNT BOND: rd = 15% 8 7 6 5 4 3 2 1 0 YEARS TO MATURITY

BOND PRICE THEOREMS 1. BOND PRICES & YIELDS MOVE IN OPPOSITE DIRECTIONS 2. BOND PRICES ARE MORE SENSITIVE TO YIELD CHANGES THE LONGER THEIR MATURITIES 3. THE PRICE SENSITIVITY OF BONDS TO YIELD CHANGES INCREASES AT A DECREASING RATE WITH MATURITY 4. HIGH COUPON BOND PRICES ARE LESS SENSITIVE TO YIELD CHANGES THAN LOW COUPON BOND PRICES 5. WITH A CHANGE IN YIELD OF A GIVEN NUMBER OF BASIS POINTS, THE ASSOCIATED PERCENT GAIN IS LARGER THAN THE PERCENT LOSS.

BOND YIELDS • CURRENT YIELDANNUAL INTEREST PRICE • YIELD TO MATURITYCC CMP = + + …. + (1+r) (1+r)2 (1+r)n (1+r)n 8 90 1,000 800 = +t=1 (1+r)t (1+r)8 AT r = 13% … RHS = 808 AT r = 14% … RHS = 768.1 808 - 800 YTM = 13% + (14% - 13%) = 13.2% 808 - 768.1C + (M - P) / n YTM ≃ 0.4M + 0.6 P • YIELD TO CALLn* C M*P = +t=1 (1+r)t (1+r)n

YTM • SOMEONE WHO INVESTS IN A COUPON - PAYING BOND WILL EARN THE YTM PROMISED ON THE PURCHASE DATE IF AND ONLY IF ALL OF THE FOLLOWING THREE CONDITIONS ARE FULFILLED • THE BOND IS HELD UNTIL IT MATURES RATHER THAN BEING SOLD AT A PRICE WHICH DIFFERS FROM ITS FACE VALUE BEFORE ITS MATURITY • THE BOND DOES NOT DEFAULT • ALL CASHFLOWS ARE RE-INVESTED AT AN INTEREST RATE EQUAL TO THE PROMISED YTM

REALISED YIELD TO MATURITY FUTURE VALUE OF BENEFITS (1+r*)5 = 2032 / 850 = 2.391r* = 0.19 OR 19 PERCENT

RISKS IN BOND INVESTMENT • INTEREST RATE RISK INTEREST BOND (MARKET RISK) RATE PRICE • REINVESTMENT INTEREST RATE ON RISK INTERIM CASH FLOW • DEFAULT RISK ISSUER MAY DEFAULT (CREDIT RISK) • INFLATION RISK PURCHASING POWER RISK • CALL RISK ISSUER MAY RECALL THE BONDS • EXCHANGE RATE RISK A NON-RUPEE DENOMINATED BOND • LIQUIDITY RISK MARKETABILITY RISK • EVENT RISK ISSUER’S ABILITY.. CHANGE.. UNEXPECTEDLY (a) A NATURAL ACCIDENT OR (b) .. CORP. RESTR’G

DEBT RATING • WHAT IS IT ? • PROBABILITY OF TIMELY PAYMENT OF INTEREST & PRINCIPAL BY A BORROWER • WHAT IT ‘IS NOT’ ? • NOT A RECOMMENDATION • NOT A GENERAL EVAL’N OF THE ISSUING ORGANISATION • NOT A ONE-TIME EVALUAT’N CREDIT RISK . . VALID ENTIRE LIFE • HOW IS IT DONE ? • INDUSTRY & BUS ANALYSIS. FINANCIAL ANALYSIS • QUANTITATIVE RATING MODELS • VALUE OF RATINGS ? • RATING SCENARIO ?

FUNCTIONS OF DEBT RATING • DEBT RATINGS (OR DEBT RATING FIRMS) ARE SUPPOSED TO : • PROVIDE SUPERIOR INFORMATION • OFFER LOW-COST INFORMATION • SERVE AS A BASIS FOR A PROPER RISK-RETURN TRADEOFF. • IMPOSE HEALTHY DISCIPLINE ON CORPORATE BORROWERS. • LEND GREATER CREDENCE TO FINANCIAL AND OTHER REPRESENTATIIONS. • FACILITATE THE FORMULATION OF PUBLIC POLICY GUIDELINES ON INSTITUTIONAL INVESTMENT.

CREDIT RATING • CRISIL’S RATING SYMBOLS • AAA : HIGHEST SAFETY • AA : HIGH SAFETY • A : ADEQUATE SAFETY • BBB : LOW SAFETY • BB : INADEQUATE SAFETY • B : HIGH RISK • C : SUBSTANTIAL RISK • D : IN DEFAULT • KEY FACTORS CONSIDERED IN CREDIT RATING • INDUSTRY & BUSINESS ANALYSIS FINANCIAL ANALYSIS • • GROWTH RATE & REL’N WITH THE ECONOMY • EARNING POWER • • INDUSTRY RISK CHARACTERISTICS • BUSINESS & FINANCIAL RISKS • • STRUCTURE OF INDUSTRY & NATURE • ASSET PROTECTION OF COMPETITION • • COMPETITIVE POSITION OF THE ISSUER • CASH FLOW ADEQUACY • • MANAGERIAL CAPABILITY OF THE ISSUER • FINANCIAL FLEXIBILITY • • QUALITY OF ACCOUNTING

THE YIELD CURVE THE YIELD CURVE., OR THE TERM STRUCTURE OF INTEREST RATES, SHOWS HOW YTM IS RELATED TO TERM TO MATURITY FOR BONDS THAT ARE SIMILAR IN ALL RESPECTS, EXPECTING MATURITY. YIELD CURVE YIELD TO MATURITY (YTM) 14.0 13.0 12.0 1 2 3 4 5 TERM TO MATURITY (YRS)

TYPES OF YIELD CURVEYTM A. UPWARD SLOPINGYTM B. DOWNWARD SLOPING TERM TERM YTM C. FLAT YTM D. HUMPED TERM TERM

ILLUSTRATIVE DATA FOR GOVERNEMNT SECURITIES Face Value Interest Rate Maturity (years) Current Price Yield to maturity 100,000 0 1 88,968 12.40 100,000 12.75 2 99,367 13.13 100,000 13.50 3 100,352 13.35 100,000 13.50 4 99,706 13.60 100,000 13.75 5 99,484 13.90

FORWARD RATES 88968100000 • ONE - YEAR TB RATE 100000 88968 = r1 = 0.124 (1 + r1) • 2 - YEAR GOVT. SECURITY 12750 112750 99367 = + + r2 = 0.1289 (1.124) (1.124) (1 + r2) • 3 - YEAR GOVT. SECURITY 13500 13500 113500 100352 = + + (1.124) (1.124) (1 .1289) (1.124) (1.1289) (1 + r3) r3 = 0.1512

FORWARD RATES • 4-YEAR GOVERNMENT SECURITY

EXPLAINING THE TERM STRUCTURE • EXPECTATIONS THEORY • LIQUIDITY PREFERENCE THEORY • PREFERRED HABITAT THEORY • MARKET SEGMENTATION THEORY

EXPECTATIONS THEORY SHAPE …. YIELD CURVE … DEPENDS ON .. EXPECTATIONS … THOSE WHO PARTICIPATE … MARKET (1 + tRn) = [ (1 + tR1) (1 + t+1R1) … (1 + t+n-1Rn)]1/n YIELD CURVE EXPLANATION ASCENDING SHORT-TERM RATES RISE IN FUTURE DESCENDING SHORT-TERM RATES … FALL IN FUTURE HUMPED SHORT-TERM RATES … RISE …. FALL FLAT SHORT-TERM RATES . . UNCHANGED IN FUTURE

LIQUIDITY PREFERENCE THEORY FORWARD RATES SHOULD INCORPORATE INTEREST RATE EXPECTATIONS AS WELL AS A RISK (OR LIQUIDITY) PREMIUM (1 + tRn) = [ (1 + tR1) (1 + t+1R1+L2) … (1 + t+n-1Rn +Ln)]1/n AN UPWARD-SLOPING YIELD CURVE SUGGESTS THAT FUTURE INTEREST RATES WILL RISE (OR WILL BE FLAT) OR EVEN FALL IF THE LIQUIDITY PREMIUM INCREASES FAST ENOUGH TO COMPENSATE FOR THE DECLINE IN THE FUTURE INTEREST RATES

PREFERRED HABITAT THEORY INVESTORS PREFER TO MATCH THE MATURITY OF INVESTMENT TO THEIR INVESTMENT OBJECTIVE BORROWERS . . TOO IF MISMATCH … INDUCEMENT TO SHIFT MARKET SEGMENTATION THEORY EXTREME FORM OF PREFERRED HABITAT THEORY

DETERMINANTS OF INTEREST RATES • INFLATION RATE • REAL GROWTH RATE • TIME PREFERENCE • SHORT-TERM RISK-FREE RATE • DEFAULT PREMIUM • BUSINESS RISK • FINANCIAL RISK • COLLATERAL • MATURITY PREMIUM • FUTURE EXPECTATIONS • LIQUIDITY PREFERENCE • PREFERRED HABITAT INTEREST RATE • SPECIAL FEATURES • CALL/PUT FEATURE • CONVERSION FEATURE • OTHER FEATURES

VALUATION OF CONVERTIBLE BONDS VALUE OF THE STRAIGHT CONVERSION OPTION CONVERTIBLE = MAX BOND VALUE + VALUE BOND VALUE , VALUATION OF CONVERTIBLE BONDS A. STRAIGHT DEBT VALUE B. CONVERSION VALUE C. VALUE OF CONVERTIBLE BOND FIRM VALUE FIRM VALUE FIRM VALUE VALUEOFCONVERTIBLE BONDS CONVERTIONVALUE STRAIGHT DEBTVALUE

SUMMING UP • The debt market in India has registered an impressive growth • particularly since mid-1990s and has been accompanied by • increasing complexity in instruments,interest rates, methods of • analysis, and so on • The value of a noncallable, nonconvertible bond is: • nCM • P = + • t =1 (1+ r)t (1 + r)n • The commonly employed yield measures are : current yield, yield • to maturity (YTM), yield to call, and realised yield to maturity. • The YTM of a bond is the discount rate that makes the present • value of the cash flows receivable from owning the bond equal to • the price of the bond.

Bonds are subject to diverse risks, such as interest rate risk, • inflation risk, real interest rate risk, default risk, call risk, and • liquidity risk. • Default risk or credit risk is reflected in credit rating of debt • instruments. • The term structure of interest rates, popularly called the yield • curve, shows how yield is related to maturity. • Three principal explanations have been offered to explain the term • structure of interest rates : expectations theory, liquidity • preference theory, and preferred habitat theory. • The interest rate is determined by four factors : short-term risk- • free interest rate, maturity premium, default premium, and • special features. • Convertible bonds may be viewed as a debenture – warrant • package.