Download

1 / 16

160 likes | 177 Views

This article provides an overview of remittances from South Africa to the Southern African Development Community (SADC) region, including the size of the migrant population, remittance amounts, and the cost of remittances. It also discusses the impact of remittances on countries like Lesotho and highlights the Shoprite Money Transfers service as a popular remittance channel.

E N D

Remittances from South Africa to SADC Geoff Orpen 26 March 2015

About FinMark Trust and its focus areas • Independent trust formed in April 2002 • Initial and core funding from the UKAid • Mission: “Making Financial Markets Work for the Poor” • Aim: Facilitating and catalysing development around access to financial services • How: move beyond data production, with an increased focus on being a catalyst to systemic change in financial inclusion by providing support to transformation at a country level Focus areas Information and Research Support Micro-insurance Consumer Financial Empowerment Regional Financial Integration Financial Policy and Regulation Retail payments systems Housing Finance Rural / agricultural finance Cross cutting themes: Savings Credit SMME access 2

Remittances are defined as non-reciprocal transfers from one person to another across a distance (generally cross-border) of relatively low value usually cash to cash Outcomes of recent Surveys on Remittances: migrants send money home to service their family’s basis needs, to pay for school fees, rent or transport, or to meet unexpected costs 80% of migrants send cash remittances at least once every three months (frequency depends largely on the remitters’ capacity to save enough money) average amounts sent home by migrants to be between R500 and R1,000 for each send only 2% of remittances are sent through official banking channels, almost 70% are sent via buses or taxi drivers, 20% are sent back with visiting family or friends and about 8% through other channels Remittances: An Overview

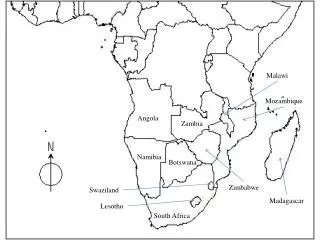

Source: DNA calculations, drawing on various sources Estimated size of the migrant population

Shoprite Money Transfers The South Africa Case Study The South African Market (2012) • 13 million adults make up the unbanked market segment • R19 billion is the estimated value of cash-to-cash person-to-person money transfers uncaptured by the formal sector (Retailers, Taxis/buses/personal delivery, etc.) • Only 10% (R1.9 billion) is captured by the formal sector (Banks & Post Office) Shoprite Domestic Money Transfers • Shoprite, in association with eCentric and Capitec Bank, launched the domestic in store remittances service in 2006 • By 2010, they manage to capture an estimated R10 billion of the market • Annual volume growth rates are exceeding 25%, despite growing competition • Service used by more than 10 million individuals

Lesotho remittances-the impact • Population is 2 million • 50% of the population have incomes below poverty line • 400 000 migrants from Lesotho living in SA • Total remittances from SA to Lesotho is R1.75bn • R1.4bn of the total remittances is remitted informally • Using formal channels the cost to remit money is 16.43% of the value remitted • If all remittances were formalised the cost would amount to R287 million • New remittance corridor cost is R9.99 per transaction up to a max of R5000 per transaction

Shoprite - Money Markets “Money Market” service stations offer a comprehensive range of financial services and products to the Group’s customers through dedicated in-store service counters: •utility bill payments • bus and airline tickets • basic insurance policies • tickets for major sporting and cultural events • travel packages • MONEY TRANSFERS Shoprite estimates more than 50% of its clients make use of the counter while in the store Installed 642 new service points to meet demand

Key issues to be addressed • In-country remittances scheduled for piloting in Swaziland (during 2015) Currently operational in Zambia ,RSA, Namibia and Lesotho • Cross Border remittances currently operational in Lesotho (March 2015) • Landscape of remittances is changing as a result of the new product (e.g. people depositing money before they get on a taxi to travel home at the end of a week’s work) • Need to motivate for increased lenience with respect to Exemption 17 • Cross Border remittance is currently limited to a remittance between RSA and another country (1 direction)-needs to allow for remittances between all countries in the region