Download

1 / 12

240 likes | 872 Views

Goodwill Impairment. Overview. O n September 15, the FASB issued ASU 2011-08, Testing Goodwill for Impairment Intent of the new standard is to reduce cost and complexity of annual goodwill impairment test

E N D

Overview • On September 15, the FASB issued ASU 2011-08, Testing Goodwill for Impairment • Intent of the new standard is to reduce cost and complexity of annual goodwill impairment test • Provides entities an option to perform a qualitative assessment to determine whether it is necessary to perform Step One of the annual Two-Step impairment test • Effective for fiscal years beginning after December 15, 2011 • Early adoption allowed

Overview, continued • Pronouncement does not change: • How goodwill is calculated • How goodwill is assigned to reporting units • The requirement to test goodwill annually • The requirement to test for goodwill impairment at interim periods if events and circumstances warrant • However, FASB acknowledged that it may later consider a longer-term project to evaluate goodwill accounting

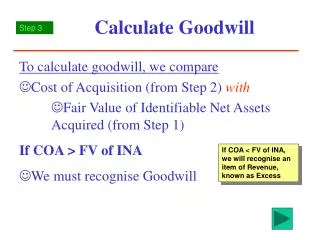

Current Impairment Test Step 1: • Determine whether the fair value of the reporting unit is less than its carrying amount, including goodwill. If so, proceed to step 2. • If the fair value of the reporting unit is greater than the carrying amount, further testing of goodwill for impairment is not performed.

Current Impairment Test, continued Step 2: • Determine the implied fair value of the goodwill of the reporting unit by assigning the fair value of the reporting unit used in step 1 to all the assets and liabilities of that reporting unit (including any unrecognized intangible assets) as if the reporting unit had been acquired in a business combination. • Compare the implied fair value of goodwill with the carrying amount of goodwill to determine whether goodwill is impaired.

Key Provisions of New Requirements • Entity has the option to first assess qualitative factors to determine whether or not it is necessary to perform the current two-step test. • Based on the qualitative assessment, if it is more-likely-than-not that the fair value of a reporting unit is less than its carrying value, quantitative impairment test is required • Otherwise, no further testing required

Key Provisions of New Requirements, cont. • Qualitative assessment can be performed on none, some or all reporting units – don’t have to follow same procedures for all reporting units • Decision can be based on specific facts and circumstances • For example, an entity may conclude that the qualitative assessment would be cost effective for certain reporting units but not others • Selection of reporting units on which qualitative assessment is performed is not an accounting policy choice that requires consistency between periods

Examples of Qualitative Factors to Consider • Macroeconomic conditions • Limits in accessing capital • Fluctuations in foreign exchange rates • Industry and market considerations • Deterioration in entity’s operating environment • Increased competitive environment • Change in the market for entity’s products or services • Regulatory or political developments

Examples, continued • Entity specific events • Declining financial performance • “Cushion” between the reporting unit’s fair value and carrying amount as determined in recent fair value calculations • Likely to be an important consideration • Cost factors (e.g., increases in raw materials, labor, etc.)that negatively impact earnings and cash flows • Changes in management, key personnel, strategy, or customers; contemplation of bankruptcy; or litigation • Decrease in share price (if applicable)

Implementation Considerations • Qualitative consideration may be more cost effective when fair value substantially exceeded reporting unit carrying value in prior period and no significant adverse changes have occurred • Likely less cost effective when a reporting unit’s fair value closely approximated its carrying amount in recent fair value calculations • Companies are required to give more weight to events and circumstances that most significantly impact a reporting unit’s fair value

Implementation Considerations, cont. • Effective for fiscal years beginning after Dec. 15, 2011 • Early adoption allowed • Companies can choose to early-adopt even if annual test date is before September 15, 2011 (date of issuance of new standard), as long as the company has not yet issued financial statements for the period that includes the test date. • Could provide a planning opportunity • Even though this is a qualitative measure, companies should consider documenting assessments with quantitative information (e.g., projections of financial results)

International Ramifications • Differences exist between U.S. GAAP and IFRS • Revised standard does not eliminate differences nor achieve convergence • IFRS requires annual quantitative goodwill impairment test to be performed at the level of a cash-generating-unit or a group of cash-generating-units.