Download

1 / 36

380 likes | 645 Views

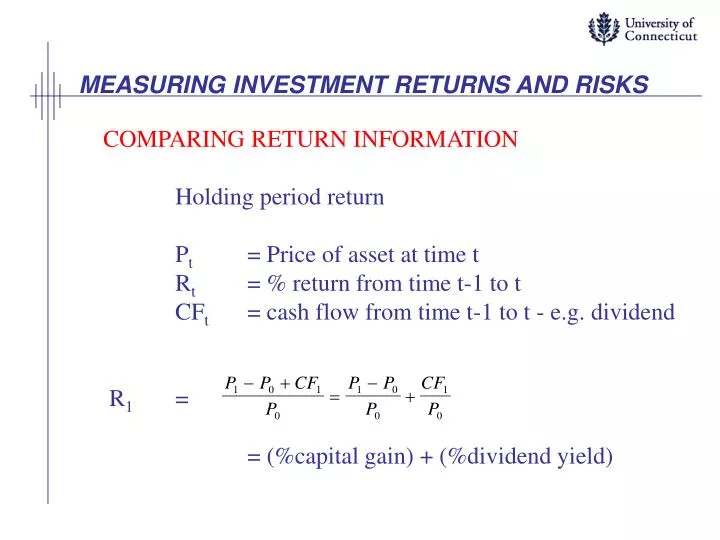

MEASURING INVESTMENT RETURNS AND RISKS. COMPARING RETURN INFORMATION Holding period return P t = Price of asset at time t R t = % return from time t-1 to t CF t = cash flow from time t-1 to t - e.g. dividend R 1 = = (%capital gain) + (%dividend yield).

E N D

MEASURING INVESTMENT RETURNS AND RISKS COMPARING RETURN INFORMATION Holding period return Pt = Price of asset at time t Rt = % return from time t-1 to t CFt = cash flow from time t-1 to t - e.g. dividend R1 = = (%capital gain) + (%dividend yield)

QUESTION: How can you measure the return you expect from an asset? The best guess at the future return i.e., what one should expect is the mean return: where Ri is an observation of the variable (return) and is the arithmetic sample mean of the variable (return)

EXAMPLE OF ARITHMETIC MEAN P0 = 100 - price now P1 = 200 - price at time 1 period from now R1 = (200 - 100)/100 = 1.00 or 100% Suppose P2 = 100 - period 2 price R2 = ((100 - 200)/200 = -.5 or -50% Arithmetic mean return = (R1 + R2 )/2 = .25 or 25%

QUESTION: Is an average return of 25% a good return? Is it accurate? ANSWER: Not for past returns. Instead use Geometric return (also called compound return) especially when returns are volatile. Geometric mean ≤ arithmetic mean. G = G = is the geometric mean return Ri = the return in period i Õ = the product operator The geometric mean using the previous data is: G = (1 + 1.0)1/2 x (1 + (-.5))1/2 - 1 = [(2)(.5)]1/2 - 1 = 0

Question: Who knows what this symbol means?Answer: This is the Chinese ideograph for Risk (or crisis). It is a combination of the ideograph for Danger (first symbol) and the ideograph for Opportunity (second one). Why are they together? Who likes taking risks? –playing card games – poker? Who wants to make millions of dollars?

RISK AVERSE INVESTORS REQUIRE MORE RETURN TO HOLD ASSETS WITH MORE RISK QUESTION: What is risk? ANSWER: The likelihood that you will not receive what you expect - i.e. the mean risk free you always get what you expect Variance and Standard Deviation - ivolatility.com sample variance = s2 = 2 /n sample standard deviation = s for s = 10% and = 10% -20% -10% 0 10% 20% 30% 40%

COEFFICIENT OF VARIATION (CV) CV = (Std. Dev. of return)/(mean return) = risk/ arithmetic expected return says, for each percent of mean return, how much volatility must you bear. PROBLEM: Suppose asset 1 has a standard deviation of .08 and a mean return of .06 while asset 2 has a standard deviation of .05 and a mean return of .03. Which is best? (Asset 1) CV1 = .08/.06 = 1.33 still has more total risk CV2 = .05/.03 = 1.67

Ibbotson Sinquifield Data – 1926-2009 Geometric Arithmetic Standard StocksMeanMeanDeviation Large Cos. 10.4 12.4 20.3 Small Cos. 12.7 17.5 33.1 Bonds Long Corp. 5.9 6.2 8.6 Long Treas. 5.4 5.8 9.3 Med. Treas. 5.4 5.5 5.7 Tbills 3.7 3.8 3.1 QUESTION: Compare the Risk/Return tradeoff of Bonds to stocks and T Bills to Bonds. -anything unusual here? ANSWER: Bonds have relatively low returns but large variation due to unexpected inflation

Expected Return and Variance Using Probability Distributions Probabilities are weights attached to scenarios or observation classes where i indexes scenarios. Expected return = E(R1) = S Probabilityi x Return1i Return Variance = s2(R1) = S Probabilityi x [Return1i - E(R1)]2 Sample mean and variance assumes that each observation has equal probability which is acceptable if the sample covers a full economic cycle. Return standard deviation = s(R1) = [s2(R1)]1/2

How to Get Probabilities You can get some probabilities from past data. If stocks earned 10% in 30 years over the last 100 years, then the probability of earning 10% is .30. But this approach uses past data which may not reflect expected future events. Another approach is to use data from websites like intrade.com that offer bets on events for prices that reflect the probability that the event will occur. Price = probability1(payoff1) + probability2(payoff2) = probability1(1) + probability2(0) Price = probability1

EXPECTED RETURN, VARIANCE, AND COVARIANCE OF A PORTFOLIO USING JOINT PROBABILITY DISTRIBUTION Assume portfolio consisting of stock 1 and stock 2: Expected portfolio return = E(Rp) = Weight1 x E(R1) + Weight2 x E(R2) Portfolio Variance = sp2 =Weight12 x s2(R1) + Weight22 x s2(R2) + 2 x Weight1 x Weight2 x s(R1, R2) where s(R1, R2) = covariance of stock 1 and stock 2 returns.

NO COST TO DIVERSIFY Diversifiable risk can be eliminated easily so - no compensation. Only undiversified risk should receive compensation - Covij risk where Covariance = s(R1, R2) = S Probabilityi x [Return1i - E(R1)][Return2i - E(R2)] In a portfolio, there is a covariance for each asset pairing – the many covariances account for most of a portfolio’s variance. All else equal, covariance is large when the data points fall along the regression line instead of away from it because, on the line, the deviations from the means of each variable are equal – the products are squares - larger than otherwise.

Illustrate surprising probabilities with student birthdays. Question: What is the probability that two students in class have the same birthday? Individual pairings have small probability but there are many pairings. It’s usually best to diversify, except in this case.

Example: Bill Gates started with $100 billion in Microsoft - now sells $50 million each month and buys other stocks. QUESTION: Consider two stocks with the following return distributions. Find the variance for a portfolio with 40% invested in stock 1 and 60% invested in stock 2. Obama Liberal Conservative Moderate Probability .50 .10 .40 stock 1 return .10 .15 .20 stock 2 return .25 .10 .05

Portfolio Return Distribution Example: Probability Distribution Results E(R1) = .50(.10) + .40(.20) + .10(.15) = .145 E(R2) = .50(.25) + .40(.05) + .10(.10) = .155 s2(R1) = .50(.10 - .145)2 + .40(.20 - .145)2 + .10(.15 - .145)2 = .0022375 s2(R2) = .50(.25 - .155)2 + .40(.05 - .155)2 + .10(.10 - .155)2 = .009235 s(R1, R2) = .50(.10 - .145)(.25 - .155) + .40(.20 - .145) (.05 - .155) + .10(.15 - .145)(.10 - .155) = -.004476

correlation = s(R1, R2)/s(R1) s(R2) = -.004475/[(.0473022)(.0960989)] = -.98 E(Portfolio return) = .4(.145) + .6(.155) = .151 Portfolio Variance = (.4)2 (.0022375) + (.6)2 (.009235) + 2(.4)(.6)(-.004475) = .0015346 QUESTION: Suppose Obama chose Chris Dodd as Treasury Secretary instead of New York Fed President Timothy Geithner. How would you restructure the portfolio? - more of stock 2 and less of stock 1.

Illustrate correlation and optimal portfolio weights using www.wolframalpha.com (click “Examples”, then Money and Finance” then under “compare several stocks” put in up to 4 stock ticker symbols) Explain the optimal portfolio return and volatility. For more complex portfolio optimization statistics and to input more than 4 stocks go to Macroaxis.com, register for free and create a portfolio – then try the “management” option and try “optimize” or “suggest”.

CORRELATION AND HEDGING - FIRE INSURANCE Correlation - in general - hedging takes advantage of negative correlation but less than perfect correlation can be used to reduce risk. EXAMPLE Suppose you own a $200,000 house. QUESTION: If the probability of fire = .001 and the cost of a fire insurance policy is $700, what is your expected return on the insurance policy alone. Is it risky? Is insurance a good investment?

Probability Outcome % Return Fire.001 200,000-700 199,300/700= 28471% No fire .999 -700 -700 / 700 = -100% Expected return and variance of policy on its own (like Walmart buys life insurance policies on its employees). E(R) = .001(28471) + .999(-100) = -71.43% s2 = .001( 284.71 - (-0.7143))2 + .999( -1 - (-0.7143))2 = 81.46 + .0815 = 81.54 = 8154%

Expected return on house without insurance = [.999 (0) + .001 (-1.00)] = -.001 = -.1% Variance of return on house without insurance = [.999 (0 - (-.001))2 + .001 (-1.00 - (-.001))2] = .0001 Expected return with insurance = [ .001 (-700/200,700) + .999 (- 700/200,700)] = 1.00 (- 700/200,700) = -.0035 = -.35%

Variance of return with insurance = [.001 [(- 700/200,700) - (-.0035)]2 + .999 [(-700/200,700) - (-.0035)]2 = 1.00 (0) = 0% Insurance doesn't look like a good investment but return variance is zero with insurance, hence insurance is valuable for hedging or risk reduction purposes. Question: Many stores offer insurance or service contracts on items such as DVD players to cover costs after warranties run out. Why is this coverage typically an even poorer investment than home or automobile coverage?

Beta is a Standardized Covariance Beta is the slope of a regression line of an asset’s returns on the market portfolio’s return. Beta1 = = where m signifies market and 1 signifies stock 1. All asset betas are measured against the market so all are being compared with the same gauge. If B1 = 1 and B2 =.5, stock 1 is twice as risky as stock 2

CAPM - Capital Asset Pricing Model Beta is used as a measure of risk in a theoretical return equation called CAPM. E(Ri) = Rf + Bi[E(Rm) - Rf] where E(Ri) = expected return on stock i Rf = the risk-free rate of return Bi = stock i’s beta E(Rm) = expected return on the market portfolio

Illustrate diversification with stockcharts.com – carpets Holding a diversified portfolio is best unless you have better estimates of payoff probabilities for a stock than the market.

Illustrate beta and return distributions using www.wolframalpha.com (click “Examples”, then Money and Finance” then under Stock Data put in a company)