Download

1 / 22

220 likes | 327 Views

PERFORMANCE BUDGETING IN THAILAND GEOFF DIXON FORMER CONSULTANT, THAI BUREAU OF THE BUDGET. Thai budgeting has been very centralized. very detailed budget categories. cash allotments within each budget year. pre-audit of spending transactions (soft). This results in

E N D

PERFORMANCE BUDGETING IN THAILAND GEOFF DIXON FORMER CONSULTANT, THAI BUREAU OF THE BUDGET

Thai budgeting has been very centralized • very detailed budget categories • cash allotments within each budget year • pre-audit of spending transactions (soft)

This results in • strong control of the budget bottom line but • weak control of budget composition and efficiency

The challenge is to improve the TRADE-OFF between • macro fiscal control, and • compositional and operational efficiency How? By introducing performance budgeting

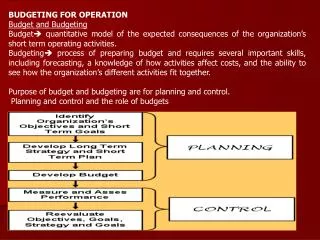

PERFORMANCE BUDGETING MEANS 1. Output driven budgeting • identifying agency outputs • costing those outputs • basing budget allocations on this information In the Thai case this meant identifying and costing output classes

PERFORMANCE BUDGETING MEANS 2. Empowering program agencies to manage • internalizing control of inputs • providing a predictable funding environment In the Thai case this meant broader budget categories & MTEF

PERFORMANCE BUDGETING MEANS 3. Replacing external control over inputs with external control over outputs • reporting budget-year outputs against budget preparation assumptions • introducing broader performance indicators for policy management In the Thai case this meant sector experts helping develop performance indicators

Input control Output control External control Internal control

Internal versus external control (agency autonomy) New Zealand Aust pre ’90s Thailand Cambodia Output versus input control (performance focus)

Transitioning to performance budgeting 1. How to manage change in program agencies?

The chicken/egg problem in moving program agencies from external to internal control • agency skills are in obtaining resources rather than internally allocating them • the Budget Bureau argues that reducing its controls is therefore dangerous The result: HIATUS

The 7 hurdles attempted to break the impasse by making BOB concessions to an agency conditional on hurdle standards in 7 areas • ¨budget planning • ¨output costing • ¨procurement management • ¨budget/funds control • ¨financial and performance reporting • ¨asset management • ¨internal audit

The reform process is formalized for each of six pilot agencies by • a memorandum of understanding with BOB at the start of the reform process • a resource agreement with BOB when the seven hurdles are met

Transitioning to performance budgeting 2. How to manage change in the budget agency?

The focus of BOB control should shift FROM • whether actual spending is consistent with very detailed pre-specified categories and conditions TO • whether agencies’ use of budget funds in a freer operating environment is effective

The challenge for the Bureau of the Budget • refocus from agency control to agency analysis • refocus from amounts of inputs to amounts of outputs and input- output links

The Bureau of the Budget must change from • an enforcer of rules to • an evaluator of performance It is already familiar with this role in budget preparation The role will need to extend through to budget execution

Transitioning to performance budgeting 3. Is the hurdle approach ‘migratable’?

There are two approaches to managing budget reform in change resistant environments • sequence the STAGES OF REFORM - output identification/perf. indicators/devolution /MTEF • sequence the AGENCIES TO BE REFORMED, with multi-stage package for each agency upon meeting hurdle standards The Thais adopted the second approach

This reflected the Budget Bureau’s difficulty in quickly providing technical leadership • spearhead for reform was six reform focused agencies • each had an integrated package of reform • budgetary freedoms would be granted by BOB conditional on meeting 7 hurdles

The hurdle approach is well suited to Thailand • progress is possible in program agencies even though progress is slow in BOB • hurdle approach is failsafe for BOB and more likely to win its acceptance • there is a stronger incentive package for individual agencies to reform due to hurdle conditionality • it provides an integrating framework for different reforms required in budget and program agencies

In countries in which the budget bureau itself has achieved critical reform momentum the alternative of • sequencing by reform stages (each stage simultaneously introduced across all agencies) rather than • reform agencies (each of which is offered a multi-stage reform package when hurdles are met) • should be considered