Download

1 / 23

240 likes | 547 Views

Purchasing Power Parity. A Survey on East European Countries (1995-2001). Ioana Ceanga. The Theory of Purchasing Power Parity. arbitrage across goods markets Law of One Price (LoOP). absolute PPP:. The Theory of Purchasing Power Parity. - absolute form of PPP in logarithm.

E N D

Purchasing Power Parity A Survey on East European Countries (1995-2001) Ioana Ceanga

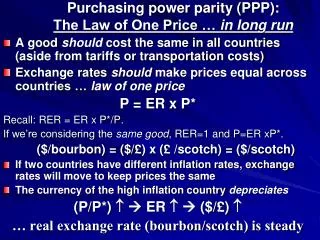

The Theory of Purchasing Power Parity • arbitrage across goods markets • Law of One Price (LoOP) absolute PPP:

The Theory of Purchasing Power Parity - absolute form of PPP in logarithm • semi-strong form of PPP - relative form of PPP - the weak form of PPP

The Theory of Purchasing Power Parity - Absolute PPP cannot be taken as instantaneous equality – it is a guide to long-run behavior of exchange rate • real exchange rate q = s + p* - p

The Theory of Purchasing Power Parity • If PPP is to hold in the long-run, the real exchange rate should be stationary • One way to test the stationarity of it is to find a cointegration relationship between the nominal exchange rate and the prices • Cointegration framework

• Data and methods • bilateral exchange rates (ROL/USD, CZK/USD, PLZ/USD, HUF/USD) monthly average • consumer price indexes (Romania, Czech Republic, Poland, Hungary) set to 100 in December 1994 • consumer price index for United States set to 100 in December 1994 Covered period: 1995:01-2001:12 (72 observations)

• Data and methods • unit root tests for determining the order of integration • Johansen test for establishing if there are cointegration relationships in case of the absolute and semi-strong forms of PPP • Ordinary Least Squares Method and Wald test in case of the relative form of PPP

• Testing the strong form of PPP • testing the existence of long-run relationships between nominal exchange rates and consumer price indexes using the cointegration techniques • verifying the size of the CPI’s coefficients

• Testing for ROL/USD exchange rate Results: 5 lags in differences included speed of adjustments coefficients: (-0.291 0.045 0.006)

• Testing for CZK/USD exchange rate Results: 1 lag in differences included speed of adjustments coefficients: (-0.007 0.009 0.004)

• Testing for PLZ/USD exchange rate Results: 7 lags in differences included speed of adjustments coefficients: (-0.040 0.061 0.003)

• Testing for HUF/USD exchange rate Results: 9 lags in differences included speed of adjustments coefficients: (-0.237 -0.050 0.00008)

• Testing the semi-strong form of PPP Why should the assumptions of PPP be relaxed? • Different weights in the construction of price indexes • The price index comprises both tradables and non-tradables • Measurement errors • Transportation costs • Non-homogeneity of goods, tariff barriers where

• Testing for ROL/USD exchange rate Results: 3 lags in differences included Trace test indicates no cointegration at both 5% and 1% levels

• Testing for CZK/USD exchange rate Results: 1 lag in differences included The null of no cointegration cannot be rejected

• Testing for PLZ/USD exchange rate Results: 6 lags in differences included speed of adjustments coefficients: (0.014 0.073)

• Testing for HUF/USD exchange rate Results: 7 lags in differences included speed of adjustments coefficients: (-0.005 0.037)

• Testing the relative form of PPP - states that the proportionate change in the exchange rate is a function of the difference in the proportionate changes in home and foreign prices - implies an OLS estimation for the equation: - applying Wald test in order to check if the coefficients estimated can be 1 or -1

• Testing for ROL/USD exchange rate Wald test null hypothesis: c(1)=1, c(2)=-1 F-statistic 2.934718 Probability 0.059117 Chi-square 5.869436 Probability 0.053146

• Testing for CZK/USD exchange rate Wald test null hypothesis: c(1)=1, c(2)=-1 F-statistic 60.35474 Probability 0.000000 Chi-square 120.7095 Probability 0.000000

• Testing for PLZ/USD exchange rate Wald test null hypothesis: c(1)=1, c(2)=-1 F-statistic 8.293522 Probability 0.000542 Chi-square 16.58704 Probability 0.000250

• Testing for HUF/USD exchange rate Wald test null hypothesis: c(1)=1, c(2)=-1 F-statistic 1.958467 Probability 0.147780 Chi-square 3.916934 Probability 0.141075

• Conclusions PPP theory in all the forms studied does not hold - the assumption of no transaction costs is unrealistic - the lack of commercial barriers is not found in real life - the intervention of central banks - the costs of non-traded goods - imperfect information - the participation of other traders in the FOREX market