Download

1 / 13

130 likes | 229 Views

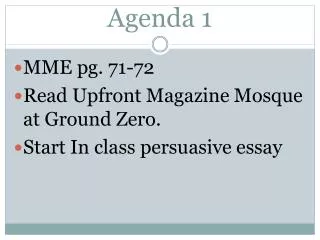

BA 128A-1 Agenda 2/8. Questions from lecture Review Assignment - I3-36,47,57 I4-27,28,56 Additional Problems - I4-10,13,24,34,51 Web Page - www.haas.berkeley.edu/Courses/Spring1999/BA128A-1/index.html. Items that are not income. Unrealized income e.g. stock appreciation Self-help income

E N D

BA 128A-1 Agenda 2/8 • Questions from lecture • Review • Assignment - I3-36,47,57 I4-27,28,56 • Additional Problems - I4-10,13,24,34,51 • Web Page - www.haas.berkeley.edu/Courses/Spring1999/BA128A-1/index.html

Items that are not income • Unrealized income e.g. stock appreciation • Self-help income • Rental value of personal-use property • Gross selling price of property

Statutory exclusions • Gifts and Inheritances • Life insurance proceeds/ Death Benefits • Adoption expenses - from qualified assistance programs • Scholarships • Payments of injuries and sickness • Foreign earned income • Forgiven Debt • Employee Fringe Benefits

Gifts and Inheritances • Generally excluded • Income produced by the gift afterwards is taxable • Prize and awards are inclusive • To determine whether it is a gift or not, motivation is the key: love, affection, sympathy, generosity

Awards • Prizes and awards - generally taxable • Exceptions: charitable, religious, scientific achievements • Scholarships - excludable for tuition, fees, books, supplies and equipment. Include if its room and board, laundry and work study

Life insurance proceeds • Generally excluded • Amount received > face value of policy is taxable as interest • Exchange/selling of policy is taxable to the extent of the excess amount of cash received over premiums paid • Dividends from life insurance policy are excluded (return on capital) • Accelerated death benefits are excluded

Adoption expenses • Generally use as tax credit • Exclusions of up to $5000 from a qualified employer adoption assistance plan • Subject to phase out • Adoption expenses include adoption fees, court fees and attorney fees

Compensation for injury and sicknesses • Payments are generally excluded if policy is purchased by the taxpayer • Cannot deduct premiums if paid by the taxpayer • Include both physical and emotional distress • Punitive damages are taxable • Payments of loss income under accident and health insurance policy are excludable

Other exclusions • Foreign earned income • $72,000 exclusion • a resident of a foreign country or present in a foreign country for 330 days • additional exclusion related to housing costs • Forgiven debt • generally taxable • exceptions: bankruptcy, insolvency and student loan • insolvency, NOL basis is reduced

Employee fringe benefits • Premiums paid by employers for health, accident and disability insurance are deductible and excluded from employees’ gross income • Group term life insurance - up to $50,000 premium exclusion. Key employees are subject to more restrictions P I4-11 • Benefits from medical and life insurance are excluded from employees’ gross income but benefits from disability insurance are taxable • Self employed individual may deduct 45% of medical insurance premiums as business expenses

Other fringe benefits • Excludable if it is ordinary and necessary • Provides no-additional-cost benefits • Qualified employee discounts • Athletic facilities • De minimis benefits • Transportaton/Parking fringes • Membership fees in professional organization

Other employee fringe benefits • Employee awards - de minimis rule, not disguised compensation, no discrimination. • Individual employee awards can be up to $1,600 • Meals and lodging - deductible if furnished at employer’s premise • De minimis rule applies e.g. overtime meals excluded • Meal allowances are taxable • Meals and entertainment that are not reimbursed - can deduct 50%

Other employee fringe benefits • Employee death benefits - depends on intention of transferor (gift or compensation of past services) • Dependent care by employer - $5000 excluded for married couples • Educational assistance by employer- up to $5250 excluded • Cafeteria plans - choice of cash/statutory nontaxable fringe benefits • Cash is taxable • some statutory nontaxable fringe benefits in lieu of wage reduction of supplement wages • non discriminatory