Download

1 / 86

880 likes | 1.12k Views

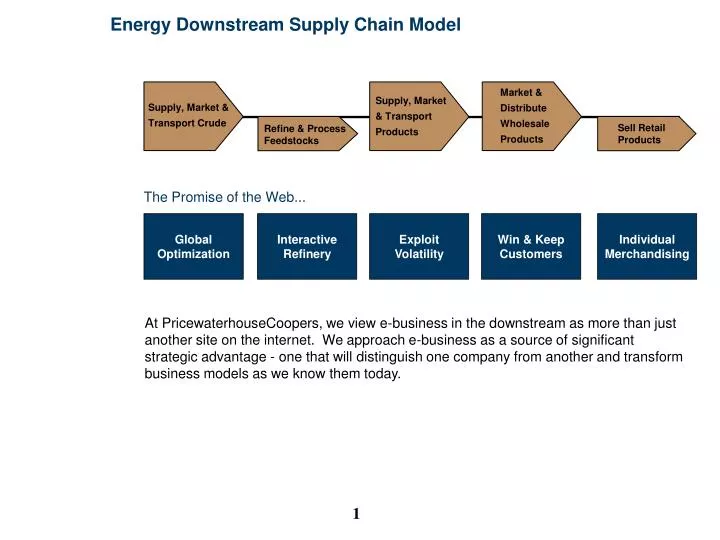

Global Optimization. Interactive Refinery. Exploit Volatility. Win & Keep Customers. Individual Merchandising. Energy Downstream Supply Chain Model. Market & Distribute Wholesale Products. Supply, Market & Transport Products. Supply, Market & Transport Crude. Sell Retail

E N D

Global Optimization Interactive Refinery Exploit Volatility Win & Keep Customers Individual Merchandising Energy Downstream Supply Chain Model Market & Distribute Wholesale Products Supply, Market & Transport Products Supply, Market & Transport Crude Sell Retail Products Refine & Process Feedstocks The Promise of the Web... At PricewaterhouseCoopers, we view e-business in the downstream as more than just another site on the internet. We approach e-business as a source of significant strategic advantage - one that will distinguish one company from another and transform business models as we know them today.

Exciting Future for Downstream Oil E-Business Global connectivity is the most "disruptive" technology to hit industry • It can enable a thoroughness in decision process and enrichment in staff never before available • Many tools & techniques available; no single solution dominant • Globality and dynamics of downstream make it a strong candidate to achieve dividends • Downstream behind other industries and there are lessons to be learned • New operating models must be driven by defensible business value improvement principles

E-Business is “In the Money” The www.pwcmoneytree.com survey tracks investments in USA by venture capitalists • Internet investments increased six-fold from $3.4 billion in 1998 to $19.9 billion in 1999 • B2C still captured largest share with $4.5 billion • B2B increased 908% over 1998 • Infrastructure companies rose 547% over 1998 “Shattering previous annual record by 150%, venture capital investment in US reached a new high of $35.6 billion in 1999.”

Six Forces Shaping the Future of Business European convergence required development of unique insights Corporate management is finding: • In converging industries, the customer rules • E-Business is business • Success in the knowledge economy requires new thinking • There is a revolution in corporate reporting • The battle for top talent will increase The sixth force is European convergence...

Elements of the Downstream Our subject is the entire downstream hydrocarbon supply chain Crude Acquisition and Transportation Bulk Distribution Refining MARKETING Final Distribution Terminals & Wholesalers Retailing RISK MANAGEMENT

Questions to be Answered for the Downstream E-Business is here and growing daily. Given all the options: • How will it affect my company? • What should we be doing now, next month and in 12 months? • What are the value creation leverage points? • How do we get started?

Working the Web How companies use E-Business to boost productivity Data: Companies; Business Week

Benefits of E-Business must be Value Driven Value creation focus needed for successful E-Business initiatives Although E-Business can create multiple opportunities, a strong business focus is needed to maximize value Improved customer service Focus on Value Drivers Reduced costs/ overhead Newrevenue streams Higher returns on investment

1 2 3 4 5 6 Low Med High Benefits of E-Business E-Business is impacting areas that CEOs are most concerned about 80.0 70.0 60.0 Building customer loyalty 50.0 Achieving market leadership Percent responding 40.0 30.0 Streamlining business processes 20.0 Creating new products/services 10.0 Managing “risk and compliance” 0.0 Reaching new markets Diminish Risk Enhance our Reputation Segment Markets Finely Enhance Brand Recogition Match Competitive Moves Increase Customer Loyalty Achieve/maintain Leadership Reduce Infrastructure Costs Offer Differentiated Products Reach New Markets Quickly Lower Customer Service Costs Assure Regulatory Compliance Increase Information's Impact Source: PricewaterhouseCoopers Research, 1998

E-Business is about Speed E-Business is expanding at phenomenal rates Maturity 40 40 35 Mass market 30 Infrastructure development (next generation) 25 20 Take up years (50 m users) Adoption % of Population Product / service innovation and initiation Experimenters/ pioneer 15 15 10 5 Early adapters 4 0 Radio PCs Internet 1980 1990 2000 2010 2020 Time

B2B will significantly outpace Business to Consumer (B2C) commerce in the next several years Energy Industry Behind Others Other industries can provide lessons learned to the downstream

B2C Examples Provide Some Insight Technology leadership came from B2C innovators Convergence IndustryTransformation Degree of change to business model Value ChainIntegration Channel Enhancement Enabler Transformer Role of E-Business

Channel Enhancement Industry Transformation Convergence Secure Transaction Processing Online Catalogs Publishing Web Sites Integrated Industries e-Business Portals Transparent Integration Industry Consortiums Cybersourcing Industry Reengineering Virtual Organizations Value Chain Integration Disintermediation Reintermediation Value Chain Integration Business Process Outsourcing Four Box E-Business Development Model Every stage requires new organizational structure

E-Business Development Organizations evolve through four stages: Channel Enhancement involves the development of an electronic presence or web site, which presents information about the company, its products, and its key differenti- ators. In the business-to-business world, this is typically the use of electronic channels such as EDI to suppliers and key partners. The goal is to improve timeliness, cost effectiveness, and reach. Integration brings closer interaction as customers and suppliers work together on-line and as vendors customize content for their users. Exchange of critical information brings greater understanding and can offer significant competitive advantages. Tax, legal, risk management, and internal control & compliance issues loom larger as real business transactions take place. Convergence allows companies to achieve true integration with other organizations both within and outside their own industries. Over time, cross-country supply chains will come together to create networked organiza- tions and markets. New forms such as dynamic customer-centered networks may exist for only a single contract, a single customer, or a single instant. Transformation begins as executives distinguish between their core and non-core competencies. E-Business allows them to more easily unbundle operations, retaining only those critical to market position. With transformation comes challenges involving organization, staff, training and retention.

Channel Enhancement - Downstream Oil New possibilities are just being discovered • Check vessel status and characteristics to support nomination process for crude & product supply • Check and query order status • Allow distributors to view price/volume data for shipment and orders prior to dispatch • Post (real time) wholesale prices • Web-based exchange and throughput balances available to counter parties • Enable viewing of retail site dispatch status • Provide web-based MSDS sheets, tax and environmental documents to customers and distributors

A virtual market place channel, e-Chemicals has 20 major chemical suppliers, 1000 products and over 500 customers, and alliances with IBM, Suntrust and Yellow Services Another virtual market place channel, Chemdex offers laboratory chemicals and recently announced it will handle $85M as a third party source for VWR Scientific Products Chemical Industry Innovations New entrants have entered the marketplace

Channel Enhancement - Summary Channel Enhancement often entails basic website development primarily with customers and some supplier interfaces E-Commerce Steps to Achieve Description Impact on Value Drivers Channel Enhancement • Publishing Websites • Online Catalogs • Online Processing • Secure Transactions • The initial website will provide basic corporate information to customers, investors, etc. • Online catalogs are provided by suppliers. • Selected suppliers will begin to provide online processing of orders. Selected customers are able to track place and track orders online via customized extranet which are linked to the company. • All transactions are intrinsically secured. Revenue growth through: • Enhanced visibility in the market place. • Opportunity to reach new customers. • Customers value convenience of ordering products online. Reduction in costs through: • More automated supply acquisition will reduce the total cost of acquisition. • Streamlined processes will allow customer service staff to direct attention to higher value added activities.

Enhanced customer services via the web Order entry and queries Changing orders on-line On-line inventory optimization Provide customers with available-to-promise (ATP) data at entry of order Allowing customer and supplier to check stocks and inventories on-line for fast replenishments Real time matching of supply and demand via the web Integrating production, inventory, quality and other information between refineries and chemical plants Matching risk services with commodity trades Value Chain Integration - Downstream Oil New possibilities are being discovered

Value Chain Integration - Supply Chain Model Collaborative planning and forecasting is the heart of an integrated supply chain SUPPLIERS WHOLESALE CUSTOMERS PLANNING & FORECASTING PLANNING & FORECASTING PLANNING & FORECASTING REFINER RAW MATERIALS FINISHED GOODS

Strategic Supplier Strategic Supplier Value Chain Integration - Supply Chain Model Real-time collaboration now possible with external partners • Will procure materials in anticipation of customer needs • Obtain materials on a just in time basis • Will monitor costs more effectively • Allows customer to anticipate finished goods delivery • Logistics Partner uses GPS • for real time tracking of orders • Customer ERP can directly interface to automate the order cycle • Tied directly to the customer’s own demand based planning system • Real time telemetry will trackorder throughout manufacturing cycle • Manufacturing planning based on accurate anticipated demand Customer Order Cycle Procurement Cycle Replenishment Cycle Manufacturing Cycle • Visibility of Exchanges and Swaps • Internet enabled communication allows supplier to see status of finished goods inventory • Accurately monitor vendor performance • Can more easily implement vendor managed inventory • Implement a more accurate demand based procurement plan • Strategic supplier can see real time status of customer orders • Accumulated customer order history helpsstrategic supplier anticipate demand for inputs • Supplier can communicate directly with customer as needed • Telemetry allows for more accuratematerials need tracking • Integration with ERP to anticipate and automatically procure materials

Value Chain Integration - Summary Seamlessly connecting customers & suppliers forms a truly optimized value chain E-Business Steps to Achieve Description Impact on Value Drivers • Value Chain Performance Assessment • Value Chain Strategy • Value Chain Optimization and Integration • Initial Interfaces between Strategic Partners IT Systems • A comprehensive value chain analysis is performed. The focus is on value creation. • The value chain strategy is revisited as a result of analysis. Strategic partners are identified. • The e-business enabled value chain will integrate suppliers and customers to the core organization via custom designed Websites. Business processes are redesigned in order to optimize activities in the value chain. • Initial steps are taken to interface with strategic partner systems. The changes in the role of suppliers and distributors will result in the disintermediation and reintermediation of value chain participants. Revenue growth through: • Ability to reach new customers will be enhanced. • Availability of accurate market information will enable quicker response to market changes. Reduction in Working Capital: • Integration of the value chain will enable collaborative demand based planning resulting in inventory reductions and reduced cycle times. • E-enabled communication will expand strategic suppliers in Vendor Managed Inventory (VMI) programs. Reduction in Capital Expenditure: • Inventory is utilized more effectively and therefore capital employed investment is reduced. Value Chain Integration

Industry Transformation - Downstream Oil New possibilities are being discovered • Honeywell proposing remote diagnosis of asset problems • Could control loops across geographies be next • Wide bandwidth allows global movement of drawings • Can oil companies outsource technical functions • AspenTech announces ProcessCity.com portal • Process models & design tools • Focused discussion groups • BPGAS UK bundling risk services with gas purchases • Enron providing risk managed gas & power contracts • Evans systems, a USA midwest C-Store operator: • Purchased I-Net holdings & sold the c-stores • Providing web marketing & sourcing to c-store industry

Industry Transformation - Downstream Downstream may fragment into value networks, with little vertical integration Retail Management Refining Specialists Design & Engineering Teams Wholesale Transportation Brokers Crude & Product Traders Logistics Providers Source: MIT “Inventing the Organization of the 21st Century”

Industry Transformation - Summary As they transform, companies link with strategic business partners to form virtual organizations E-Business Communities Steps to Achieve Description Impact on Value Drivers Integrated Value Chain Extension • Consolidation and review of strategic partnerships • Integration of partners systems • Creation of a virtual organization • Each partner has a clear vision of its core competencies. The processes and capabilities needed to participate in the virtual organization are well defined. • Partners systems are integrated reducing significantly manual interventions. • The organization has evolved to the point where new strategic members, not necessarily linearly related in the value chain, can be integrated relatively quickly. Revenue growth through: • New product and market opportunities can be exploited more quickly by using the combined resources of the virtual organization. Reduction in Working Capital: • Further reduction in inventory levels. • Enhanced communication capabilities will make it possible to outsource non-core activities. Reduction in Capital Expenditure: • Capital budgeting will be done across part or all of the virtual organization. This will result in greater collaborative usage of capital.

Convergence Evolution The picture becomes opaque as companies move toward convergence, but the steps are clear on how to prepare • Core competencies expand beyond traditional business • Leverage the brand Convergence • Corp boundaries extended, info shared • Non-core competencies are outsourced IndustryTransformation Degree of change to business model • All counter-party business conducted electronically • Boundaries breakdown, info shared across companies Value ChainIntegration • Internal teams expand to external partners • Some counter-party business conducted electronically Channel Enhancement Enabler Transformer Timing of E-Business Acceptance

Convergence - Examples Convergence already exists outside the oil world, especially in Europe British Gas insurance Electricity companies look at Internet access via wall sockets Citigroup, many others Electricity Gas Psion + Nokia, Ericsson Information Technology Insurance Telecomms Entertain-ment Retail Banking Broad- casting Consumer Goods Sainsbury, Barclay Square Loblaw British Telecom +BSkyB=BIB Disney Stores, Rainforest Café Character merchandising Consumer Direct

Convergence Possibilities The oil industry, like others, is restructuring to capitalize on its brand value Business to Consumer (B2C) • Shell Oil UK becomes an ISP • Pipeline companies becomes a voice and data transmission experts - Williams • Utility companies enhancing direct connections to household consumers Business to Business (B2B) • Risk management provided with energy commodity deals - Enron/Owens Corning • PGE outsourcing power supply to ARCO & UDS • Trading skill set extended to “bandwidth trading” - Enron & Williams

Downstream Oil - Convergence Example A new world example: service stations that offer a complete convenience service to the traveler Insurance Food Co. Bank GPS Locator Traffic Info Home Security Hotels Automobile Club Network Services Grocery Store Leisure Co. Travel Agents Distribution Co. Service Station Airlines Oil Co.’s Non-Fuels Repairs Car Rental Oil Co.’s Manufacturing Oil Co.’s Fuels Consumer

Convergence - New Business Model Communities will become powerful catalysts for change The New York Times “All the news that’s fit to print” Carmakers to Buy Parts on Internet by Keith Bradsher 02/26/00 General Motors, Ford and DaimlerChrysler announced today that they would set up the world’s biggest online marketplace for the auto industry’s private use, a giant auction site like eBay through which they plan to buy the nearly $250 billion worth of automotive components.

Downstream Outline Our downstream discussion is organized by supply chain components Relate top industry issues to: • Trade Crude • Refine • Trade Products • Market Wholesale • Sell Retail Trade Crude Trade Product Market Wholesale Sell Retail Refine Each sections is organized as follows: • Theme & key processes • Critical success factors (CSFs) • E-business vision theme and business issues • Web site catalog (industry and non-industry) • Value added by global E-Business approach • Sample problem definition

Five Forces Facing the Downstream Based on input from top executives at the CERA 2000 conference in Houston • Global market liberalization • Continued margin pressure across the chain • Re-balancing of refining-marketing by majors • Growing importance of trading competency • Size no guarantee of competitiveness Trade Crude Trade Product Market Wholesale Sell Retail Refine

Trade Crude - Processes and CSFs This section describes the characteristics of a “global optimization process” Trade Crude Trade Products Market Wholesale Sell Retail Refine Processes • Forecast demand & supply • Crude selection & optimization • Make & document deals • Arrange transportation • Manage risk/exposure/position • Settle and analyze deals CSFs • Strong relationships with producers • Instantaneous global access to price and changing market conditions • Accurate assays especially for swing purchases • Powerful price and market analytics capability • Accurate position system-wide, paper and physical

Trade Crude - Theme and Key Issues In optimizing globally, the following needs to be considered: Key issues in “Global Optimization”: • Large cargo market, few transactions, few sellers • Power shifted to producers • Managing price volatility • Transportation cost important, controllable component • Lack of crude quality transparency • Evaluation of open vs. flexible crude slate options • Understanding margin drivers & required synergies • Current business decision model process very slow

Trade Crude - Web Value Added Enhance competitive edge through collaboration and reduced decision time Web allows traders to: • Integrate-optimize selection & cargo movement • Respond more rapidly to global conditions • Identify & manage selective quality premiums Websites • RedMeteor.com • Enrononline.com • Altra.com • JPMorgan - Cygnifi.com • BPUK: E-Energy trading site • GoCargo.com

Trade Crude - Industry E-Business Examples There are numerous examples of new trading channels developing: • www.RedMeteor.com - designed with the idea of offering the energy buyer/seller one neutral place to gather information, analyze and then execute a split-second trade, authorized users will initially transact crude oil, electricity, natural gas, and natural gas liquids. The capability is there to trade physical, financial and option products, RedMeteor offers the ability to customize a personal homepage. • Enron Online - (www.enrononline.com) enables companies to buy and sell the full range of wholesale energy products & services on the web. The site also provides free of charge access to hundreds of commodity prices across the globe. Paper instruments will be added this year. • Altra - (www.Altra.com) provides registered users a real-time, on-line exchange for trading natural gas, electricity and liquid fuels. For gas, Altra provides limited clearing services for anonymous buyers and sellers. Altra is counterparty to the trades. To limit exposure, Altra uses credit and forward exposure limits for its customers. Users have the ability to view: Live Chalkboard activity, Pricing Summary, Completed NGL Transactions and Completed Crude Transactions.

Trade Crude - E-Business Examples There are other examples of how far it can go: • BP Amoco launched an internet-based gas trading service in an effort to assist its UK business customers in managing their gas portfolios more efficiently. The service, called "e-EnergyTrade," is available to all existing customers contracted to buy gas on a risk-managed basis. The service allows customers to buy/sell physical quantities of gas in accordance with their contractual arrangements. • JPMorgan - announced plans to launch an online derivatives service company called Cygnifi (www.cygnifi.com) to be complete by the end of Q1 2000. • GoCargo.com - (www.gocargo.com) is a neutral exchange manager between shippers and qualified transportation service providers. They provide a solution for buying and selling container shipping services. Similar initiatives are underway in crude & products tonnage.

Processes Plan and select feedstocks, production forecasting Schedule feedstocks, products, units Operate to plans & schedules Enhance operational reliability & safety Blend, store and ship on-spec products Adjust for variations and measure performance Refine - Processes and CSFs Characteristics of an “interactive refinery” Trade Crude Trade Products Market Wholesale Sell Retail Refine CSFs • Maximize variable margin • Optimal economic utilization • Minimize give-away and energy usage • Maximize controller utilization and improve unit reliability • Meet or exceed SHE requirements

Refine - Theme and Key Issues New models needed to enhance value drivers with continued margin pressure Key Issues in achieving an “Interactive Refinery” model: • Improve collaborative planning • Head toward real-time performance management • Reduce deviations from plan/schedule • Verify data consistency/visibility over hydrocarbon supply chain • Accurate and timely feedstock/product quality

Refine Web Value Added Utilizing the web can enhance decision processes • Collaboration across plants or functional departments • Consistent performance management with accountability • Improved knowledge management & best practice sharing • Improved data consistency • Faster decision processes Websites • OilMonitor.com • Honeywell - Myplant.com • AspenTech - ProcessCity.com • Refiningonline.com

Refine - E-Business Examples There are numerous examples of E-Business offerings developing: • PricewaterhouseCoopers - (OilMonitor.com) is a web-based crude oil evaluation service that provides crude oil characterization data, whole crude property trending, discussion forums for topics related to oil quality and US petroleum import reports. The site will add functionality related to standardized and customized assay-cutting, assay formats and linear programs. • Honeywell - (www.myplant.com) Microsoft recently joined Honeywell in an alliance to accelerate the growth of MyPlant.com by increasing the site’s reach and offerings significantly. It is a forum for plant managers, engineers, and other operations people to exchange ideas, use Honeywell software to simulate their processes, buy Honeywell products and even view banner ads from other manufacturers.

Refine - E-Business Examples There are numerous examples of E-Business offerings developing: • AspenTech - (www.processcity.com) provides a collaborative B2B portal for many process industries, with content and services directed at refining, petrochemical, chemical, polymers, life sciences, specialty chemicals and others. Members can interact, share ideas, get news & information, find jobs, buy books, access software, tools, services and other resources relevant to their process work. • RefiningOnline - (www.refiningonline.com) provides a web-based value-added information on refinining. The website is aimed at refining industry professionals ranging from engineers to consultants to business managers. One of the main features of the site is an online Q&A for refining-related issues.

Refine - Business Case 1 Feedstock quality impacts of $0.04 - $0.15/bbl • Lack of transparency in true crude oil quality • Transport quality degradation not tracked or sufficiently analyzed • Outdated crude oil quality representation results in non-optimal crude slate • Undetected crude oil quality variation decreases refinery performance • Most feedstock quality processes are still very manual and time-consuming Solution: • One centralized internet hub for oil quality information • Automated data gathering / retrieval / model loading • Shared costs/resources for crude oil quality tracking Solution Benefits/Value • Improved crude slate optimization • Improved quality of domestic common streams (LLS, WTI, WTS) • Reduced crude testing costs; reduced time cycles for quality updates • Profit Improvement of $0.04 - $0.15/bbl of crude

Price Reporting Services (e.g. Platt’s, OPIS) Futures Exchanges (NYMEX, IPE, SIMEX) Other Paper Markets GAP Understanding Oil Supply Risks Parameters, Drivers and Management of Risks Risk Parameter RiskDriver Management Facilitated by: • Pricing Window • Pricing Formula Terms • Volatility • Ability to Hedge • Quality Transparency Price Oil Supply Risk • Wellhead quality • Gathering/blending • Cargo degradation • Pipeline degradation • Producer Assays (infrequent) • GAP • Receipt Testing (too late) Delivered Quality Delivery Timing • Cargo Load Window • Cargo Discharge Window • Transit Time • Pipeline Schedule • Storage Capacity Avails • Ability to “time trade” cargo • Logistics/Supply Coordination • Inventory Management

Today, because of cost pressures, most refiners under-invest in quality monitoring and management, spending less than 0.5 cents/bbl. Typical Refinery Feedstock Quality Relieving constraints in Feedstock Quality Management (FQM) is the big prize A shift from cost-focused to value-focused quality management is needed Gross Margin Incentives 4 to 15 Cents / bbl 15 10 5 0 3 Accounting High-return investments in FQM are easily justified 2 Legal Cents / bbl Crude Cents / bbl Crude Procurement 1 Taxes Average Personnel Analytical “Best Practice” 0 Feedstock Quality Management (FQM) Crude Quality Monitoring Costs vs. Other Less-Value-Added Functions Recognizing the gap between current spending levels and potential benefits warrants an increase in resources for FQM

Feedstock Quality Management (FQM) Practices In-house opportunities for improvement • Develop formal FQM process w/ Sponsor and Owner • Implement centralized database repository with assay tool • Consider outsourcing crude analysis work • Conduct “commodity” analyses; in-source proprietary know-how • Identify areas for simulated distillation or on-line analyzer applications

Sales Contract Thereby and wheretofore all parties are in agreement that the aforementioned proposed plan to build on confirmed site shall be witnessed by all parties and executed this day of April 7, 2000. In the interests of the owner and the agent, this contract furthermore shall serve to unite said parties to this agreement and be considered legally binding in a court of law. • Expanded quality specs • Independent reference for baseline (‘typical’) specs Feedstock Quality Management (FQM) Practices Industry drivers to enhance quality information • Industry Solutions COQG • Participate in industry Crude Oil Quality Group (COQG) consortium to address supply chain quality issues • Establish independent, centralized quality monitoring and reporting service • Approach crude producers and common carriers about adding meaningful quality specs to contract terms OilMonitorTM

Sales Contract Thereby and wheretofore all parties are in agreement that the aforementioned proposed plan to build on confirmed site shall be witnessed by all parties and executed this day of April 7, 2000. In the interests of the owner and the agent, this contract furthermore shall serve to unite said parties to this agreement and be considered legally binding in a court of law. • Expanded quality specs for sales contracts • OilMonitor used as reference for “typical specs” OilMonitor.com - Purpose Price transparency links to feedstock quality • To make crude oil quality more transparent to the oil industry; price transparency requires quality transparency • To facilitate each refiner’s quality management process - data accuracy, speed, data utility • To provide oil quality ‘intelligence’ - new streams to market, quality changes to existing streams, predicted quality

OilMonitor.com - Benefits to the Refinery Reduce margin risk associated with feedstock quality • Assay and other testing costs are significantly cheaper • More frequent and more comprehensive data - OilMonitoras a “one-stop shop” • Assay is provided in usable format for expediting LP modeling • Ability to characterize quality variation for use in crude oil valuation improves quality and optimality of crude selection • Refiners can evaluate quality on crudes not routinely run • Crude quality variation should decrease with increased measurement and attention • All corners of the globe can participate in OilMonitorto provide even greater span of quality data

Economic Impact of Crude Oil Quality Variation Small variations yield large economic impact Quality Variation Annual Impact 2% Yield Variation Impact, $/bbl per 100 M BPD Economic Basis $2/bbl value delta $ 0.04 $1.5 MM Diesel to VGO 0.10 $5/bbl value delta 3.6 MM VGO to Resid 0.20 7.2 MM $10/bbl value delta Naphtha to light ends Overall Crude 0.06 Typical pipeline quality bank 2.2 MM Sulfur +/- 0.1 wt% value of $0.60 per 1 wt% sulfur 0.15 Typical pipeline quality bank 5.5 MM Gravity +/- 1 degree API value of $0.15 per deg API $0.04 - 0.55 $1.5 - 20.0 MM Consistent v. Common Stream Range of Valuation

Refine - Business Case 2 Hydrocarbon supply chain planning across system • Delayed communication and decisions regarding high $ impact events • No mechanism to quickly “re-publish” operating plan once “copies are made and the meeting is over” • No common view of economic drivers across supply chain, “what’s ‘my’ optimal vs. what’s ‘your’ optimal” • Disparate planning decision support tools with no visibility outside of functional “walls” • Accuracy of planning model constraints Solution: • Packaged intranet platform for collaborative planning - “Virtual Plan” • Common standards for planning documents; defined processes, workflow Solution Benefits/Value • Better decisions and faster decision cycles • Rapid deployment of IT platform; low cost roll-out • Managed work processes; knowledge organization and capture • Profit Improvement of $010 - $0.30/bbl of crude