Download

1 / 41

440 likes | 650 Views

The Industry Supply Curve. Industry Supply Curve. Industry Supply Curve is the relationship between price and the total output of an industry as a whole Up to this point, was called the supply curve or the market supply curve. Short-Run Industry Supply Curve.

E N D

Industry Supply Curve • Industry Supply Curve is the relationship between price and the total output of an industry as a whole • Up to this point, was called the supply curve or the market supply curve

Short-Run Industry Supply Curve • Jennifer and Jason’s farm is producing organic tomatoes and assume there are 100 organic tomatoes farms and they all have the same costs as Jennifer and Jason

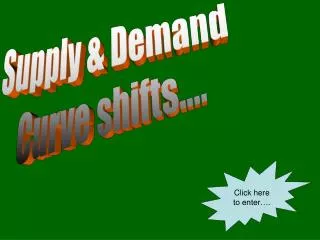

The Short-Run Market Equilibrium All 100 farms has the same individual short-run supply curve. At the price below $10, no farms will produce. Price, cost of bushel Short-run industry supply curve, S $26 22 E MKT Market price 18 D 14 Shut-down price 10 At a price of more than $10, each farm will produce the quantity of output at which its marginal cost is equal to the market price. Each farm will produce 4 bushels if the price is $14, at 5 bushels the price is…..6 bushels…… 0 200 300 400 500 600 700 Quantity of tomatoes (bushels)

Short-Run Industry Supply Curve • All leads to the short-run industry supply curve • This curve shows how the quantitative supplied by an industry depends on the market price given by a fixed number of producers

Short-Run Industry Supply Curve • EMKT is the short-run market equilibrium where the quantity supplied equals the Quantity demanded, taking the number of producers as given

Long-Run Industry Supply Curve • New producers will enter the industry whenever existing producers are making a profit – whenever the market price is above the break-=even price of $14 a bushel • If the new firms enter the industry, the quantity supplied at any given price will increase

Long-Run Industry Supply Curve • The EMKT had a equilibrium market price of $18 and a quantity of 500 bushels. At this price, existing producers are profitable • The existing firm makes a total Profit shown by the A rectangle when the market price is $18 • These profits will induce new producers to enter the industry, shifting the short-run industry supply curve to the right

Long-Run Industry Supply Curve • The effect of the new producers on the existing farm is a fall in price causes it to reduce its output and its profits fall to the rectangle B • The profit of the existing firms is diminishing to DMKT but this also means that the numbers of firms will continue to rise

Long-Run Industry Supply Curve • EMKT and DMKT and CMKT is a short-run equilibrium • Since the price of $14 is each firm’s break-even price, an existing producer makes zero profit, earning only opportunity cost of the resource used in production • CMKT = long-run market equilibrium which is when the quantity supplied equals the quantity demanded, given that sufficient time has elapsed for entry into and exit from the industry to occur

Long-Run Industry Supply Curve • In the long-run market equilibrium, all existing and potential producer have fully adjusted to their optimal long-run choices, as a result, no producer has an incentive to either enter or exit the industry

The Effect of an Increase in Demand in the Short Run and the Long Run (b) Short-Run and Long-Run Market Response to Increase in Demand (a) Existing Firm Response to New Entrants (a) Existing Firm Response to Increase in Demand Price, cost Price Price, cost Long-run industry supply curve, Higher industry output from new entrants drive price and profit back down. An increase in demand raises price and profit. LRS S S MC 1 2 MC $18 Y A T C A T C Y Y MKT 14 X Z D Z X 2 MKT MKT D 1 0 0 Q Q Q 0 Quantity Quantity Quantity X Y Z Increase in output from new entrants

Long-Run Industry Supply Curve • The LRS line that passes through XMKT and ZMKT is the long-run industry supply curve • Shows how the quantity supplied by an industry responds to the price given that producers have had time to enter or exit the industry • In the example, the long-run industry supply curve is horizontal at $14 – what does this say about its elasticity?

Long-Run Industry Supply Curve • Perfectly elastic! • In the example, the industry supply is perfectly elastic in the long run • Perfectly elastic long-run supply is actually an assumption for many industries—it shows constant costs across the industry • Each firm (regardless of it being an incumbent or a new entrant) faces the same cost structure

Long-Run Industry Supply Curve • Example of these industries: agriculture or bakeries • Use some product that is in limited supply (inelastically supplied) • When industry expands…..price of that input is driven up • Consequently, later entrants in the industry find that they have a higher cost structure than early entrants • Example: beachfront resort hotels

Long-Run Industry Supply Curve • Regardless of if long-run industry supply curve is horizontal or upward sloping or even downward sloping, the long-run price elasticity of supply is HIGHER than the short-run elasticity whenever there is free entry and exit

Long-Run Industry Supply Curve • Long-run industry supply curve is always flatter than the short-run industry supply curve • WHY???? • The reason is entry and exit – a high price caused by an increase in demand attracts entry by new producers, resulting in a rise in industry output and an eventual fall in price

The Cost of Production & Efficiency in Long-Run Equilibrium • Three conclusions about cost of production and efficiency in the long-run equilibrium of a perfectly competitive industry: • in a perfectly competitive industry in equilibrium, value of marginal cost is the same for all firms • WHY? • All firms produce the quantity of output at which MC equals the market price and as price-takers, all face the same market price

The Cost of Production & Efficiency in Long-Run Equilibrium • In a perfectly competitive industry with free entry and exit, each firm will have zero economic profit in long-run equilibrium • Firms produce the quantity of output that minimizes its ATC • TC of production of the industry’s output is minimized in a perfectly competitive industry

The Cost of Production & Efficiency in Long-Run Equilibrium • Long-run market equilibrium of a perfectly competitive industry is efficient: no mutually beneficial transactions go unexploited • WHY? • All consumers have a willingness to pay greater than or equal to sellers’ cost actually get the good

The Cost of Production & Efficiency in Long-Run Equilibrium • In the long-run equilibrium of a perfectly competitive industry, production is efficient: costs are minimized and no resources are wasted • Allocation of goods to consumers is efficient: every consumer willing to pay the cost of producing a unit of the good gets it

Industry Supply Curve • Industry Supply Curve is • Up to this point, was called the supply curve or the market supply curve

The Short-Run Market Equilibrium Price, cost of bushel Short-run industry supply curve, S $26 22 E MKT Market price 18 D 14 Shut-down price 10 0 200 300 400 500 600 700 Quantity of tomatoes (bushels)

Short-Run Industry Supply Curve • All leads to the short-run industry supply curve • This curve shows how the

Short-Run Industry Supply Curve • EMKT is the short-run market equilibrium where the

Long-Run Industry Supply Curve • New producers will enter the industry whenever existing producers are making a profit – whenever the market price is above the break-=even price of $14 a bushel • If the new firms enter the industry, the quantity supplied at any given price will increase

Long-Run Industry Supply Curve • The EMKT had a equilibrium market price of $18 and a quantity of 500 bushels. At this price, existing producers are profitable • The existing firm makes a total Profit shown by the A rectangle when the market price is $18 • These profits will induce new producers to enter the industry, shifting the short-run industry supply curve to the right

Long-Run Industry Supply Curve • The effect of the new producers on the existing farm is a fall in price causes it to reduce its output and its profits fall to the rectangle B • The profit of the existing firms is diminishing to DMKT but this also means that the numbers of firms will continue to rise

Long-Run Industry Supply Curve • EMKT and DMKT and CMKT is a short-run equilibrium • Since the price of $14 is each firm’s break-even price, an existing producer makes zero profit, • CMKT = long-run market equilibrium which is when the quantity supplied equals the quantity demanded, given that sufficient time has elapsed for entry into and exit from the industry to occur

Long-Run Industry Supply Curve • In the long-run market equilibrium,

The Effect of an Increase in Demand in the Short Run and the Long Run (b) Short-Run and Long-Run Market Response to Increase in Demand (a) Existing Firm Response to New Entrants (a) Existing Firm Response to Increase in Demand Price, cost Price Price, cost LRS S S MC 1 2 MC $18 Y A T C A T C Y Y MKT 14 X Z D Z X 2 MKT MKT D 1 0 0 Q Q Q 0 Quantity Quantity Quantity X Y Z

Long-Run Industry Supply Curve • The LRS line that passes through XMKT and ZMKT is the long-run industry supply curve • In the example, the long-run industry supply curve is horizontal at $14 – what does this say about its elasticity?

Long-Run Industry Supply Curve • __________________! • In the example, the industry supply is perfectly elastic in the long run • Perfectly elastic long-run supply is actually an assumption for many industries—it shows constant costs across the industry

Long-Run Industry Supply Curve • Example of these industries: agriculture or bakeries • When industry expands…..price of that input is driven up • Consequently, later entrants in the industry find that they have a higher cost structure than early entrants

Long-Run Industry Supply Curve • Regardless of if long-run industry supply curve is horizontal or upward sloping or even downward sloping, the long-run price elasticity of supply is HIGHER than the short-run elasticity whenever there is free entry and exit

Long-Run Industry Supply Curve • Long-run industry supply curve is always flatter than the short-run industry supply curve • WHY???? • The reason is entry and exit –

The Cost of Production & Efficiency in Long-Run Equilibrium • Three conclusions about cost of production and efficiency in the long-run equilibrium of a perfectly competitive industry: • in a perfectly competitive industry in equilibrium, value of marginal cost is the same for all firms

The Cost of Production & Efficiency in Long-Run Equilibrium • In a perfectly competitive industry with free entry and exit, each firm will have zero economic profit in long-run equilibrium

The Cost of Production & Efficiency in Long-Run Equilibrium • Long-run market equilibrium of a perfectly competitive industry is efficient: no mutually beneficial transactions go unexploited

The Cost of Production & Efficiency in Long-Run Equilibrium • In the long-run equilibrium of a perfectly competitive industry, production is efficient: • Allocation of goods to consumers is efficient: every consumer willing to pay the cost of producing a unit of the good gets it