Download

1 / 20

200 likes | 333 Views

The Iridium '‘Team’'. Issues in Iridium. How Valuable is Reputation and Quality of Sponsor What Risks are Debt Risks versus Equity Risks Marketing Risks Pricing of Product Convenience of Product Technology and Pricing Flexibility What is the capacity if lower price and increase volumes.

E N D

Issues in Iridium • How Valuable is Reputation and Quality of Sponsor • What Risks are Debt Risks versus Equity Risks • Marketing Risks • Pricing of Product • Convenience of Product • Technology and Pricing Flexibility • What is the capacity if lower price and increase volumes

Basic Problem of Project Finance – No History (From Iridum Prospectus) • Iridium is a development stage enterprise with no operating history.. Accordingly, all statements in this Prospectus that are not clearly historical in nature are forward looking. Examples of such forward looking statements include the statements concerning Iridium's operations, prospect s, markets, technical capabilities, funding needs, financing sources, pricing, launch schedule, commercial operations schedule, estimates of the size of addressable markets for mobile satellite services, estimates of customer counts, the last year in which Iridium will have negative cash flow and a net increase in year-end borrowings, and future regulatory approvals, as well as information concerning expected characteristics of competing systems and expected actions of third parties such as equipment suppliers, gateway operators, service providers and roaming partners. These forward looking statements are inherently predictive and speculative and no assurance can be given that any of such statements will prove to be correct. Actual results and developments may be materially different from those expressed or implied by such statements.

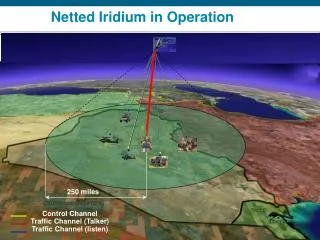

Iridium Concept - Continued • Iridium Operating LLC ("Iridium") is developing and commercializing a global mobile wireless communications system that will enable subscribers to send and receive telephone calls virtually anywhere in the world -- all with one phone, one phone number and one customer bill. The IRIDIUM communications system (the "IRIDIUM System") will combine the convenience of terrestrial wireless systems with the global reach of Iridium's satellite system. • The IRIDIUM System encompasses four components: • the "space segment," which will include the low earth orbit satellite constellation and the related control facilities; • the ground stations or "gateways," which will link the satellites to terrestrial communications systems; • the Iridium subscriber equipment, which will provide mobile access to the satellite system and terrestrial wireless systems; and • the terrestrial wireless interprotocol roaming infrastructure, which will facilitate roaming among the Iridium satellite system and multiple terrestrial wireless systems that use different wireless protocols.

Launch of Satallites • The first launch of Iridium satellites occurred on May 5, 1997. Iridium expects to commence commercial operations in September 1998. The satellite constellation is being designed, assembled and delivered in orbit by Motorola, Inc. ("Motorola"), a leading international provider of wireless communications systems, phones and pagers, semiconductors and other electronic equipment. Motorola also is the principal investor in Iridium, having provided investments, guarantees and conditional to provide guarantees totaling over $1.1 billion, including its conditional commitment to guarantee up to an additional $350 million of borrowings under the Guaranteed Bank Facility described below. • Other strategic investors include leading wireless communications service providers from around the world, as well as experienced satellite manufacturers and experienced launch providers. Iridium is a wholly owned subsidiary of Iridium LLC, a Delaware limited liability company ("Iridium LLC" or "Parent").

Example of Technical Obsolescence – Iridum Feasibility Studies $880 million bridge financing 66 Low earth orbiting satellites International charges $4-7 per minute Handsets cost $3,000 each

Demand Expectations for Telecom • During the boom many people believed that Internet traffic was doubling roughly every 100 days. This fantasy was based on statements made by WorldCom in the 1997 time frame….It led to financiers to put up trillions of dollars in capital. After all, demand would soon catch up with whatever supply that could be built. • The specific reference to this growth rate was a statement of the chief financial officer of Worldcom, John Sidgemore, who stated[1]: • We’re seeing growth at an unprecedented level. Our backbone doubles every 3.7 months, which means that it’s growing by a factor of 10 every year. So three years from now, we expect our network to be 1,000 times the size it is today. . . . The big challenge is to deploy infrastructure fast enough to accommodate such a growth rate. We’re in a supply-constrained economy for the first time in the telecom industry. • Crowe, Thomas, “The Telecom Meltdown…Looking For The Underlying Reasons”

The Iridium Concept International Coverage 66-LEO Satellites Launched 72; got 67; 5-year life each 12 Ground Stations Handset Cost = US$3,000 Call Cost = US$3.00-US$7.50 per min. US$800 million PF LIBOR + 4%; 2-year Bullet

Standard and Poors and Housing Price Assumptions – Comparison with Iriduim Assumptions According to one story an investor called the rating agency Standard & Poor’s and asked what would happen to default rates if real estate prices fell. “The man at S&P couldn’t say; its model for home prices had no ability to accept a negative number. ‘They were just assuming home prices would keep going up…’”

The Iridium Concept • Coverage? • Does not work in your car • Does not work in a city • interference from buildings • Does not work as you exit an airport • Satellite crosses the sky in ca. 14 minutes • handover software aboard the satellites

Forgetting Fundamentals of Supply and Demand and Back of the Envelope Analysis -- Telecommunications • At the end of the day you should evaluate whether forecasts make sense in light of fundamental economic principles. • In the 1990’s telecoms seemingly limitless upside potential • Venture capitalists and stock investors fell over each other to invest insane amounts of money in many companies • Success of internet companies premised oh high growth continuing • When companies failed to generate cash flow, defaulted companies skyrocketed • Barriers to telecommunications companies came down • Telecommunications network became overbuilt due to lack of demand

Telecommunications Meltdown • In 2001, 77 telecommunications companies sought bankruptcy • In 2000, 20 declared bankruptcy. • Two Trillion in Market Value Lost • Large bankruptcies included: • WorldCom’s -- the single largest bankruptcy in U.S. history. • The fiber optic network operator, Global Crossing, 4th largest • Other leaders -- Williams Communications Group and Network Plus • Reasons • Long distance price competition in pursuit of retaining market share. • Entry into local markets blocked. • It's fallout from a telecoms industry in which supply has dwarfed demand.

Surplus Supply in Telecommunications • . • There was an overbuilding of telecom capacity based on the fantasized vision of the objectives of the New Economy, which will never be realized. For example, there was an overbuilding of fiber-optic cable systems by a factor of at least 10. Many New Economy companies were built based on the idea that the telecom sector would expand perpetually by 15 to 30% per annum.

Demand versus Supply • The result is overcapacity: 39 million miles of cable were laid underneath railroad beds, natural gas lines, corn fields, and roads—enough to encircle the Earth more than 1,500 times. Today less than 5% of the cable is "lit"; the rest remains dark, and most is not likely to be "lit." • But reality has further asserted itself, causing additional problems in the physical economy and revenues of the telecom sector, and ripping apart that sector's two fundamental assumptions. The sector's CEOs thought that increased volumes of data traffic, as opposed to voice calls, would be the savior of the telecom industry. But data users, mostly corporations, instead of paying on the more expensive per-minute basis, are paying for the data in bulk. On this basis, data transmission is not even as profitable as old-fashioned voice calls. • Belief that voice-call traffic would rise. But alarmed industry executives report that people are sending millions of e-mails per day, instead of spending money for telephone calls. Some industry sources now predict that, in the future, the volume of voice calls will fall each year.

Financial and business problems • The telecom sector collapse is driven by two intertwined forces. • First, it is over-leveraged: Its companies borrowed enormous sums of money during the 1990s, to finance a wave of mergers and some expansion. Telecoms' total outstanding debt—still estimated at $650 billion or more—requires debt service far larger than that portion of the sector's revenue stream available to service it; it is sucking the telecom sector dry. • Every company that could get its hands on the stuff proclaimed that it was going to build a national, or super-regional fiber-optic network. In some cases, four to six companies built fiber-optic cable networks between or within the same major cities, far beyond prospective levels of voice or data transmission.

Technology Risk • Project Financing is seldom applied to new technology. • Can take technology risk if: • Known and proven technology is used; • The facilities are projected to remain technologically competitive; and • Plant/project life is longer than the funding life; • Project financiers do not want to be ‘first’ to bank a project with new technology. • If an untried taechnologyis incorporated into a new project, most financiers will require extra support. • Liquidated damage provisions after the plant is complete • Added insurance • Sponsor guarantee • Covenants will be required to ensure that the borrower applies generally accepted operating practices and obeys the applicable laws including environmental regulations. (the "prudent operator" clause).