Download

1 / 43

440 likes | 601 Views

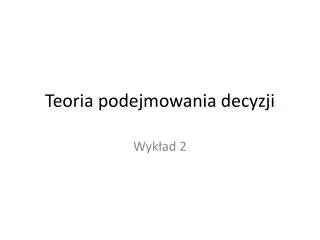

Teoria podejmowania decyzji. Wykład 7. Reduction of compound lotteries. 1. A. 1/2. A. 1/3. 1/4. A. 1/2. 1/2. 1/3. 3 / 8. B. B. 3 / 8. 1/3. C. 1/2. 1/2. A. 1/4. A. 3 / 8. 1/2. B. 3 / 8. C. C. 1/2. A. 1/4. B. 1/4. C. Von Neumann Morgenstern proof graphically 1.

E N D

Teoria podejmowania decyzji Wykład 7

Reduction of compound lotteries 1 A 1/2 A 1/3 1/4 A 1/2 1/2 1/3 3/8 B B 3/8 1/3 C 1/2 1/2 A 1/4 A 3/8 1/2 B 3/8 C C 1/2 A 1/4 B 1/4 C

Fallacy (2) • Fire insurance: • Fire: paythepremium, house rebuilt (C) • No Fire: paythepremium, house untouched (B) • No insurance: • Fire: house burnt, no compansation (D) • No Fire: house the same (A) • A≻B≻C≻D • Supposetheprobability of fireis 0.5 • And an individualisindifferentbetweenbuying and not buyingthe insurance • AlthoughFire insurance hassmallervariance and ½u(A) + ½u(D) = ½u(B) + ½u(C), itdoes not meanthatFire insurance should be chosenover No insurance Loss = $70K Loss = $60K Loss = $100K Loss = $0 Riskaverse, and EL(insurance) = $65K EL(no insurance) = $50K

Fallacy (3) • Fire insurance: • Fire: paythepremium, house rebuilt (C) • No Fire: paythepremium, house untouched (B) • No insurance: • Fire: house burnt, no compansation (D) • No Fire: house the same (A) • A≻B≻C≻D • Supposethattheprobability of fireis ½ and an individualprefers not buyingfire insurance and hence ½u(A) + ½u(D) > ½u(B) + ½u(C) ⇒ u(A) - u(B) > u(C) - u(D) • Howeveritdoes not meanthatthechangefrom B to A ismorepreferredthanthechangefrom D to C. • Preferencesaredefinedoverpairs of alternatives not pairs of pairs of alternatives

Crucial axiom - independence • Our version • The general version • Why the general version implies our version?

Independence – examples • If I prefer to go to the moviesthan to go for a swim, I mustprefer: • to toss a coin and: • heads: go to the movies • tails: vacuumclean • than to toss a coin and: • heads: go for a swim • tails: vacuumclean • If I prefer to bet on red than on even in roulette, then I mustprefer: • to toss a coin and • heads: bet on 18 • tails: bet on red • than to toss a coin and: • heads: bet on 18 • tails: bet on even

Machina triangle p2 x2 1 1-a P a aP+(1-a)R x1 R x3 1 p1

Independenceassumption in the Machina triangle Suppose that A1 is better than A2 is better than A3 p2 1 αP+(1-α)R P αQ+(1-α)R R Q 1 p1

17.1 and 17.2 17.1) Choose one lottery: P=(1 mln, 1) Q=(5 mln, 0.1; 1 mln, 0.89; 0 mln, 0.01) 17.2) Choose one lottery: P’=(1 mln, 0.11; 0 mln, 0.89) Q’=(5 mln, 0.1; 0 mln, 0.9) Kahneman, Tversky (1979) [commonconsequenceeffectviolation of independence] Many peoplechoose P over Q and Q’ over P’

Common consequence graphically P = (1 mln, 1) P’= (1 mln, 0.11; 0, 0.89) Q = (5 mln, 0.1; 1 mln, 0.89; 0, 0.01) Q’= (5 mln, 0.1; 0, 0.9) • If we plug c = 1mln, we get P and Q respectively • If we plug c = 0, we get P’ and Q’ respectively

18.1 i18.2 18.1) Choose one lottery: P=(3000 PLN, 1) Q=(4000 PLN, 0.8; 0 PLN, 0.2) 18.2) Choose one lottery: P’=(3000 PLN, 0.25; 0 PLN, 0.75) Q’=(4000 PLN, 0.2; 0 PLN, 0.8) Kahneman, Tversky (1979) [common ratio effect, violation of independence] Many peoplechoose P over Q and Q’ over P’

Common ratio graphically P=(3000 PLN, 1) P’=(3000 PLN, 0.25; 0 PLN, 0.75) Q=(4000 PLN, 0.8; 0 PLN, 0.2) Q’=(4000 PLN, 0.2; 0 PLN, 0.8)

Monotonicity of utilityfunction • prefersmore to less • currentwealth x • probability p of bankruptcy (u(0)=0) • how much to pay to avoidit?

Monotonicity of utilityfunction F(x) 1 x

First Order StochasticDominance (FOSD) cdf cdf 1 1 1 1 t t

FOSD • Assume X and Y aretwodifferentlotteries (FX(.), FY(.) are not the same) • LotteryX FOSD Y if: For all a, hence: Thosewhoprefermore to less willneverchooselotterythatisdominated in the abovesense. • Theorem: X FOSD Y if and onlyif Eu(X) ≥ Eu(Y), for allinreasing u

Marginalutility x+d Todaychancenodessplit 50:50 x-d x

Marginalutility utility payoff

Certaintyequivalent and riskpremium 4,5 1 2 0,5 0,5 utility 10 6 1

Marginalutility • x – initialwealth (number) • l – lottery with zero exp. value (randomvariable) • k –multiplier (we tak k close to zero) • d – riskpremium (number) • x-d – certaintyequivalent for x+l

Second Order StochasticDominance cdf 1 t 1 1 1 t

SOSD • Assume X and Y aretwodifferentlotteries (FX(.), FY(.) are not the same) • LotteryX SOSD Y if: For all a hence: • Thosewhoareriskaversewillneverchoose a lotterythatisdominated in the abovesense. • Theorem: X SOSD Y if and onlyif Eu(X) ≥ Eu(Y), for allinreasing and concave u

Mean-variancecriterium • Riskaversiondoesn’tmeanthatalways: A betterthan B, ifonly E(A)=E(B) and Var(A)<Var(B) • somelotteries do not result from another with meanpreservingspread • istruewhenVar(A)=0 • Mean-variancecriteriumworkse.g. for normallydistributedrandomvariables (lotteries)

Measures of riskaversion • Riskpremiummeasuresriskaversion with respect to a givenlottery • As a function of payoffvaluesriskaversionismeasured by Arrow, Prattmeasures of (local) riskaversion

Exercise 1 • From now on let’sassume X is a set of monetarypay-offs (decisionmakerprefersmoremoneythan less) • Decisionmaker with vNMutilityfunctionpreferslottery (100, ¼; 1000, ¾) to (500, ½; 1000, ½) • Whatis a realtionbetween(100, ½; 500, ¼; 1000, ¼) and (100, ¼; 500, ¾)? • Suggestion – we canarbitrarily set utilityfunction for twooutcomes

Exercise 2 • Decisionmakerisindifferentbetweenpairs of lotteries:(500, 1) and (0, 0,4; 1000, 0,6)and (300, 1) and (0, ½; 500, ½) • Can we guess the preferencerelationbetween(0, 0,2; 300, 0,3; 1000, ½) and (500, 1)?

Exercise 3 • Decisionmaker with vNMutilityisriskaverse and indifferentbetween the followingpairs(400, 1) and (0, 0,3; 1000, 0,7)and(0, ½; 200, ½) and (0, 5/7; 400, 2/7) • Can we guess the preferencerelationbetween(200, ½; 600, ½) and (0, 4/9; 100, 5/9)? • (suggestion – remamberthanvNMutilityisconcave)