Download

1 / 9

90 likes | 92 Views

For the average Canadian, buying a home is impossible without the financial vehicle of a mortgage, and through the ensuing contract, theyu2019re able to pay for a property in exchange for monthly payments, plus interest.

E N D

Mortgage Guidance For First Time Buyers In Canada

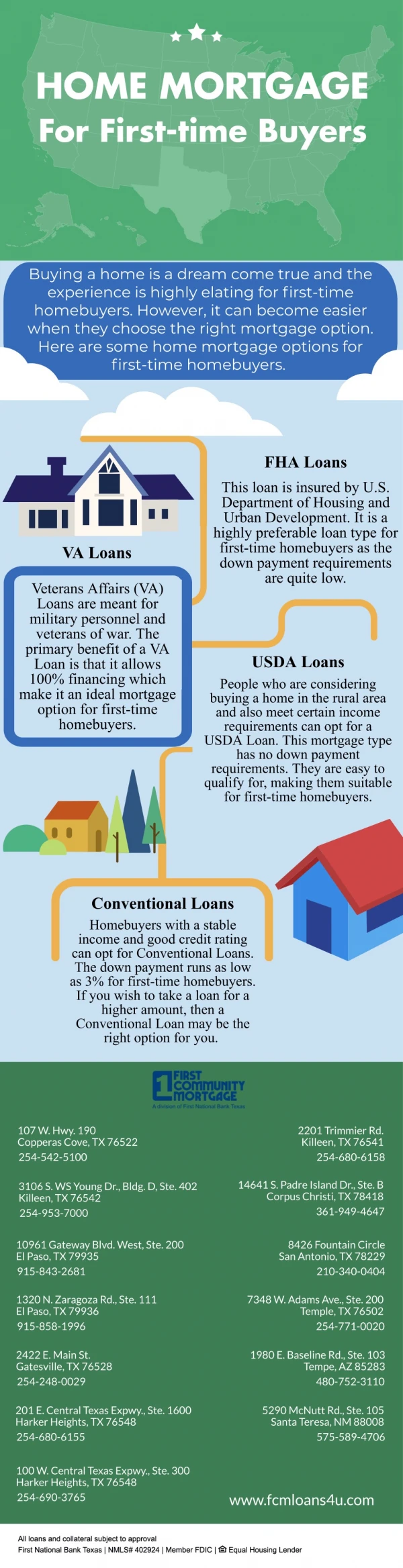

For the average Canadian, buying a home is impossible without the financial vehicle of a mortgage, and through the ensuing contract, they’re able to pay for a property in exchange for monthly payments, plus interest. If you’re a first-time property buyer in Canada, you might be interested to know what mortgage options are available to you: Mortgage types in Canada: Conventional mortgages – these are not insured by or guaranteed, by the government ●

Government-insured mortgages – these are insured or guaranteed by a government agency such as the Federal Housing Administration or the Veteran’s Administration Fixed-rate mortgages – dividing interest payments evenly throughout the lifespan of the loan, these mortgages mean that the payment amount never changes, since the interest rate is fixed. Adjustable rate mortgages – these mortgages have interest rates that can go up or down during the period of the loan, and while the initial rate of interest is typically lower at the beginning of the loan, it then increases over time. If you anticipate that your income may increase over time, this type of mortgage might be an appealing prospect for you. ● ● ●

Getting preapproved for a first-time mortgage The process of pre-approval is one that helps lenders to determine how much you can afford to spend on a home, and many real estate agents will insist upon prospective buyers having a letter of pre-approval before any official offer on a property is placed. If you have a poor credit score, you should try and take steps to improve it before seeking a mortgage pre-approval.

Here’s how to obtain pre-approval: Find a suitable lender with the help of a local mortgage broker With their help, gather up paperwork proving your current employment, and which verifies your earnings Gather bank statements and other documents that prove you have enough funds to make a down-payment. Finally, schedule a pre-approval appointment with the lender of your choice. ● ● ● ●

Work with a mortgage broker to help you find a suitable lender While your first instinct might be to go to your bank (or any bank) to find a mortgage, they aren’t always the right choice for everyone. A lot will depend upon your individual circumstances, but it’s important to note that banks are regulated at a federal level through the FDIC, and as such, their mortgages must adhere to certain federal lending guidelines. For you, this might limit your options.

The best way to find a lender that will offer you a mortgage at a great rate, and with conditions that match your existing financial circumstances, is to work with a local mortgage broker. They will have access to a whole variety of other lending options that you might not even have known existed, and can introduce you to offers from private lenders that are exclusive to them. Other costs to factor in when buying your first home On top of the monthly principal payment you’ll be required to make on your mortgage loan, you’ll also need to factor in the following costs:

Mortgage insurance Homeowners insurance Property taxes Homeowners association fees Closing costs ● ● ● ● ● Buying your first home in Canada need not be a stressful or daunting time; seek help from a knowledgeable local mortgage broker and not only get yourself a great new home, but a great deal on a mortgage, too.

Mortgage-broker-Calgary is your best resource for finding a mortgage for your property. Luke Wile, is one of the best Calgary mortgage brokers and is proud to serve clients from across Canada, while being centered in Calgary, Alberta. Luke is proud to serve his clients with a personalized approach to finding his clients the best and lowest Canadian interest rates and terms offered by the major banks and private lending institutions. If you are looking for a mortgage specialist in Calgary, with Luke Wile you can get fast and personal expertise for your mortgage. Contact us today!