Download

1 / 24

240 likes | 322 Views

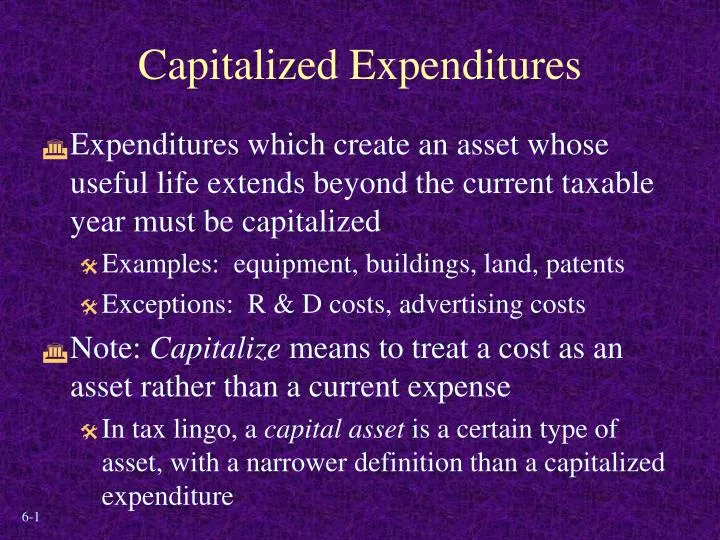

Capitalized Expenditures. Expenditures which create an asset whose useful life extends beyond the current taxable year must be capitalized Examples: equipment, buildings, land, patents Exceptions: R & D costs, advertising costs

E N D

Capitalized Expenditures • Expenditures which create an asset whose useful life extends beyond the current taxable year must be capitalized • Examples: equipment, buildings, land, patents • Exceptions: R & D costs, advertising costs • Note: Capitalize means to treat a cost as an asset rather than a current expense • In tax lingo, a capital asset is a certain type of asset, with a narrower definition than a capitalized expenditure

Cost Recovery of Capitalized Expenditures • When is the cost of a capitalized expenditure ‘recovered’ for tax purposes? • Over time? • When the asset is sold? • Other? • How is the cost of a capitalized expenditure recovered for tax purposes? • Permissible cost recovery methods? • Treatment of unrecovered cost on sale?

Types of Property • Define the following and provide examples of each: • Tangible property • Intangible property • Real property • Personal property

Initial Tax Basis of Business Assets • General rule: initial tax basis equals purchase price: • Cash paid + debt assumed or incurred + FMV of other property or services given up • Other purchase-related costs also included in initial tax basis: • Sales tax • Freight • Installation charges

Adjustments to Tax Basis of Tangible Business Assets • Must capitalize the costs of additional expenditures which materially increase the value or extend the useful life of the asset • Repairs vs. capital improvements • Which of the following costs must be capitalized? • Environmental cleanup/asbestos removal • New roof on building • Landscaping costs • Interior remodeling (carpet, partitions, etc.) • Paint

Adjustments to Tax Basis continued • Adjusted tax basis = Initial tax basis + capital improvements - depreciation/amortization/ depletion allowed or allowable • Adjusted tax basis represents the taxpayer’s unrecovered cost of the asset

Tax Depreciation under MACRS • WARNING: MACRS rules have changed significantly several times since enacted in 1981. Depreciation is determined by the rules in effect for the year in which an asset is placed in service. • The following discussion pertains to rules in effect for assets placed in service since 1993.

MACRS • Ten recovery periods • Specified by type of property • Usually shorter than useful life for GAAP • Conventions for year placed in service and year of disposition • Mid-year convention for 3- through 20-year property • Midquarter convention if > 40% of depreciable personalty acquisitions occur during final quarter • Mid-month convention for >20-year property • Tax depreciation ignores salvage value

MACRS Depreciation Methods • 200% DB for 3- through 10-year property • 150% DB for 15- and 20-year property • Straight-line for >20-year property • IRS tables provide percentages • Table percentages are applied to the asset’s initial tax basis (not adjusted tax basis) to determine each year’s depreciation amount • Mid-year and mid-month conventions for year of acquisition are built into tables • For year of disposition (if before end of recovery life) table percentages must be adjusted

Tax Basis of Intangible Assets • Costs of self-created intangibles must be capitalized and amortized over time period for which economic benefits expected • Many purchased intangibles subject to IRC. Sec. 197 • Amortized on straight-line basis over 15 years • Examples: Goodwill, covenant-not-to-compete, customer-based and workforce intangibles

Start-up and Organization Costs • Start-up Costs: Pre-operational costs and costing of investigating either the creation or acquisition of a business • Organization Costs: legal, accounting, filing and registration costs related to formation of a new corporation or partnership • Taxpayer may elect to amortize these costs over 60 months, beginning in the first month of operation of an active business

Mineral Rights • Costs of acquiring mining or drilling rights must be capitalized and are subject to depletion as mineral is removed • Cost = Adjusted Basis * Current production in unitsDepletion Estimated total units of production • Percentage Depletion = Gross Income * Statutory Rate • Greater of cost or percentage depletion for taxable year is deductible (property-by-property)

Current Deductions of Capital Expenditures • Sec. 179 (Limited Expensing) Election – NEW LAW CHANGES • $100,000 (2003-2006) of tangible personal property costs deductible in year of acquisition • Phased out for taxpayers with annual property expenditures > $400,000 • Currently deductible amount limited to taxable business income before this deduction • Post-Sept. 11 additional first year depreciation • Applies to tangible personal property, computer software and leasehold improvements • 30% of cost deductible in year of acquisition for acquisitions after 9/11/01 and before 5/6/03 • 50% of cost deductible in year of acquisition for acquisitions after 5/5/03 and before 1/1/05 (NEW LAW CHANGE)

Current Deductions of Capital Expenditures continued • Costs of removal of barriers to handicapped access ($15,000 annual maximum) • Soil and water conservation expenditures by farmers • Research and experimentation costs • Advertising • Costs of environmental remediation at targeted contamination sites • Intangible Drilling Costs

Tax Incentives Example: Oil and Gas Drilling and Development • Independent oil and gas companies receive two important tax incentives: • Current deduction for intangible drilling costs • Percentage depletion (15% of gross revenue) • Why are these favorable tax breaks offered? Without them, the riskiness of oil and gas exploration would deter many companies from investing in this activity

Example 1: Oil and Gas Incentives • Assume drilling costs of $100,000 for a well expected to produce 2,500 barrels of oil annually for 5 years. Current oil prices are $18 per barrel, and expected operating costs for the well are $6 per barrel. Assume a marginal tax rate for the independent producer of 34%, and a 7% discount rate.

Example 1 continued • Without special tax incentives to promote exploration, drilling costs would be capitalized and depleted, using cost depletion, over the productive life of the well. • Annual gross revenue $45,000Annual operating costs 15,000Annual depletion 20,000Net taxable income 10,000Annual tax cost 3,400Annual after-tax cash flow 26,600 • PV of 5 year after-tax returns $109,065Rate of Return on investment 9%

Example 1 continued • By allowing immediate expensing of drilling costs, the return on this investment increases significantly. • Annual gross revenue $45,000Annual operating costs 15,000Annual depletion 0Net taxable income 30,000Annual tax cost 10,200Annual after-tax cash flow 19,800 • PV of 5 year after-tax returns $81,184Tax benefit in year 1 from drilling cost deduction 34,000Total NPV $115,184 • Rate of Return on investment 15%

Example 1 continued • By also allowing percentage depletion of 15% of annual gross revenue, the return on this investment more than doubles from the non- tax-favored return. • Annual gross revenue $45,000Annual operating costs 15,000Annual depletion 6,750Net taxable income 23,250Annual tax cost 7,905Annual after-tax cash flow 22,095 • PV of 5 year after-tax returns $90,594Tax benefit in year 1 from drilling cost deduction 34,000Total NPV $124,594 • Rate of Return on investment 25%

Incorporating Cost Recovery into NPV Analysis • Initial cost of asset results in cash outflow • If acquired with debt, cash outflows occur for debt principal and interest payments • Tax savings generated by interest expense represents a cash inflow • Depreciation expense is not a cash outflow • Tax savings generated by depreciation expense represents a cash inflow

Accounting for Inventories • Must use accrual method - only cost of goods sold (COGS) is deductible • Two issues in determining COGS: • Product versus period costs (which costs are inventoriable) • Manufacturers and large retailers/wholesalers must determine inventory cost (product cost) for tax purposes using uniform capitalization rules, which are NOT consistent with GAAP • Allocation of costs to goods on hand versus goods sold (cost flow assumptions): • Specific identification, FIFO, LIFO • LIFO conformity requirement

Tax Implications of Asset Acquisitions: Planning Issues • The after-tax cost of an asset acquisition increases as the recovery life (period of time over which the asset’s cost may be deducted for tax purposes) increases • Leveraged financing of asset purchases, where the cost of the asset is financed over a period longer than the recovery period, can decrease the after-tax cost of an acquisition

Planning Issues continued • Another alternative: Lease vs. purchase • Tax treatment of leases: • Generally, annual lease payments are deductible • Up-front payments to acquire a lease must be capitalized and amortized over lease term • Some leases may be treated as purchases for tax purposes, depending on facts

Update to Book/Tax Difference List • Temporary Differences • Differences in inventoriable costs under Unicap rules • Differences between book and tax depreciation/ amortization/depletion • Sec. 179 (immediate expensing) deduction • Intangible drilling costs (full cost method for GAAP) • Deductible R&D costs • Permanent Differences • Percentage depletion in excess of investment