Download

1 / 16

200 likes | 656 Views

Foreign Exchange Rate Determination and Forecasting. Outline: I. Balance of Payment II. Parity Conditions Purchasing Power Parity Fisher Effect International Fisher Effect Forward Rate as Unbiased Predictor of Future Spot Rate Interest Rate Parity Covered Interest Arbitrage

E N D

Foreign Exchange Rate Determination and Forecasting • Outline: • I. Balance of Payment • II. Parity Conditions • Purchasing Power Parity • Fisher Effect • International Fisher Effect • Forward Rate as Unbiased Predictor of Future Spot Rate • Interest Rate Parity • Covered Interest Arbitrage • II. Foreign Exchange Rate Forecasting in Practice • Methods of Forecasting

I. Description of Balance of Payment Accounting • Summarizes economic transaction between residents of one country and the rest of the world. Transactions include • Import and Export of goods and services • Transfers • Capital Flows etc • BOP account as an itemization of the factors behind the demand and supply of a currency • Rules of Debits and Credits • Credits (+): Transactions that represent demands for the local currency in the foreign exchange market. Result from purchases by foreigners of goods, services, financial and real assets, gold and foreign exchange • Export of goods and services (sale • Receipt of gifts • Borrowing (sale of stocks, bonds etc • Investment by foreign residents (real estate, expansion of plant and equipment etc • Decrease in Official Reserve of gold/foreign currency

I. Description of Balance of Payment Accounting cont’d • Debits(-): Transactions that represent supplies of local currency in the foreign exchange market. Result from purchases by residents of goods, services, financial and real assets, gold, or foreign exchange from foreigners. • Import of goods and services • Gifts and Transfers • Lending (purchase of foreign stocks, bonds etc • Local investment in foreign countries • Increases in Official Reserve of gold/foreign currency • Balance of Payment Categories • Current Account - flow of goods, services and transfers • Capital + Financial Accounts - public and private investments and lending • Errors and omissions • Official Reserves Account - changes in holdings of gold and foreign currencies

I. Description of Balance of Payment Accounting cont’d • A Current Account Balance (BC) • Export of Goods XX • Import of Goods (XX) XX Trade Balance • Export of Services XX • Import of Services (XX) XX • Unilateral Transfers (XX) • XX Current Balance • B Capital (including Financial) Accounts Balance (BK) • Direct Investment XX • Portfolio Investment XX • Short term Investments XX XX • C Errors and Omissions () XX • XX Overall Balance • D Changes in Official Reserves (R)XX

I. Balance of payment Accounting • The Balance of Payment Accounting Identity: • Assuming no errors and omissions, • BC + BK +R = 0 • Flexible exchange rate system • No change in Reserve • BC + BK = 0 => BC = - BK • correctly measured current account deficit/surplus equals correctly measured capital account surplus/deficit • current account deficit/surplus could be caused by capital account surplus/deficit • Fixed Exchange Rate System • BC + BK +R = 0 ==> R = - (BC + BK) • increase/decrease in reserve equals the combined surplus or deficit. • Implications of Imbalances in BOP • Long term deficits not sustainable

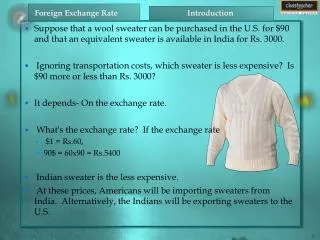

II. Parity Conditions • Assumptions • - perfect financial markets (no taxes, no transaction costs, no informational asymmetry, many buyers and sellers) • - perfect goods markets (no transaction costs, no barriers to trade, many buyers and sellers) • Purchasing Power Parity (PPP) • - relates inflation rates to changes in spot rates • A. The Law of One Price • Identical products trading in different markets should cost the same. • - Domestic markets (same currency) • - Markets across countries • - Prices expressed in common currency should be same • e.g. PU.Swheat = S($/£) PUKwheat ==>S($/£) = PU.Swheat / PUKwheat

II. Parity Conditions cont’d • B. PPP (absolute form) • If the law of one price holds for all goods and services for similar baskets of goods, • PIU.S = S($/£) PIU.K ===> S($/£) = PIU.S / PIUK • (i.e Spot exchange rate is determined by relative prices of similar baskets of goods) • C. PPP (relative form) • If the spot exchange rate between two countries starts in equilibrium, any change in differential inflation rates between them tends to be offset over a long run by an equal but opposite change in the spot exchange rate. • Exchange Rate - Direct Quote(# domestic currency/ unit of foreign currency)

II. Parity Conditions cont’d • Exchange Rate - Indirect Quote (# foreign currency/unit of domestic currency) • e.g UK inflation rate = 15%; U.S. inflation rate 10%. Hence, if the currencies were in equilibrium at the start of the period, the UK pound should fall by: • (0.10 - 0.15)/ 1.15 = - 0.043 or 4.3% or approximately by, • 0.10 - 0.15 = -0.05 or 5% • Implications of PPP: • Real return on an asset should be identical for investors of different countries. • Example: • Empirical Evidence: • 1. Generally PPP not accurate in predicting exchange rate (particularly in the short run) • 2. PPP holds well over a long run • 3. PPP holds better for countries with relatively high rates of inflation.

II. Parity Conditions cont’d • The Fisher Effect (FE) • Relates differentials in nominal interest rates to differentials in inflation rates. • Fisher Closed Condition: • The nominal interest rates in each country are equal to the required real rate of return to the investor plus premium for expected inflation. • Fisher Open Condition (Fisher Effect (Generalized Version)): • Differences in nominal interest rates are equal to differences in expected inflation. It asserts that real rates of returns should tend to equalize across countries; hence, nominal rates of interest will vary by the difference in expected inflation.

II. Parity Conditions cont’d • International Fisher Effect (IFE) • The spot exchange rate should change in an equal but opposite direction to the difference in nominal interest rates between two countries. • Forward Rate as an Unbiased Predictor of the Future Spot Rate • i.e. Forward premium on foreign currency equals forecasted change in the spot rate.

II. Parity Conditions cont’d • Interest Rate Parity (IRP) • Except for transaction costs, a difference in national interest rate for securities of similar risk and maturity should be equal but opposite sign to the forward exchange rate discount or premium for the foreign currency. • Suppose that a U.S. investor is considering to invest $1 in a money market instrument for a year. • Alternative 1: Invest in U.S. ($ denominated) money market instrument • Return = $1 (1 + i ($)) • Alternative 2: Invest in foreign money market instrument (say in Japanese Yen) • Buy Yen at spot ==> # of yen = 1/S (Assume direct quote ($/Yen) • Sell Yen forward (buy dollar forward) at F • Return in Yen = 1/S (1 + i (¥)) • Convert Yen into $ using forward rate F • Return = 1/S (1 + i (¥)) F • IRP ==> $1 (1 + i ($)) = 1/S (1 + i (¥)) F • ==> F/S = (1 + i ($)) / (1 + i (¥))

II. Parity Conditions cont’d • In general (assuming direct quote (# domestic currency/ unit of foreign currency), • Covered Interest Arbitrage (CIA) • If IRP does not hold, an arbitrageur can earn “riskless” profit by investing in the currency that offers higher return on covered basis. • Illustration: • Two money market instruments: Dollar money market - i($) = 8% per annum • Yen money market - i(¥) = 5% per annum • Exchange rates: Spot (S0) = ¥ 135/$ • Forward rate (180 days) = ¥ 134.5 /$ • Assume that the arbitrageur can borrow or lend $1,000,000 equivalent in the two markets.

II. Parity Conditions cont’d • Step 1: check if IRP holds: • S/F = (1+ id)/(1+ if) = => ¥135/ ¥ 134.5 1.04/1.025 • there exists an arbitrage opportunity • Step 2: Identify where to invest and where to borrow • Method 1: determine implied (i.e. IRP consistent) interest rate of one of the currencies • S/F = ¥ 135/ ¥ 134.5 = 1.0037 = (1 + id )/ 1.025 (by IRP) • ==> (1 + id ) = 1.0288103 or id = 0.0288/ 6 months Vs 0.04 (actual rate) • cheaper to borrow in Yen market and invest in Dollar market (i.e. Id) • Method 2: compare the domestic rate against the effective foreign rate using IRP • Recall, from IRP • id = 4% Vs if + (s0 - F / F) = 0.025 + (135- 134.5) / 134.5 = 0.0287 • cheaper to borrow in Yen market and invest in Dollar market (i.e. Id)

II. Parity Conditions cont’d • Step 3: outline the arbitrage strategy • 1. Borrow $1 m equivalent in¥ ($1,000,000 @ ¥ 135 = ¥ 135,000,000) • 2. Convert to $ at spot rate of ¥ 135 / $ = $1,000,000 • Buy forward contract to buy ¥ @ forward rate of ¥ 134.5/$ • 3. Invest in $ money market instrument for 6 months • Total Return: $1,000,000 (1.04) = $1,040,000 • 4. Repay loan • Loan in ¥ = ¥ 135,000,000 (1.025) = ¥ 138,375,000 • Loan in $ ( @ F) = ¥ 138,375,000/ ¥ 134.5 = $ 1,028,810.40 • Profit in $(excluding transaction costs) = $1,040,000 - $1,028,810.40=$11,189.60

III. Foreign Exchange Rate Forecasting • Approaches to Forecasting • 1. Technical Analysis • - Based on trends of data series • - used mostly for short term forecasting • 2. Fundamental Analysis • - based on financial and economic theory • The Balance of Payments Approach • Analysis of a country’s BOP as indicator of pressure on exchange rate • The Asset Market Approach • An exchange rate between two currencies represents the price that balances the relative supplies and demands of assets denominated in those currencies . • Hence, the relative attractiveness of a currency for investment purposes is a deriving force of exchange rate movements. • Example: impact of high economic growth

III. Foreign Exchange Rate Forecasting in Practice cont’d • Short run forecasts: • - for periods less than a year • - motivated by a desire to hedge receivables, payables etc • - accuracy more important • - techniques include: time series techniques fitting trends • Forward rate as predictor of future spot rate • Long run forecasting • - motivated by MNC’s desire to initiate direct foreign investment, raise long term finance etc. • - forecast accuracy not critical • - recommended techniques include: fundamental analysis, including analysis of balance of payments, relative inflation rates and interest rates.