Download

1 / 20

220 likes | 252 Views

Learn about financial elder abuse, its impact, legal definitions, examples, and how to prevent undue influence in elderly financial matters.

E N D

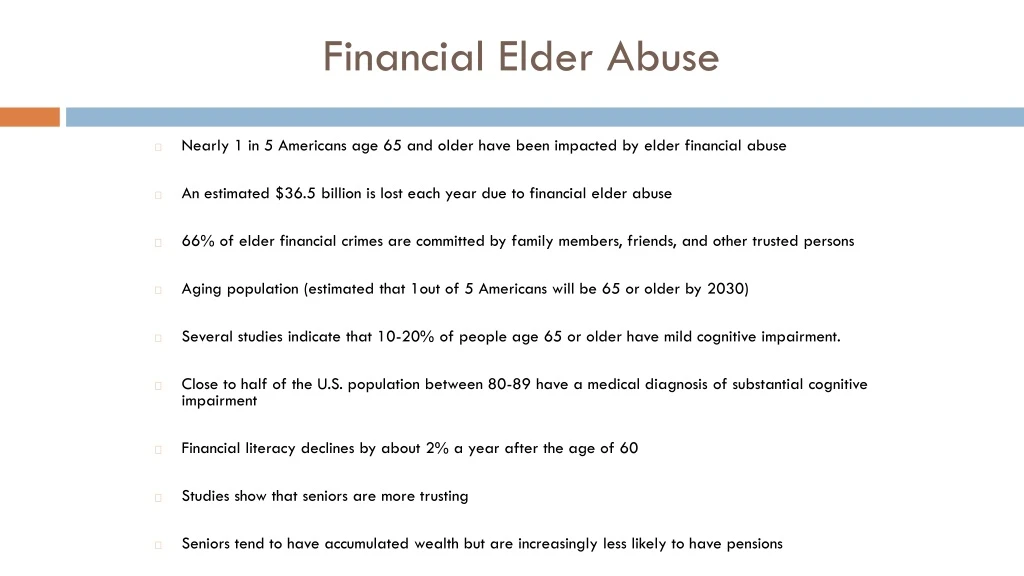

Financial Elder Abuse • Nearly 1 in 5 Americans age 65 and older have been impacted by elder financial abuse • An estimated $36.5 billion is lost each year due to financial elder abuse • 66% of elder financial crimes are committed by family members, friends, and other trusted persons • Aging population (estimated that 1out of 5 Americans will be 65 or older by 2030) • Several studies indicate that 10-20% of people age 65 or older have mild cognitive impairment. • Close to half of the U.S. population between 80-89 have a medical diagnosis of substantial cognitive impairment • Financial literacy declines by about 2% a year after the age of 60 • Studies show that seniors are more trusting • Seniors tend to have accumulated wealth but are increasingly less likely to have pensions

Financial Elder Abuse Defined (a) Financial abuse of an elder or dependent adult occurs when a person or entity does any of the following: (1) takes, secretes, appropriates or retains real or personal property of an elder or dependent adult to a wrongful use or with an intent to defraud, or both; (2) assists in taking secreting, appropriating or retaining real or personal property of an elder or dependent adult to a wrongful use or with intent to defraud, or both; (3) takes, secretes, appropriates or retains or assists in taking, secreting, appropriating or retaining real or personal property of an elder or dependent adult by undue influence, as defined in Section 15610.70. (b) a person or entity shall be deemed to have taken, secreted, appropriated, obtained or retained property for a wrongful use if, among other things, the person or entity takes, secretes, appropriates or retains the property and the person or entity knew or should have known that this conduct is likely to be harmful to the elder or dependent adult. (c) For purposes of this section, a person or entity takes, secretes, appropriates, obtains or retains real or personal property when an elder or dependent adult is deprived of any property right, including by means of an agreement, donative transfer, or testamentary bequest, regardless of whether the property is held directly or by a representative of an elder or dependent adult. (California Welfare & Institutions Code § 15610.30)

Examples of Elder Financial Abuse • cashing an elderly person’s checks without authorization • forging an elder’s signature • misusing or stealing money or property • coercing or deceiving an elder into signing a document (ie a contract, deed, Will, change in beneficiary of an insurance policy or IRA) • improper use of conservatorship, guardianship or power of attorney • advising or recommending that the elder purchase an inappropriate investment • using misleading advertising to promote or sell a financial product to seniors

Undue Influence defined: W & I Code § 15610.70 defines undue influence as follows: (a) “Undue influence” means excessive persuasion that causes another person to act or refrain from acting by overcoming that person’s free will and results in inequity. In determining whether a result was produced by undue influence, all of the following shall be considered: (1) The vulnerability of the victim. Evidence of vulnerability may include, but is not limited to, incapacity, illness, disability, injury, age, education, impaired cognitive function, emotional distress, isolation or dependency, and whether the influencer knew or should have known of the alleged victim’s vulnerability. (2) The influencer’s apparent authority. Evidence of apparent authority may include, but is not limited to, status as a fiduciary, family member, care provider, health care professional, legal professional, spiritual advisor, expert, or other qualification. (3) The actions or tactics used by the influencer. Evidence of actions or tactics used may include, but is not limited to, all of the following: (A) Controlling necessaries of life, medication, the victim’s interactions with others, access to information or sleep. (B) Use of affection, intimidation or coercion. (C) Initiation of changes in personal or property rights, use of haste or secrecy in effecting those changes, effecting changes at inappropriate times and places, and claims of expertise in effecting changes. (4) The equity of the result. Evidence of the equity of the result may include, but is not limited to, the economic consequences to the victim, any divergence from the victim’s prior intent or course of conduct or dealing, the relationship of the value conveyed to the value of any services or consideration received, or the appropriateness of the change in light of the length and nature of the relationship. (b) Evidence of an inequitable result, without more, is not sufficient to prove undue influence.

Examples from Case Law of Instruments That Were Voided Based on Undue Influence: Lintz v. Lintz(2014) 222 Cal. App.4th 1346 [decedent was fearful of the defendant, defendant took an increasingly active role with respect to the decedent’s estate planning which benefitted the defendant, defendant misinformed the decedent’s lawyers regarding the decedent’s testamentary wishes, the decedent was not independently represented when he signed the documents at issue; the documents disinherited the decedent’s youngest child who he adored and the dispositions of assets in the documents were inconsistent with the decedent’s prior actions and statements] Olson v. Washington (1936) 18 Cal. App.2d 85 [the decedent was mentally and physically infirm, she had a very close relationship with the defendant, the decedent received no consideration in return, and no independent persons were present when the joint account at issue was created] Longmire v. Kruger (1926) 80 Cal. App.230 [the decedent and the grandson had a close relationship; the widow had implicit confidence in the grandson; the decedent was elderly, infirm, partially blind and mentally and physically impaired by age and sickness; the grandson was young and healthy; the deed effected a material change in the decedent’s Will that was not satisfactorily explained; the grandson obtained the bulk of the decedent’s estate for no consideration; the deed was kept a secret for a period of time and was not recorded; and the deed was executed when nobody else was present except the decedent, the grandson and an attorney procured by the grandson]

Signs of Diminished Capacity • taking longer to complete financial tasks • missing key details in financial documents • not paying bills • confusion about accounts, funds and transactions • difficulty with everyday math • decreased understanding of financial concepts • difficulty identifying investment risk • unfounded concern about nature and extent of their finances • memory loss • drastic mood swings • changes in personality • increased passivity

Red Flags of Potential Financial Elder Abuse • reluctance to discuss financial matters that were previously discussed as a matter of course • sudden, atypical or unexplained withdrawals, wire transfers, or disbursements by the elder or someone with a Power of Attorney for the elder • abrupt or unexplained changes in legal documents or beneficiaries • sudden changes in elder’s bank or investment accounts, practices, transactions, investment style • client has recently purchased one or more potentially abusive financial products • forged or suspicious or abnormal signatures • new signers added to the elder’s account, or newly formed joint accounts between the elder and another individual • indicia of diminished physical or mental capacity/confusion • excessive interest in finances of an elder by family members, caregiver or others • family member/caregiver does not allow client to speak for themselves or is reluctant to leave client’s side during conversations/ “coaching” is overheard or evident in conversations with the elder • new individual appears on the scene and/or attempts to conduct financial transactions on behalf of the elder or impersonates the client or the client’s POA/agent • the client appears to be suddenly isolated from friends and family • -inability to contact or directly speak to the elder • changes in behavior (ie elder appears fearful, withdrawn, quiet when they used to be talkative) • client appears to be forgetful • substandard care or unpaid bills despite the apparent availability of adequate financial resources (ie disheveled appearance, poor hygiene, home or residence is missing possessions or without heat, client claims to have been evicted or to not have a place to live) • admission of financial exploitation or suspected exploitation

Potentially Abusive Products Characteristics of potentially abusive products: • illiquid • overly speculative or risky (market, inflation or issuer credit risk) • not transparent (ie share price not tied to a market value, information on assets, revenues etc not easily identifiable or easy to follow) • not backed by a financially solvent entity or enforceable security interest • funded by the investor taking out a personal loan/mortgaging real property Examples of potentially abusive products: • deferred variable annuities • equity indexed annuities • variable life settlements • private placement investments (tenancies in common, non-traded Real Estate Investment Trusts, unsecured notes, investments in a start-up business, limited partnerships) • private loans to real estate developers • complex structured products (ie collateralized debt obligations) • new life insurance policies with expensive premiums • mortgaging home equity for investment or insurance purposes • using retirement savings to invest in high risk investments

Mandated Reporters of Financial Elder Abuse The following persons must report known or reasonably suspected financial elder abuse to adult protective services or local law enforcement: • care-givers (full or part-time) • administrators, supervisors and licensed staff of any public or private facility that provides care or services to elder or dependent adults • health practitioners • clergy members • employees of Adult Protective Services • employees of local law enforcement agencies (Cal. W & I Code § 15630)

Obligations of Fiduciaries and Other Professionals Fiduciary duties: • to act in customer’s best interest • refrain from participating in any transaction that is adverse to customer’s best interest • inquire/ask questions if there are red flags • investigate further • disclose all known facts Professional duties of non-fiduciaries: • act with reasonable care

Aiding and Abetting Liability A third party may be liable for aiding and abetting in financial elder abuse through undue influence if the third party reasonably should have known of the wrongdoing and substantially assisted in the other’s actions, or financially benefitted from the wrongful conduct. (Mahan v. Charles W. Chan Ins. Agency (2017) 14 Cal. App.5th 841; Das v. Bank of America (2010) 186 Cal. App.4th 727; Wood v. Jamison (2008) 167 Cal. App.4th 156; Zimmer v. Nawabi(E.D. Cal 2008) 566 F. Supp.2d 1025.)

Special Duties of Securities Brokers and Broker-Dealers - FINRA Rules Rule 2090 - Know your customer • Broker must use reasonable diligence to know and retain essential facts concerning every customer and concerning the authority of each person acting on behalf of the customer • Essential facts include those required to a) effectively service the customer’s account; b) act in accordance with special handling instructions for the account; c) understand the authority of each person acting on behalf of the customer; and d) comply with applicable laws, regulations and rules

Special Duties of Securities Brokers and Broker-Dealers - FINRA Rules Cont. Rule 2165 - Financial Exploitation of Specified Adults (effective 2/5/18) • Allows brokerage firm to place a temporary hold on securities transactions or disbursements of an elderly or mentally or physically impaired adult if the firm or its personnel reasonably believe that financial elder abuse has occurred, is occurring, has been attempted or will be attempted • The firm must notify parties and Trusted Contact Person of the temporary hold and the reason for it, within two business days unless that person is unavailable or the firm reasonably believes that person has engaged, is engaged or will engage in the financial elder abuse • The firm must immediately initiate an internal review of the facts and circumstances that caused the firm to place the temporary hold • The temporary hold can last up to 25 business days unless terminated or extended by a state regulator or agency or court • Firms must have written procedures in place regarding the identification, escalation and reporting of matters related to potential financial elder abuse • Firms must maintain records verifying their compliance with this rule • Firms must develop and document training policies and programs reasonably designed to ensure compliance

Special Duties of Securities Brokers and Broker-Dealers - FINRA Rules Cont. Rule 4512 - Customer Account Information (effective 2/5/18) • For individual customers, brokers must obtain the name and contact information for a trusted contact person age 18 or older who may be contacted about the customer’s account • The broker-dealer must disclose in writing that it is authorized to contact the trusted contact person and disclose information about the customer’s account to address possible financial elder abuse; or to confirm the specifics of the customer’s current contact information, health status, or the identity of any legal guardian, executor, trustee, or holder of a power of attorney, or as otherwise permitted by Rule 2165 • The absence of the name of or contact information for a trusted contact person shall not prevent a member from opening or maintaining an account for a customer provided that the member makes reasonable efforts to obtain the name of and contact information for a trusted contact person

Special Duties of Securities Brokers and Broker-Dealers - FINRA Rules Cont. Prohibitions on misleading advertising • the use of a title or designation that conveys an expertise in senior investments or retirement planning where such expertise does not exist • referencing nonexistent or self-conferred degrees or designations or referencing legitimate degrees or designations in a misleading manner • holding onself out as the author of a book on senior investing which was ghostwritten by a third party vendor • the use of free lunch seminars to use high pressure tactics to promote products • inaccurate or exaggerated claims regarding the safety, liquidity or expected returns of the touted investment or strategy • misrepresentations or material omissions • conflicts of interest • misleading credentials • failure to include firm’s name • improper use of testimonials

Special Duties of Securities Brokers and Broker-Dealers - Internal Firm Rules Many major broker/dealers (ie Merrill Lynch, Morgan Stanley, Wells Fargo Advisors) have internal guidance/rules for their financial advisors regarding financial elder abuse. Examples of these rules include: • the advisor/broker is the first line of defense against potential elder abuse • the advisor/broker is not expected to determine whether an elder is the victim of financial abuse before reporting, but is obligated to report potential incidents to the designated supervisor or compliance personnel if they observe any red flags • the firm’s professionals in compliance/risk management will research the broker’s reports and determine if reporting needs to be made to a government agency or local law enforcement • firm rules protect brokers who report potential financial abuse • if advisor/broker reasonably suspects financial elder abuse, they should: • try to speak to the elder alone • ask open-ended and probing questions to determine elder’s intent and purpose and let the elder explain the reason for the transaction in their own words and without prompting • confirm the authority of anyone who claims to acting on behalf of the elder (check documentation including signatures and Power of Attorney) • contact family members (including trusted contact) and/or suggest the client bring a close family member or friend to the next meeting • immediately escalate and discuss the issue with supervisor/compliance department/ specific designated individual or group within the firm • hold/delay the transactions pending firm review and investigation • document the events • communicate with elder’s designated emergency contact or POA • review the client’s account for transactions/patterns that could indicate a problem • maintain frequent contact with the client • have a manager also communicate with the client

Special considerations for attorneys • Duty of Confidentiality • No exception for suspected financial elder abuse • ABA Model Rule 1.14 would allow an attorney who reasonably believes that the client has diminished capacity, is at risk of substantial, physical, financial or other harm unless action is taken, and cannot adequately act in his or her own interest to take reasonably necessary protective action, including consulting with individuals or entities who have the ability to take action to protect the client, and in appropriate cases, seek the appointment of a guardian ad litem, conservator or guardian. In such circumstances, the lawyer may reveal information about the client, but only to the extent reasonably necessary to protect the client’s interests. • ABA Model Rule 1.14 has NOT been adopted in California

What can you do if you suspect financial elder abuse? • try to speak to the elder alone • ask open ended and probing questions about the proposed transaction • contact family members (other than the influencer) • Report it to Adult Protective Services • Report it to local law enforcement • Report it up the chain of command (if you’re part of a larger organization (ie a financial advisor, associate or junior partner of a law firm or CPA firm, etc.) • Most broker-dealers have procedures regarding how and to whom to escalate (see above) • Freeze the proposed transaction pending further review and investigation • File an interpleader action with the court • Consult with regulator (if it concerns an investment or insurance product) • securities regulators (SEC, FINRA, CA Dept of Bus. Oversight) • insurance regulators (CA Dept. Of Insurance, NASAA) • real estate regulators (CA Dept. Of Real Estate) • Consult with financial elder advocacy group (AARP, CANHR) • Consult with private attorney • Withdraw from the relationship

Scenarios Scenario 1: Elderly woman who has been client of the firm for several years, and who has an adult son who is the POA, comes into the bank with the POA to make a $10,000 cash withdrawal from her brokerage account, which is a significantly larger sum than typical. She is usually friendly and talkative and knows her banker. However, when the banker asks her the reason for the withdrawal, she is unusually rude and refuses to discuss it.

Scenarios Cont’d. Scenario 2: Elderly client has been customer of broker’s for four years. Client stops by broker’s office regularly and broker considers the client to be a friend. Client has instructed broker to never call his house, and to never leave messages for him at the house. Client never schedules meetings with broker in advance. Client has told broker on multiple occasions that one of his primary objectives is to take care of his daughter and grandchildren. About 4 days before client’s death, his wife (from a second marriage) contacts broker. Broker calls back and speaks to wife who says client is very ill and wants to put her on the account as a joint owner. Broker asks to speak to client who says he wants to add his wife onto the account and also change the beneficiaries on two annuities he purchased outside of the firm from his daughters to his wife. Broker prepares the paperwork and brings it to the house the following day and client signs it. Wife is not in the room but is within earshot. Broker processes the transactions and does not mention it to his supervisor until after client has died. Then, he just tells supervisor that client had asked for his wife to be added to the account.