Download

1 / 42

420 likes | 536 Views

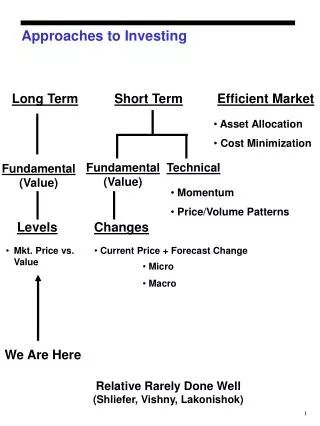

Investing for the Next Decade “The Age of “Macro” Investing”* *The Wall Street Journal, Sept. 10-11, 2011 pg B7. Objectives for the Course. Understand the characteristics and the reasons for investing in various securities.

E N D

Investing for the Next Decade “The Age of “Macro” Investing”* *The Wall Street Journal, Sept. 10-11, 2011 pg B7.

Objectives for the Course • Understand the characteristics and the reasons for investing in various securities. • Understand the relationship between risk and return when investing. • Understand the role of diversification in successful investing. • Be familiar with financial considerations important to those nearing retirement or currently retired.

Today’s Class • Become familiar with characteristics of popular financial securities commonly used by individual and institutional investors and how these instruments are traded on organized security exchanges.

Basic Types Major Subtypes Interest-bearing Money market instruments Fixed-income securities Equities Common stock Preferred stock Derivatives Futures Options Classifying Securities

Interest-Bearing Assets • Money market instruments are short-term debt obligations of large corporations and governments. • These securities promise to make one future payment. • When they are issued, their lives areless than one year. • Fixed-income securities (a bond) are longer-term debt obligations of corporations or governments. • The typical bond promise to make fixed payments according to a pre-set schedule. At maturity you received the principal (par value) back. • A “zero coupon” bond pays no annual interest. It is bought at a discount price that reflects the current interest rate. At maturity pays the par value (typically stated as 100). • When they are issued, their maturity exceeds one year.

Money Market Instruments • Examples: U.S. Treasury bills (T-bills), bank certificates of deposit (CDs), corporate and municipal money market instruments. • Potential gains/losses: A known future payment/except when the borrower defaults (i.e., does not pay). • Price quotations: Usually, the instruments are sold on a discount basis, and only the interest rates are quoted, not the prices.

Why Buy Money Market Securities? • A safe place to store cash balances and earn interest on the proceeds. • Provides liquidity for your portfolio. • Most money market instruments have a very low probability of default. • Price risk is low because of short time to maturity. • However, the interest earned will be the lowest of all fixed income assets.

Fixed-Income Securities (Bonds) • Examples: U.S. Treasury notes, corporate bonds, municipal bonds. • Bond Quality is rated by three private companies: Standard & Poor’s (AAA), Moody’s (Aaa) and Fitch’s. • Rating ranges from “AAA” (best) to “D” (in default) • Investment grades are AAA, AA, A and BBB-. • Like grades, “+” and “-” may be used, eg. AA-

The price (per $100 face) of the bond when it last traded. You will receive 6.875% of the bond’s face value each year in 2 semi-annual payments. The Yield to Maturity (YTM) of the bond. Quote Example: Fixed-Income Securities • Price quotations from www.wsj.com—the online version ofThe Wall Street Journal (some columns are self-explanatory):

Pros and Cons of Bonds in a Portfolio • Pros - Include Bonds in a portfolio to: • Reduce risk. Bonds are more stable in value than stocks or many other assets. • Provide income. They provide consistent payments every six months(the interest). • Provide some liquidity. U.S. Treasury Bonds are highly liquid, however, many others are not. • Cons - Risk of Bonds include: • Prices vary with interest rates. Up and down. • Can be highly volatile. Like the last three years. • Many bonds are highly illiquid. Eg. Municipals and some corporates.

Common Stock • Represents ownership in a company. You are an equity owner and typically have voting rights in the company. • May be publicly traded, (eg. Williams Companies) or privately held, (Koch Industries). • Typically you get two things of value when you buy a stock:(1) The price rises over time and (2) dividends. Stocks that pay no dividends but have a good business are typically called “growth stocks”. Stocks that pay a relatively large dividend (eg. 3+%) are typically called “value stocks”.

Common Stock Price Quotes Onlineat http://finance.yahoo.com* *From Monday, Sep 12, 2011

The Pros of having stocks in a portfolio • Stocks provide the growth factor in a portfolio • Stock prices tend to rise over time as the economy grows. • Dividends tend to rise over time reflecting inflation and growth in the economy. • See the S&P Dividends Aristocrats list of 42 stocks that have raised their dividends every year for the past 25 years. Most are household names : Johnson & Johnson; Emerson Electric; Pepsico; Proctor and Gamble, etc. • Exxon Mobil has increased dividends an average of 5.7% a year for 27 years. • Most portfolios should have some common stock exposure

The Cons of owning stocks • Stocks are more “risky” than the other assets we have discussed. • That is, they tend to vary more in price. • They go to zero if the company goes bankrupt. • There is a wide variety of stocks that you can own, ranging from very safe to very risky. Thus, more time is needed to research individual stocks.

Popular Stock Market Indexes • Dow Jones Industrials – 30 large blue chip companies (DJIA). • Standard and Poor’s – • S&P 500 Index • S&P 400 Midcap Index • S&P 600 Small cap index • Russell 2000 – small cap firms • NASDAQ Composite – stocks listed on the National Assoc. of Securities Dealers Automated Quote System.

Stock Market Indexes, I. • Indexes can be distinguished in four ways: • The market covered, • The types of stocks included, • How many stocks are included, and • How the index is calculated • price-weighted, e.g. DJIA, versus • value-weighted, e.g. S&P 500.

Stock Market Indexes, II. • For a value-weighted index (i.e., the S&P 500), companies with larger market values have higher weights. • For a price-weighted index (i.e., the DJIA), higher priced stocks receive higher weights. • This means stock splits cause issues. • But, stock splits can be addressed by adjusting the index divisor. • Note: As of March 8, 2008, the DJIA divisor was a nice “round” 0.122834016!

Why do we have so many indexes? • Many are based on something called market capitalizationor market cap for short. • Market cap is the $ value of the equity of the firm that is in the hands of the shareholders: • Market cap = shares outstanding x $ price per share • It varies daily because the price of the stock changes • Shares outstanding change gradually, usually at most at each quarter. • Others are based on the geographical region or company characteristics.

Common Categories of Stock Indexes • By Market Cap • All Cap – Russell 3000; Wilshire 5000 • Large Cap – S&P 500; Russell 1000 • Mid Cap/Small Cap – S&P 400/600; Russell 2000 and 2500 • By Firm Objective • Growth • Value

By Geographical Area; • EAFE (Europe, Australia, Far East) • BRIC (Brazil, Russian, India, China) • MSCI ACWI (Morgan Stanley Capital International World Index) • By type of market • Emerging Markets • Frontier Markets

Useful Internet Sites www.nasdbondinfo.com(current corporate bond prices) www.investinginbonds.com(bond basics) www.finra.com (learn more about TRACE) www.fool.com (Are you a “Foolish investor”?) finance.yahoo.com(prices for option chains) www.wsj.com (online version of The Wall Street Journal) www.morningstar.com (Morningstar’s information on stocks and mutual funds)

The “Capital” life cycle of a business • An idea leads to starting a small business, financed by the owner’s own money – equity. • A bank may provide initial financing – debt. • A Private equity or Venture Capitalist investor may provide additional capital to finance growth – equity financing. • Ultimately, the successful firm decides to “go public” and sell its common stock on the open market. This is called an Initial Public Offering (IPO).

Private Equity and Venture Capital • Private Equityis the used for the rapidly growing area of equity financing for nonpublic companies. • Because banks generally are not interested in making loans to start-up companies, especially small ones. • Firms often seek equity financing from a venture capital (VC) firm, an important part of the private equity markets.

Venture Capital, I • Venture Capitalrefers to financing new, often high-risk, start-ups. • Individual venture capitalists invest their own money. • Venture capital firms pool funds from various sources, like • Individuals • Pension funds • Insurance companies • Large corporations • University endowments • Venture capitalists know that many new companies will fail, but the companies that succeed can provide enormous profits.

The Venture Capital Process • To limit their risk: • Venture capitalists generally provide financing in stages. • Venture capitalists actively help run the company. • At each stage, enough money is invested to reach the next stage. • Ground-floorfinancing • Mezzanine Level financing • At each stage of financing, the value of the founder’s stake grows and the probability of success rises. • If goals are not met, the venture capitalists withhold further financing. • If a start-up succeeds: • The big payoff frequently comes when the company is sold to another company or goes public.

Selling Securities to the Public • Theprimary market is the market where investors purchase newly issued securities. • Initial public offering (IPO): An IPO occurs when a company offers stock for sale to the public for the first time. • Seasoned equity offering (SEO): If a company already has public shares,an SEO occurs when a company raises more equity. • The secondary market is the market where investors trade previously issued securities. An investor can trade: • Directly with other investors. • Indirectly through a broker who arranges transactions for others. • Directly with a dealer who buys and sells securities from inventory. • The NYSE is an example of a secondary market for securities.

Bringing an IPO to the Market • The issuing firm hires an investment banking firm that performs the following functions: • Development of the prospectus: • Red Herring; Official • Origination • Underwriting arrangement – “best efforts”, “all or none”, “firm purchase”, etc. • Syndication – the group of investment banks that will help sell the issue • Distribution – Through the syndicate • Market Stabilization

The Secondary Market for Common Stock • Most common stock trading is directed through an organized stock exchange or trading network. • Whether a stock exchange or trading network, the goal is to match investors wishing to buy stocks with investors wishing to sell stocks. • The market maker function is key to providing a liquid and fair market for any financial asset. They are ready to take the other side of your order.

The New York Stock Exchange • The New York Stock Exchange (NYSE), popularly known as the Big Board, celebrated its bicentennial in 1992. • The NYSE has occupied its current building on Wall Street since the early 1900’s. • For 200 years, the NYSE was a not-for-profit New York State corporation. • The NYSE went public in 2006 • (NYSE Group, Inc., ticker: NYX) • Naturally, NYX stock is listed on the NYSE • In 2007, NYSE Group merged with Euronext to form NYSE Euronext, the world’s largest exchange.

NYSE Seats and Trading Licenses • Historically, the NYSE had 1,366 exchange members. These members: • Were said to own “seats” on the exchange. • Collectively owned the exchange, although professionals managed the exchange. • Regularly bought and sold seats (Record seat price: $3 million in 2005) • Seat holders could buy and sell securities on the exchange floor without paying commissions. • In 2006, all of this changed when the NYSE went public. • Instead of purchasing seats, exchange members purchase trading licenses: • number limited to 1,500 • In 2007, a license would set you back a cool $55,000—per year. • Having a license entitles the holder to buy and sell securities on the floor of the exchange.

Types of NYSE Members • The largest number of NYSE members are registered as commission brokers. • Commission brokers execute customer orders to buy and sell stocks. • Second in number of NYSE members are specialists, or market makers. • Market makers are obligated to maintain a “fair and orderly market” for the securities assigned to them.

NYSE-Listed Stocks • In 2006, the total number of companies listed on the NYSE represented a total global market value of about $25 trillion. • Initial and annual listing fees are charged based on the number of shares. • To apply for listing, companies have to meet certain minimum requirements with respect to • The number of shareholders • Trading activity • The number and value of shares held in public hands • Annual earnings

Operation of the New York Stock Exchange • The fundamental business of the NYSE is to attract and process order flow. • In 2007, the average trading volume on the NYSE was over 2 billion shares a day. • Volume breakdown: • About one-third from individual investors. • Almost half from institutional investors. • The remainder represents NYSE-member trading, mostly from specialists acting as market makers.