Download

1 / 11

230 likes | 1.23k Views

Arbitrage Pricing Theory. In apt there are a no of industry specific and macro economic factors that affect the security’s return unlike CAPM where Beta is considered the most important single factor

E N D

In apt there are a no of industry specific and macro economic factors that affect the security’s return unlike CAPM where Beta is considered the most important single factor • Investors indulge in arbitrage when they find differences in returns of assets with similar risk characteristics.

Return on asset=predictable component +unpredictable component • E(Rj)=Rf+UR • Rf=predictable return based on information available to investors ), UR=unanticipated part of return (future information=firm specific or market related) • E(Rj)=Rf+URs+URm • URs=unexpected component of return , specific factors related to firm • URm= unexpected component of return , market related factors

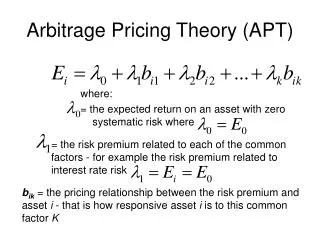

Risk and APT • Risk from firm specific factors- diversifiable= unsystematic risk • Risk from market related factors - cannot be diversified= systematic risk • Multi factor model unlike CAPM • Market risk can be caused by many factors such as changes in GDP, inflation, interest rates • Under APT sensitivity of the assets return to each factor is estimated .for each firm there are as many betas as no of factors • E(Rj)=Rf + 1F1+ 2F2+ 3F3…..+ nFn) +URs

Steps for calculating expected return under APT • Searching for factors that affect the assets return- • Estimation of risk premium for each factor • Estimation of factor beta

Difference between CAPM & APT • CAPM has a single non-company factor and a single beta, whereas arbitrage pricing theory separates out non-company factors. • Each of these requires a separate beta. The beta of each factor is the sensitivity of the price of the security to that factor.

Difference between CAPM & APT 2.APT does not rely on measuring the performance of the market. it directly relates the price of the security to the fundamental factors driving it. • The problem with this is that the theory in itself provides no indication of what these factors are, so they need to be empirically determined..

Difference between CAPM & APT • The potentially large number of factors means more betas to be calculated. There is also no guarantee that all the relevant factors have been identified. • This adds complexity - reason arbitrage pricing theory is far less widely used than CAPM

Example • Suppose that GNP, inflation, interset rate, stock market index and Industrial production affect the share return of the firm ABC ltd • You hav einformation about the forecasts and actual values of the factors, firms GNP beta, inflation Beta etc • Investor wants to invest in ABC

Total return on share= anticipated return + unanticipated return • Anticipated return= effects of known information such as expected inflation and other factors • To determine the surprise part in systematic factors? • Difference between expected and actual values of the factors =Surprise shareholders to be compensated for this • This difference multiplied by the factor beta will compensate the shareholders for factors systematic risk • Expected value of the factor is the risk free part